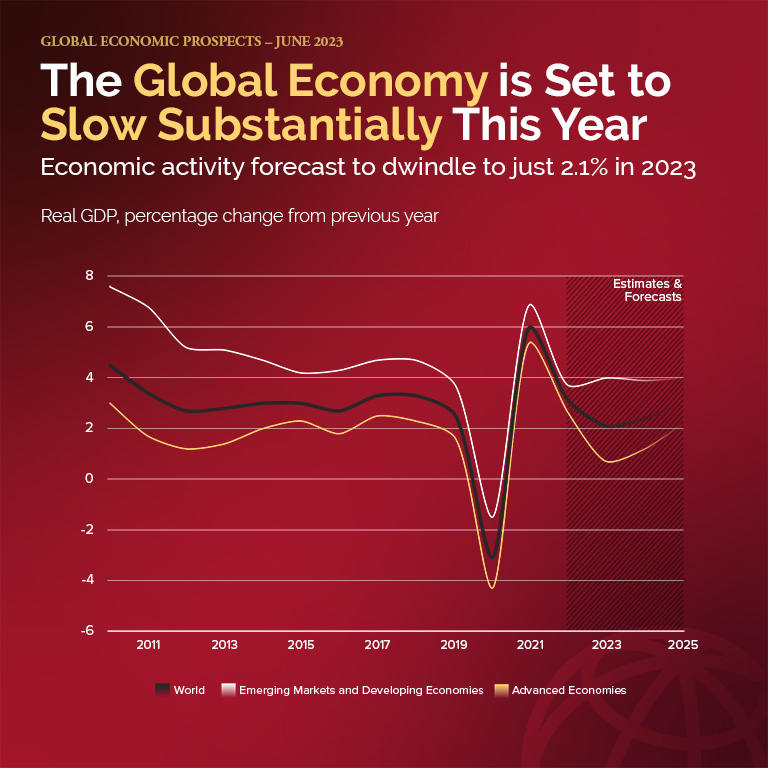

Global growth has slowed sharply, and the risk of financial stress in emerging markets and developing economies (EMDEs) is intensifying amid elevated global interest rates, according to the World Bank’s latest Global Economic Prospects report. Global growth is projected to decelerate from 3.1% in 2022 to 2.1% in 2023. In EMDEs other than China, growth is set to slow to 2.9% this year from 4.1% last year. These forecasts reflect broad-based downgrades. To help us learn more, Director of the World Bank’s Prospects Group, Ayhan Kose joins Expert Answers to discuss.

Timestamps

00:00 Welcome! Introducing the topic and the expert

00:37 Main headlines from the latest Global Economic Prospects report

01:44 Main drivers of the economic slowdown

02:48 Why is growth so important

04:50 The fight against inflation

06:02 Interest rates hikes and emerging markets

08:57 Turmoil in the US and European banking sector

10:37 Growth and poverty

12:45 Sovereign debt situation

14:44 How to unleash growth

15:50 Thanks Ayhan for sharing your expertise!

Transcript

[00:00] - Global growth will decline from 3% last year to around 2%. You need growth to solve the, kind of the investment challenge. You need growth to solve the climate challenge.

- High inflation, tight financial conditions, and record debt levels. The world economy is hobbled, and many countries are simply growing poor. The prospects for growth are weak and growing weaker. So what's driving this slowdown, and what needs to be done to unleash the global economy's full potential? For answers to that and more, we turn to the World Bank's Deputy Chief Economist, Ayhan Kose.

[00:37] - So the Global Economic Prospects is the bank's flagship economic forecast. What are your headline numbers this time around?

- So, Paul, global economy is going through a tough period. It's on a precarious footing. We are seeing a sharp and synchronized slowdown. When you look at all the economies in the world, 70% of them will see weaker growth this year than what they delivered last year. When you look at headline numbers, there is, of course, a sharp slowdown. Global economy will, the global growth will decline from 3% last year to around 2%. In the case of advanced economies, slowdown is even deeper. Almost all of them will end up seeing weaker growth this year. When you look at emerging market developing economies, other than China's big contribution, these economies will also see slow growth from around 4% to 3%. So all in all, a difficult year ahead of us.

[01:44] - So across the board of slowdown, what's driving that slowdown?

- There are multiple reasons driving the slowdown. Of course, tight monetary policy. That has been in place over the past 18 months. Increasingly, all countries are feeling the impact of tightening financial conditions. Inflation, as much as it has been coming down, it's still elevated. So that affects demand. And recent banking stress led to quite a bit of damage in terms of confidence. And you look at high frequency data, you see that credit conditions are getting deteriorated. There are other reasons. We look at global trade. Trade is slowing very sharply relative to what we saw last year. Of course, the Russian invasion of Ukraine did not help. There is an overall confidence problem and uncertain prospects dampening investment as well.

