In response to a request from Bank Al Maghrib (BAM), the Morocco's central bank, the World Bank has conducted a Financial Capability and Inclusion Survey in Morocco. Financial inclusion, financial literacy and consumer protection are high on the agenda of the BAM and Morocco's Ministry of Finance. The BAM has implemented many financial capability initiatives in recent years - from the promotion of a modern credit bureau helping prevent over-indebtedness to specific measures for transparency in bank services. The BAM, supported by the Ministry of Finance, is keen to initiate work on a national financial capability strategy. The completed survey provided key diagnostics to design such a strategy, set quantifiable and concrete targets, and assess effectiveness of the future financial capability enhancing programs. So far, this survey of financial capability has been the first in Morocco and one of the very few in the Middle East and North Africa (MENA) region.

The survey covered 4 main areas: Financial Inclusion, Financial Capability, Relationship between Financial Inclusion and Capability, and Financial Consumer Protection. The key findings are extensively addressed with actionable recommendations in the full version of the report. Here are the highlights:

1. Financial inclusion

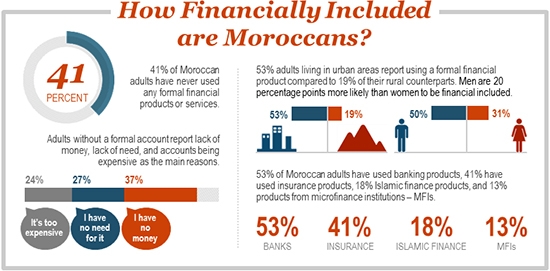

The survey indicates that 41% of Moroccan adults use a formal financial product or service, and this places Morocco well above the average level of financial inclusion in the MENA region and above the average among the lower middle income countries. However, within Morocco there are sharp variations in the use of formal financial services across different population segments. Bank accounts are used by 28% of the adult population, 21% of women, and only 10% of the low income citizens. Microfinance reaches only 5% of the adult population, although 68% report familiarity with it. Insurance is used by 24% of adult Moroccans, mainly due to mandatory coverage, and only 2% report using voluntary insurance. 18% of adults use Islamic finance. The most critical factors for improving financial inclusion in Morocco, according to the survey report:

- 24 percent of the Morocco's unbanked cite high costs as the main reason for not having a bank account

Recent research indicates that high costs of opening and maintaining accounts are associated with a lack of competition (Demirguc-Kunt and Klapper 2012). Allowing for robust competition among financial service providers stimulates innovation that helps expand the range of available products and lower their cost.

This 24% fraction also suggests that either the accounts costs are prohibitively high for much of the population or that the availability of cheap no-frills (basic) accounts is not widely known. International experience in countries such as India or the Philippines shows that the introduction of no-frills accounts must be complemented with public awareness campaigns to mitigate the risk that the uptake of these products may be very low. Therefore, additional research should be conducted to understand why BAM's efforts to promote availability of no-frills accounts and other basic financial services is not very effective. - 53% of adults living in urban areas report using a formal financial product compared to 19% for their rural counterparts. 61% of adults with higher incomes (top quartile of the income distibution) and only 25% of those with low incomes (bottom quartile) are financially included. Men are 20% more likely to be financially included than women - 50% vs 31%.

Despite banks' efforts to extend products and services to low-income clients, the survey data indicates a lack of suitable products for large parts of the population. Sustainable provision of a wide range of financial services for the poor, rural dwellers, and women - the most underserved segments of the population - will have the greatest effect on financial capability and inclusion in Morocco. Insurance and savings products have the greatest potential to reduce vulnerability of the financially underserved Moroccans to economic and social shocks.

Mobile or agent banking can dramatically reduce the costs of delivering financial services, in particular in low-density and remote areas. It can reduce not only account costs for the 24% of the excluded but also opportunity costs for the 37% with low incomes (see the key findings leaflet). Branchless banking based on modern technologies offers the potential to further expand the coverage of financial services and to reach the poor, rural dwellers, and women.

Evidence from Indonesia shows that even though men and women are equally likely to have savings accounts, males are more likely to be motivated to have an account in order to obtain a formal loan, whereas women are more likely to be motivated to have an account to save for future needs. In relation to insurance, Indonesian women are shown to purchase more often education insurance as compared to their male counterparts who prefer life insurance, and to a less degree, asset insurance. The inclusive financial sector policies should take into account the possibility of substantial differences between men and women's access, needs, and preferences in financial services.

