Strategy

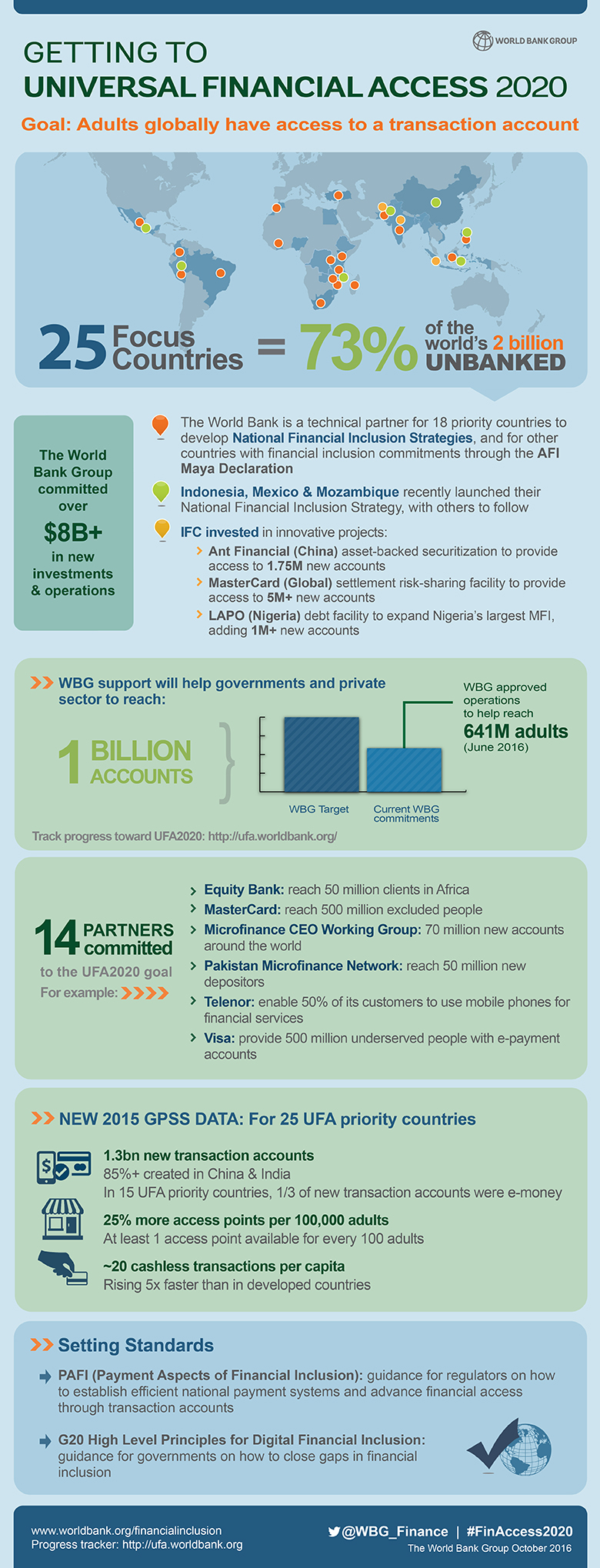

The UFA2020 initiative envisions that adults worldwide -- women and men alike -- will be able to have access to a transaction account or an electronic instrument to store money, send payments and receive deposits as a basic building block to manage their financial lives.

At the 2015 World Bank Group-IMF Spring Meetings, the World Bank Group and public and private sector partners adopted measurable commitments to achieve Universal Financial Access by 2020 (UFA2020) and help promote financial inclusion. Through the Universal Financial Access 2020 initiative, the World Bank Group – the World Bank and IFC – has committed to enabling 1 billion people to gain access to a transaction account through targeted interventions.

As of the end of December 2017, our advisory work, technical assistance financing operations and investments are projected to help reach 738 million new accountholders and we are on track to meet the goal of 1 billion by 2020..

We also work with more than 30 partners to catalyze private sector investment in financial inclusion. Leading financial service providers have set ambitious targets in line with the UFA 2020 goal.

While the UFA2020 initiative focuses on 25 priority countries where almost 70% of all financially excluded people live, we are working with more than 100 countries to advance financial access and inclusion. Our approach centers on:

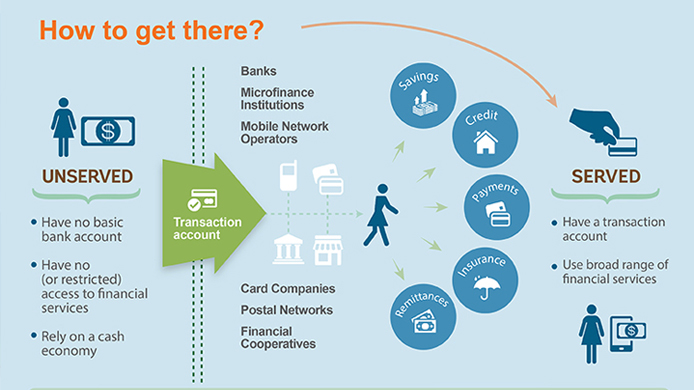

- creating a regulatory environment to enable access to transaction accounts

- expanding access points

- improving financial capability

- driving scale and viability through high-volume government programs, such as social transfers, into those transaction accounts

- focusing on reaching disadvantaged populations, such as women and rural producers

- encouraging use of financial services, to move from access to finance to account use

- working through critical value chains in priority countries to digitize payments, and creating access to other financial services such as savings, insurance, and credit

Platform approach includes three basic functionalities or layers – a biometric identity database, virtual payment addressing and digital payment interoperability.

National policies that provide scale through combinations of digital ID, digitized G2P payments.

Globally, we engage with standard-setting bodies to set recommendations and guidelines that will to advance access to transaction accounts.

The UFA framework for action is based on the Payment Aspects of Financial Inclusion (PAFI) framework, which was developed in 2015 a financial regulator taskforce chaired by the World Bank Group and the Committee on Payments and Market Infrastructures (CPMI).

In 2017, the G20 committed to advance financial inclusion worldwide and reaffirmed its commitment to implement the G20 High-Level Principles for Digital Financial Inclusion, which the World Bank Group helped develop under the China G20 Presidency leadership in 2016. The eight High Level Principles encourage governments to promote a digital approach to financial inclusion, and are being used as a reference tool by many countries.