[02:48] - Let's pause there and go back to kind of economics 101. Why is growth so important? What does it mean for everyday people, and in particular, the poorest people around the world?

- Growth is critical when it comes to, of course, increasing income levels, when it comes to eliminating poverty, when it comes to our universal objective, sharing prosperity. We need to expand the pie to be able to have better distribution of that pie. We need to expand the pie so more people will join the ranks of the people in advanced economies in terms of living standards. Let me talk about a couple of results we have in the report when it comes to income dynamics. When you look at emerging market developing economies and the destruction of these multiple crisis had in these economies, 30% of these economies are not going to get back to per capita income levels they had in 2019 by the end of 2024. So four years after the pandemic, we still have, at the per capita income level, weaker, lower income than what we had prior to the pandemic. We want these economies to grow faster so their income levels get closer to the income levels of advanced economies. But that is not happening at the pace we want. In low income countries, we have even a worse situation. Income levels are around 2 to 3% of basically advanced economy income levels. How we are gonna increase the income? Of course, we need to have more growth.

- And so if you care about inequality, you need to care about growth.

- Of course, you need to care about growth, and policies are critical, growth-enhancing policies. In some cases, of course, distribution targeting policies, critical. But you need growth to solve the, kind of the investment challenge. You need growth to solve the climate challenge.

[04:50] - Inflation has been one of the biggest topics of conversation in the the economics world over the past year or two. Where are we in the fight against inflation?

- I think we have made a significant progress. In many countries, we think that inflation has already peaked. At the global level, we saw quite high inflation, around 9% last year. Now, that number has been coming down.

- Historically, that's a high level for inflation.

- Historically, that's a high level. I think the number in many countries, the highest we have seen in a generation. And by the end of next year, our forecast suggested, at the global level, the inflation is gonna come down around 3%. Is that enough? For many central banks, in terms of their inflation targets, that's not going to be enough. So central banks are going to be on the offensive in terms of trying to contain inflationary pressures. And when you look at the core inflation, that is quite stubborn. And in a number of advanced economies, we see core actually is creeping up. So there are good news and there are still worrying signs when it comes to inflation.

[06:02] - And of course, the big lever that central banks have to pull to fight inflation is rate hikes. We're in a rate hike cycle. That's the most aggressive since at least the 1980s. What has that rate hiking cycle, the aggressiveness of that rate hike cycle meant for emerging markets?

- So when we think about the current tightening cycle, it is by far the fastest and the steepest one since we have seen in the early 1980s. As I mentioned, it was necessary to act and act aggressively on the part of central banks to contain inflationary pressures. You are trying to slow down the economy, and we see the impact of that this year. Emerging market developing economies have been affected especially those they have lower credit ratings. When you look at our forecast downgrades, we downgraded the forecast. In countries, they tighten the monetary policy more, and that we downgraded the forecast in countries with larger vulnerabilities, with lower credit ratings. And when you look at the number of emerging market, developing economies, they're experiencing spreads above 10%. The number of those countries has increased quite significantly over the past two years. Of course, if this spreads around 10%, that means you are having difficulty in accessing in international financial markets, accessing funding. So significant challenges for frontier markets and significant challenges for those economies, they have to win deficits. Current account deficits and fiscal deficits in an environment, credit condition is tightening.

- So just breaking that down a little bit. When advanced economies, those that are seen as less risky, raise their rates, the emerging markets, developing economies, frontier markets, they have to raise their rates even further to remain competitive. So when they need to access markets, they need to borrow money, it's now more difficult for them to do that than it was previously.

- So, of course, emerging market developing economies, they are increasing interest rates with the idea that they have the inflation problem. Inflation's a global problem. In some cases, there is the idea of basically defending the currency. But all in all, when they increase interest rates, they are tightening financing conditions domestically, and the major central banks increasing interest rates, those have implications, of course, global financing conditions. So in the case of emerging developing economies, it is double whammy. Domestically, they are basically slowing down their economies, and globally, they see tighter financing conditions because of interest rate hikes.

[08:57] - The other big side effect of raising rates has been turmoil in the US and European banking sector. Obviously, a lot of attention is paid to the effects of that within those economies. What does it mean for the rest of the world when there's turmoil in the banking sectors in Europe, in the US?

