Organizing Public Sector Debt statistics to Maximize Their Analytical Use and International Comparability

The Quarterly Public Sector Debt (QPSD) Initiative launched by the World Bank in December 2010, in cooperation with the International Monetary Fund (IMF), aims to provide comprehensive, timely and internationally comparable information on central and general government debt and more broadly, debt of the public sector for both industrialized, high income countries as well as those classified as low- and middle-income. The initiative is a response to recommendations by the Inter-Agency Group (IAG) on Economic and Financial Statistics and the imperative to address important gaps in international data systems highlighted by the global financial and economic crisis that erupted in 2008.

A core aim of the QPSD Initiative is to institute a standardized measure for each dimension of public sector debt. Information in the QPSD database covers all relevant sectors of the economy: (1) general government, (2) central government, (3) budgetary central government, (4) non-financial public corporations (5) financial public corporations, and (6) the total consolidated public sector debt. The instrument coverage for each sector is identical, comprising of (1) debt securities, (2) loans, (3) currency and deposits, (4) Special Drawing Rights, (5) other accounts payable, and (6) insurance, pensions, and standardized guarantee schemes.

Like with the Quarterly External Debt Statistics (QEDS) reporting to the QPSD is voluntary but countries are actively encouraged to participate, with the central and lately the general government being the minimal requirements to participate in the initiative. To date, a total of 82 countries provide quarterly information on their public debt. Of these reporting countries, 49 percent are classified as high-income and 51 percent constitute low- and middle-income countries. While most countries that have committed to report to the QPSD do so on a regular basis most still find it a challenge to provide data that covers all sectors of the economy and all borrowing instruments. Relatively few countries are found to have the capacity or resources to compile fully comprehensive gross debt statistics as defined in the Public Sector Debt Statistics Guide for Compilers and Users (PSDS Guide) and in the Government Finance Statistics Manual 2014 (GFSM 2014). Typically reports to the QPDS consist of only two, out of six, types of instruments - debt securities and loans.

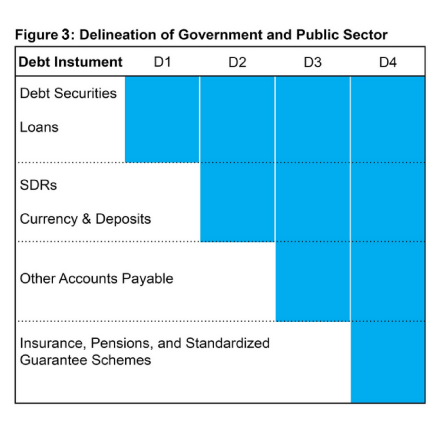

In order to enable users to make full use of the data that are available in the QPSD database and, at the same time, ensure that cross-country comparisons of indicators are coherent, the IMF, the OECD, and the World Bank have collaborated on defining a presentational debt matrix, referred to as D1-D4, that address the issue of inconsistent cross-country coverage of borrowing instruments.

The D1-D4 presentation classifies gross government debt and public sector debt into four categories, as defined in the 2012 IMF Staff Discussion Note: “What Lies Beneath: The Statistical Definition of Public Sector Debt” (PDF). Under this classification system the coverage of instruments ranges from a narrow definition that includes only debt securities and loans (D1) to a fully comprehensive definition that covers all six types of instruments (D4), described above and defined in full detail in the PSDS Guide and GFSM 2014. D1 comprises debt securities and loans, and constitutes the largest share of public debt. D2 comprises all D1 instruments, plus SDR holdings and currency and deposits. In the majority of countries, these are held by the central bank and classified under the sector ‘financial public corporations.’ D3 includes other accounts payable (in addition to all instruments captured by D2), and provides an important indicator of crisis in periods of financial distress. Finally, D4 covers all six debt instruments, including Insurance, Pensions and Standardized Guarantee Schemes (IPSGS) in addition to the indicators covered under D3. As evidenced by the recent financial crisis, IPSGS can pose a significant financial risk. However, the difficulties of compiling a comprehensive statistical measurement of such obligations is recognized. Figure 3 illustrates how the D1-D4 categories are delineated: the area shaded in blue indicates which instruments are included in each category.