The latest MENA Economic Monitor Report - Spring 2016, expects Djibouti’s growth to rise to 7% in 2016-2018.

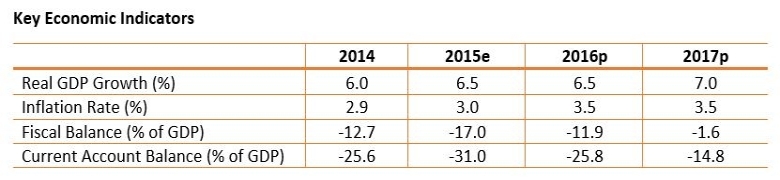

GDP grew at an estimated 6.5 % in 2015, up from 6 % in 2014 and 5 % in 2013. This growth acceleration was mainly driven by transport and port-related capital-intensive activities, such as transit trade with Ethiopia and transshipments, attracting large public and foreign investments. Despite the strong growth, inflation remained muted at 3 % in 2015 due to the stabilization of international food prices and a lowering of electricity tariffs for low-income households, combined with a low domestic demand due to high poverty and unemployment.

The primary fiscal deficit widened by 4.3 %age points in 2015 from 12.2 % of GDP in 2014; reflecting the high capital expenditures in port infrastructures development and construction projects while revenues remain subdued. The external deficit soared by 5.4 %age points in 2015 from 25.6 % of GDP in 2014 due to increased capital imports while exports remained depressed. External debt (mainly public) reached 66 % of GDP in 2015. FDI slightly declined to 8.5 % of GDP in 2015 from 9.1 % 2014. Djibouti has maintained sound international reserves over the past years, sufficient for the currency board coverage in the 2015-2020 horizon. Reserves are estimated at 350 million US dollars in 2015 (a coverage for 3.6 months of imports and 109 % of currency board). The banking sector remains weak with deteriorating loan portfolio of commercial banks and rising nonperforming loans (NPLs). The ratio of NPLs to total loans increased to over 22 % in June 2015 from 16.5 % in June 2014.

The medium-term outlook is favorable with strong growth spurred by the surge of public and private capital investment. Growth is expected to reach 7 % on average in 2016-2018. The fiscal deficit is anticipated to narrow to an average of 5.2 % of GDP in 2016-2018. This will result from a combined expectation that: (i) current investments will translate into higher revenues through new production and export capacity creation to offset the debt repayment burden, and (ii) the government engages in series of reforms to improve revenue mobilization. In addition, as major infrastructure projects near their end, government spending will also soften.

The current account deficit is expected to improve in the medium term, narrowing down to 14.5 % of GDP by 2018. This improvement is expected to be derived from the softening of capital imports related to construction projects while exports gradually pick up. FDI inflows and capital transfers should continue to finance the deficit. Inflation is projected to modestly accelerate by 0.5 %age point in 2016, spurred by housing and services sectors-stimulated demand. Reserves are expected to continue to guarantee adequate currency board and import coverage (of well over four months of import coverage), thus sustaining the peg of the Djibouti Franc to the U.S. dollar at 177.72 Djiboutian Franc/$1.

Despite the positive outlook, growth and macroeconomic stability remain subject to important risks. The main downside risks include delays in the construction and the lack of efficiency in the management of the new infrastructures, adverse economic events in Ethiopia, whose transshipment and trade transits account for more than 80 % of Djibouti’s port activities. Security developments in neighboring countries, or in the Red Sea, and domestic social and political instability due to the upcoming presidential elections could jeopardize growth.