WASHINGTON, April 19, 2013 ― Most economies in the Europe and Central Asia (ECA) region grew in 2012, with an average growth rate of 2.5 percent, and are expected to grow in 2013 at a slightly higher rate of about 2.9 percent, World Bank officials said at a press briefing during the World Bank/IMF Spring Meetings 2013. Recovery in ECA will continue to be the slowest compared to other regions in the world, and will be multi-speed, with the western part of the region growing at a much slower pace than the eastern part. Protracted recession and slow growth recovery further aggravate the persistent unemployment in some parts of the region, which in turn has long-term implications for the region’s competitiveness and social inclusion.

"Since the crisis, we see a multi-speed recovery in the region," said Philippe Le Houérou, World Bank Vice-President for the Europe and Central Asia region. "As a rule of thumb, the closer the countries are to the Euro area, and in particular to Southern Europe, the stronger they feel the impact, as their economies rely more on the Euro area as an export market and the main source of banking flows, foreign direct investments and workers’ remittances."

An uncertain environment and continued recession in the Euro area pose challenges to the ECA region through three channels: finance, trade, and workers’ remittances. Central and Eastern Europe (CEE)i and the Western Balkansii, which have the closest links to the Euro area, are considerably lagging behind Turkey and the Commonwealth of Independent States (CIS)iii.

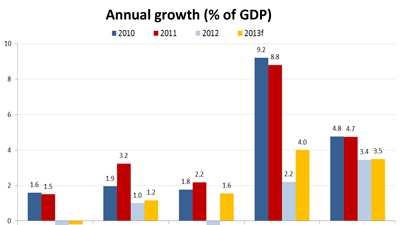

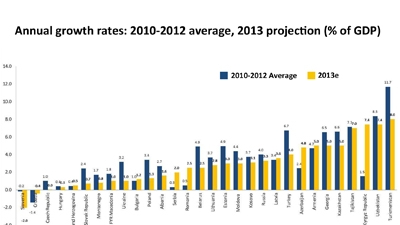

According to World Bank projections for 2013, countries of the CIS are expected to grow at about 3.5 percent and Turkey at about 4 percent, while in CEE and the Western Balkans growth will remain anemic at 1.2 percent, which is only slightly higher than 0.9 percent growth in 2012.

This multi-speed growth is reflected in fiscal and financial trends in the region.

Budget deficits have been shrinking (from 5.5 percent of GDP in 2008 to an average of 3.4 percent in 2012 in CEE; and from an average of 4.5 percent of GDP in 2008 to an average surplus of 0.3 percent in 2012 in the CIS), but the measures to bring about this fiscal adjustment have become increasingly difficult. Some of these adjustments became possible thanks to improved efficiency and better targeting of the social protection expenditures, which also helped prevent an increase in poverty in most countries.

Since the crisis, public debt levels have risen in most parts of the region, except for Turkey. Average public debt for CEE and the Western Balkans has increased from 28.3 percent in 2008 to 45.5 percent in 2012. Public debt is at potentially risky levels in several countries of the region (Hungary – 76 percent, Albania – 62 percent, Poland – 56 percent, Serbia – 54 percent, Croatia and Slovenia – 53 percent), and poses a heavy burden on public finances.

The financial sector in CEE and the Western Balkans has been weakened by deleveraging and growing non-performing loans (NPLs). Deleveraging accelerated again in 2012 after some slowdown in 2011, especially in countries such as Estonia, Hungary, Slovenia, Croatia, Latvia, and Serbia. NPLs decreased in CIS countries and Turkey, but continued to grow in the Western Balkans, Bulgaria, and Romania. In these conditions, credit issuance to the private sector has continued to decline in the Baltics and has stagnated in the rest of Central Europe, the Western Balkans, Turkey, and also in Belarus and Ukraine.

Unemployment and job creation

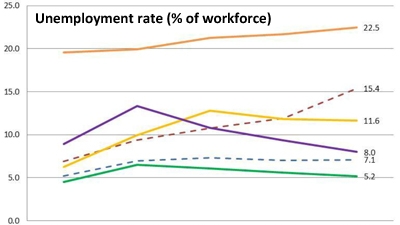

Job creation has been sluggish in the post-crisis recovery of the region. Unemployment remains stubbornly high in CEE and keeps rising in the Western Balkans, while slightly decreasing in the CIS and Turkey. Youth unemployment is of particular concern, as well as long-term unemployment, when people are unemployed for longer than 12 months.

Reducing unemployment is an urgent challenge for the ECA region and requires a mix of policy measures both in the short and long term. An upcoming World Bank report on jobs in the ECA region provides an analysis of the situation and makes policy recommendations to strengthen job creation.

The report establishes that employment creation in the ECA region was slow even before the crisis (2000-2007) when the region grew faster than other emerging economies. The report finds evidence that the countries that reformed early and have integrated into global markets, the so-called ‘advanced modernizers’, have been more successful in achieving greater employment creation than ‘late modernizers’, which have implemented reforms slowly or unevenly.

"Reforms pay off in the form of stronger and sustained job creation in the private sector and higher ability to translate entrepreneurship potential into successful creation of new businesses, but they do so with a lag," said Yvonne Tsikata, World Bank Sector Director for Poverty Reduction and Economic Management in Europe and Central Asia. She added that "Initially, economic restructuring means that jobs are both created and destroyed. As countries further integrate into the global economy, restructure enterprises, improve conditions for doing business, and modernize labor markets, job creation outpaces job destruction and this then translates into higher aggregate employment".

Ana Revenga, World Bank Sector Director for Human Development in the Europe and Central Asia region said that "Faster job creation will require changes in the social contract between workers, enterprises and governments. The policy agenda must focus on removing obstacles to entrepreneurship, helping education and training systems adapt better to fast-changing labor markets, facilitating labor mobility, and making pensions, social benefits, and labor regulations compatible with longer and more productive working lives. The right combination of specific policies will vary across countries, but the ultimate result is the same: more rapid creation of productive jobs."

To create jobs in ECA, the Bank recommends actions in three main policy areas:

- Resuming sustained growth: by ensuring macro fundamentals for economic recovery and regaining the pre-crisis reform momentum.

- Enabling private sector-led job creation: by eliminating impediments to business expansion and entrepreneurship.

- Preparing workers for new jobs: by helping workers acquire skills for the modern workplace and making formal work pay by removing disincentives and barriers to work.

_____________________________

i The Central and Eastern Europe (CEE) sub-region includes Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Slovak Republic, Slovenia, and Romania.

ii The Western Balkans sub-region includes Albania, Bosnia and Herzegovina, Kosovo, FYR Macedonia, Montenegro, and Serbia.

iii The Commonwealth of Independent States (CIS) sub-region includes Armenia, Azerbaijan, Belarus, Kazakhstan, Kyrgyz Republic, Moldova, Russia, Tajikistan, Turkmenistan, Ukraine, and Uzbekistan.