The World Bank Debtor Reporting System (DRS) and the Quarterly External Debt Statistics (QEDS) both measure external debt stocks but they do so from different optics and levels of disaggregation. The DRS demands loan-by-loan reporting of public and publicly guaranteed debt and aggregate reporting for the non-guaranteed debt of the private sector. QEDS requires aggregate reporting in conformity with The External Debt Guide for Compilers and Users (2013). It recommends a primary presentation of external debt by the main institutional sectors of the economy. These are defined in the IMF Balance of Payments Manual (Sixth Edition) as the General Government Sector, Monetary Authorities Sector (Central Bank and other deposit-taking corporations) and Other Sectors. In addition, intercompany lending is separately identified. The IMF Special Data Dissemination Standard (SDDS) and General Data Dissemination Standard (GDDS), which underpin the Quarterly External Debt Statistics (QEDS) are based on presentation of data according to this criterion.

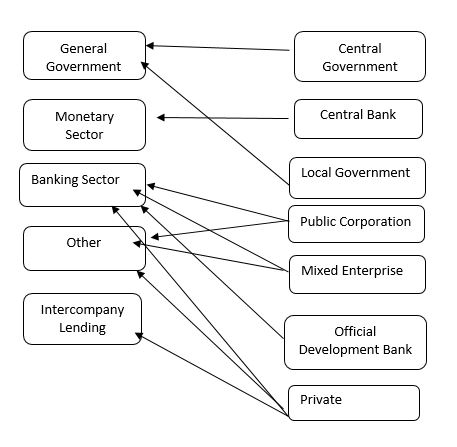

The DRS uses a classification by debtor as the primary criterion for presentation and publication of external debt data, and, below that a sub-division by type of creditor. The DRS identifies seven categories of debtor:

- Central government. The government of the country as such, includes administrative departments thereof.

- Central Bank. The monetary authority, normally the agency that issues currency and holds the country’s international reserves.

- Local government. All political subdivisions, such as states, provinces, and municipalities.

- Public corporation. Incorporated or unincorporated entities wholly owned by the governmental sector, which usually covers most of their expenses by selling goods or services to the public. Typical examples are railroads and public utilities. Both non-financial and financial corporations are included, except for official development banks, which are shown separately. Commercial banks are also included, if wholly owned by the public sector.

- Mixed enterprise. Incorporated entities, financial and non-financial institutions (excluding development banks), in which the public sector has more than 50 percent (but less than 100 percent) of voting power. If the public ownership is 50 percent or less, the enterprise is considered private; if the public ownership is complete, the enterprise is considered public.

- Official development bank. Financial intermediaries primarily engaged in making long-term loans beyond the capacity of conventional institutions and which do not accept monetary deposits.

- Private. All borrowers not included in the preceding categories

The correlation between the DRS debtor categories and the institutional sectors of the economy that underpin reporting to QEDS for countries following either the Special or the General data dissemination standards (SDDS and GDDS) is set out below (Figure 1).

Figure 1: Link between the categories of debt in DRS and QEDS

There are many complementary aspects of DRS and QEDS data as data on short-term debt illustrate. Countries reporting to the DRS are obligated to provide information only on their long-term external debt obligations. As a service to users the World Bank includes information on the total stock of countries’ short-term debt in its annual publication International Debt Statistics and the related online database. These data are captured from national sources, increasingly through reporting to QEDS, or from the information collated by the Bank for International Settlements (BIS). The QEDS reporting requirement asks for data on both long-term and short-term external debt stock for each institutional sector of the economy. This disaggregation enables users to identify those sectors of the economy most reliant on short-term debt financing and to make cross-country comparisons.