- So one byproduct of these interest rate increases, the banks with somewhat weak balance sheets or large unrealized losses, run into difficulties. Policy makers in Europe as well as in the United States acted aggressively and contained the problem. But there is damage, and that damage manifests itself in credit conditions already, loan demand has been declining, cost of financing has been increasing. Now, if the turbulence re-emerges and spreads to other countries, we will end up seeing, of course, much weaker growth especially next year than what we are forecasting. Already, our forecast suggests next year growth is going to be still tepid. We might end up seeing much lower growth. Our hope is that the banking sector stress will be contained. If it is contained in advanced economies, those economies will be affected. But if it spreads to emerging market developing economies, we can easily see growth going down below 2% in emerging, developing economies. Of course, that will be a rather low number in terms of improving prospects in these economies.

[10:37] - We talked earlier about why growth matters, and in particular, for the poorest. What have you found there?

- So in this latest edition, we have a chapter on fiscal challenges in low income countries. And we really need to focus on these 28 economies, per capita income, give and take, less than $1,000. Their fiscal challenges are chronic. Whether you look at the revenue side, whether you look at expenditure side, they have been experiencing persistent problems. When you look at the revenue side, revenue to GDP has been around, give and take, 20%. They haven't been able to make much progress in terms of expanding the revenue pace. Of course, weak tax collection, weak tax revenues led to this outcome. And when you look at the collection of taxes, the direct taxes, indirect taxes, they have been lagging behind other developing economies. When you look at on the expenditure side, what you see is growing expenditure pressures, and these pressures are quite critical for these economies. Our low income economies, you want them to invest in education, you want them to invest in healthcare. So you want them aggressively, actually spend on the items that are gonna translate into better development outcomes. Because of the revenue challenges, they are spending less to education, less to health than other developing economies have been doing. So when you combine the problems on the revenue side, on the expenditure side, you end up with deteriorating fiscal picture. So relative to 2011, almost 90% of them, now, they have weaker fiscal positions, and this is not a good sign going forward in terms of their ability to make significant progress in their development objectives.

[12:45] - Another big topic of conversation has been the sovereign debt situation, and you talk about it in the report. What do you say about debt?

- So in the context of debt, let me first talk about these low income countries. Obviously, these fiscal challenges led to large problems in terms of their ability to pay debt, but at the same time, they have been accumulating debt at a rapid pace. So if you look at the debt-to-GDP ratio, in 2011, debt number was around 37% in low income countries. Today, that number is close to 70%.

- Wow.

- So they ramped up significant amount of debt. In 2015, only five low income countries was in debt distress or high risk of debt distress. Today, that number went up to 14. So out of 28 low income countries, half of them are experiencing severe debt problems. Of course, interest rate payments have increased relative to their revenues as global financing conditions have been getting tighter. The bigger challenge is that, when we look at this millennium, in the first two decades, from 2000 to 2019, there were only 19 sovereign debt defaults. Since 2020, we have already seen 14 sovereigns defaulting on their debt obligations. So it is a reality. We have a debt crisis in our hands, and in all likelihood, in an environment with weak growth, tighter financing conditions, that debt problem will get larger. That's why global community has to work together to address this issue.

[14:44] - Just as we wrap up, we've talked here about a broad slowdown in growth. What needs to be done to unleash growth?

- I think the global economy's challenges are very clear. Policy-makers are aware of the problems in the near term in terms of stabilizing their economies with respect to inflation, and with respect to near term growth prospects. Inflation is still the number one problem. Price stability is a must to have sustained growth. So fiscal authorities and the central banks, they need to work together to address the challenge of elevated inflation. Over the medium and the long term, there are huge challenges in the context of pushing potential growth up, addressing climate change, and of course, addressing broader problems of development that will require serious supply-side structural interventions, and we articulate these interventions in the report.

[15:50] - Ayhan, thank you so much.

- Thank you, Paul.

- I appreciate it. A huge thanks to Ayhan Kose for sharing the latest insights from the Global Economic Prospects. You can download the report for free on the World Bank website at worldbank.org/GEP. Until next time. Goodbye.

ABOUT WORLD BANK EXPERT ANSWERS

Every episode of Expert Answers sits you down with a World Bank specialist: an expert answers with expert answers. From debt relief to gender equality. From COVID-19 response to inclusive growth, and much more. Our goal is to help you understand some of the biggest issues in international development today by asking our colleagues about what works on the ground and what we can do to meet the biggest global challenges. Watch previous episodes of Expert Answers!

ABOUT THE WORLD BANK GROUP

The World Bank Group is one of the world’s largest sources of funding and knowledge for low-income countries. Its five institutions share a commitment to reducing poverty, increasing shared prosperity, and promoting sustainable development.