The survey, carried out across the sectors of agriculture, manufacturing, construction and trade, and services and tourism, was designed to assess the gaps in access to finance and help Azerbaijani authorities to identify policy reform priorities aimed at increasing MSME lending.

While Azerbaijani authorities have attempted to fill-in the private sector finance gap by launching various special lending and loan subsidy programs, including through the Entrepreneurship Fund and the State Agency for Agro Credit, only 5.1 percent of surveyed MSMEs applied to these programs and less than 1.7 percent actually benefitted from them.

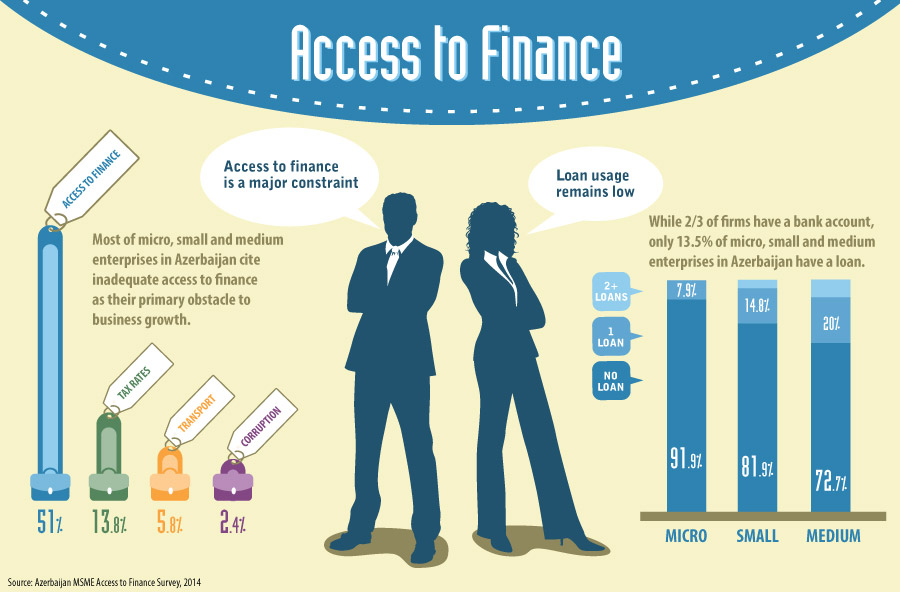

Complex credit application procedures, lack of collateral, high lending costs, and short maturities in the backdrop of low financial capability prevent MSMEs from accessing finance. While roughly two thirds of MSMEs currently own a bank account, only 14 percent have an outstanding loan or a line of credit. Around three quarters of MSMEs have never applied for either.

Very few MSMEs have access to other types of credit such as credit cards (2.4 percent) and overdrafts (0.3 percent), while letters of credit, trade insurance, leasing, and factoring remain rarely used, with only 4.1 percent and 1.7 percent of MSMEs using leasing and factoring in 2013, respectively.

Four factors in particular contribute to high financing constraints and low usage of credit instruments by MSMEs.

1. Inaccessible traditional loans

Complex application procedures, high collateral requirements, and high costs are discouraging to enterprises and generally result in loan rejections. Availability of longer term finance for more than 3 years also remains limited.

2. Limited development and Lack of awareness of non-traditional sources of financing

Letters of credit, trade insurance, leasing, and factoring are also limited by both supply and demand factors. Although two thirds of MSMEs are familiar with supplier credit and more than half actually received such credit in 2013, awareness or access to other products remains limited.

While 32 percent of MSMEs are familiar with leasing, only 5.8 percent sought this form of financing, and just 4.1 percent received it, in 2013.

3. Inadequate financial capability skills to secure financing

Less than half of MSMEs prepare financial statements, only a quarter prepare written business plans, and more than one third of MSMEs do not keep ongoing financial records at all.

Lack of reliable financial statements and low financial capability of MSMEs – both in understanding financial products and their benefits, as well as managing their finances – increases lending risks, weakens loan application credibility by MSMEs, and leads to higher loan rejection rates.

4. Limited impact of government programs on access to finance

Despite a high level of awareness of the Government programs, only 5.1 percent of surveyed MSMEs applied for state sponsored programs and only 1.7 percent received the support. There is room, therefore, to increase the scale and scope of Government support, while enhancing the design of the programs and products, expanding intermediation instruments and partners, and multiplying the impact through mobilization of private sector funds.

The way forward

A number of legal, regulatory, and institutional reforms can be taken by Azerbaijan’s government and its Central Bank to help lift the financing constraints that MSMEs face and ultimately enable them to contribute to Azerbaijan’s economic diversification and growth.

It is critical to undertake reforms aimed at reducing risks to lenders and at enhancing lenders’ skills and risk management practices in order to allow simplification and standardization of lending procedures. Reforms aimed at creating an efficient secured transactions framework for movable assets collateral and advancing credit reporting systems, with the introduction of a private credit bureau and development of clients’ credit histories, will help expand financing to smaller and younger MSMEs.

The depth and breadth of the financial sector needs to increase with the development of new financial institutions and more innovative products that will be tailored to serve the needs of different clients – especially MSMEs, including younger firms and those in rural areas.

A government MSME support strategy should be developed and access to finance programs should be streamlined to increase outreach, impact and targeting.

To address the low financial capability levels of MSMEs, particularly in new sectors and among agri-businesses, financial consumer protection and awareness programs need to be launched. In addition, there should be simplified business and financial training for MSMEs, through a dedicated and well-coordinated program of state support for SMEs and entrepreneurship.

{kind=link}