2. Financial capability

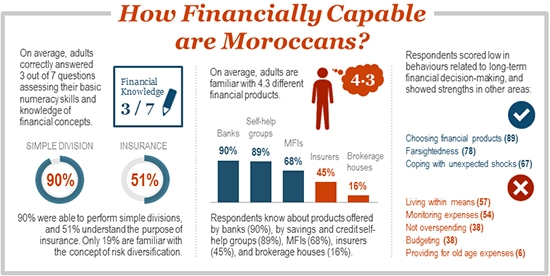

Like in many countries around the globe, in Morocco the popular knowledge of basic financial concepts is fairly low. While 90% of Moroccans can perform simple divisions (global average), only 40% understand how inflation affects their savings (below global average), and only 20% can solve slightly more difficult numeric tasks to identify better bargains. The average Moroccan is familiar with 4.3 financial products from the most common providers: banks are familiar to 90% of adults, savings and credit self-help groups - 89%, microfinance instititions - 68%, money transfer operators - 65%, insurance products - 45% of all adults and only 20% in the rural areas where insurance is especially useful to smooth seasonal income fluctuations. International comparison shows that Moroccans are becoming competent in choosing financial products, but they still struggle with managing daily expenses and retirement savings. The survey report addresses the following financial capability priorities with recommendations:

- Financial literacy, skills, and awareness of financial products are quite unevenly distributed in the Moroccan society, and especially lag behind among the rural Moroccans, youth, unemployed, and those who never finished primary school. Managing daily finances and long-term financial commitments are the skills most Moroccans need to improve.

TV usage in Morocco is almost universal, making TV an effective channel to reach remote populations and those who are the least familiar with financial concepts and products. Capturing attention of the adult audience and boosting their financial knowledge and skills requires innovative and interactive awareness and education campaigns, using edutainment in particular. Various kinds of TV shows with edutainment content have been quite popular in Kenya, South Africa, Mexico - people identify with the characters, enjoy the stories, and benefit from the financial capability enhancing messages. Morocco is well positioned to develop financial awareness, literacy, and skills among its broad population by offering high quality edutainment content in the popular categories of its national TV shows.

Around the world conditional cash transfers have been shown to affect people's investments in health and education. Social cash transfers in Morocco (e.g., Tayssir program), if financial education can be integrated, can encourage development of financial skills among beneficiaries and their families - to manage their daily finances and plan for old age expenses. Longer duration of these programs sustains long-term behavioral change. Likewise, public works programs may provide another excellent avenue to close financial knowledge gaps and promote desired behaviors among the most vulnerable. - Morocco's public education system provides little, if any, financial education

Opportunities for school-based financial education programs need to be explored, as awareness of the basic principles of financial capability has the most lasting impact if it is acquired at a young age. Even children greatly benefit from understanding such basics as budgeting, separating needs from wants, ability to refrain from overspending, as well as savings or making provisions for the future and old age. Successful school-based education programs are interactive and offer content that is relevant to student's lives in the present or near future. High-quality material or textbooks are therefore required, and teachers need to be trained accordingly. Since education resources may well be scarce, it is be the best to start with one or two subjects over three or four consecutive academic semesters, and - eventually and ideally - integrate financial education into a variety of existing subjects including math, economics, or social studies rather than adding a new subject into the curriculum.

3. Relationship between Financial Inclusion and Financial Capability

The formally included Moroccans who save and borrow from formal sources are more aware of various financial institutions and their products than the formally excluded who tap into informal sources or do not save or borrow at all. Awareness levels of financial concepts are similar among both the formally included and excluded. Financial behaviors are also also similar - both formally included and excluded segments experience difficulties with respect to managing their day-to-day finances and planning for old age expenses.

- Moroccans with the experience of using products from the formal financial institutions exhibit insignificant financial awareness and skills advantages compared to their formally excluded citizens

Financial education programs could be tied to the existing formal financial products that most people can access and use. When opening a bank account, taking out a loan, or concluding a mandatory insurance policy, users of financial services can receive free and easy to understand information to enhance their understanding of financial concepts and skills - relevant to both the current transaction and their future financial needs and options. The educational materials can range from the guides to set up a budget and monitor daily expenses to advisory materials on building up savings for seasonal shocks and long-term retirement plans. It needs to be ensured that all educational materials be informative, clear, impartial, and free from marketing. - Financial service providers in Morocco do not systemically offer products that are designed to promote financial capability among their customers

BAM may consider encouraging the financial service providers to offer profitable products that are designed to help their clients and underserved segments of the population to meet their long-term savings goals. Since the large majority of the population seems to struggle with daily budget management and long-term financial planning, it could make good business sense for financial service providers to develop products that meet the needs of their clients and underserved populations. For instance, they could develop micro-pension products or savings products with long-term savings goals. Such products would provide special accounts where fixed amounts of funds are deposited and access to cash is relinquished for a period of time or until an explicit savings goal has been achieved - for example, to establish or expand of a business, purchase a car or house, finance education, or save for retirement.

4. Financial Consumer Protection

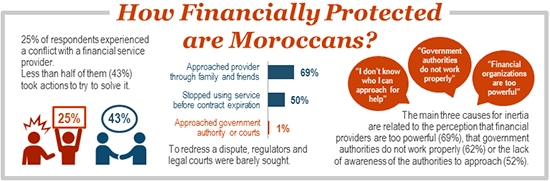

With 43% satisfaction rates, banks in Morocco trail other financial service providers in client satisfaction. Savings and credit self-help groups, money transfer operators, money exchange offices, and MFIs are viewed by 70% of their clients as meeting the clients' needs. High incidence of conflicts with the financial service providers and high post-conflict service rejection rates, especially among women and rural dwellers, signal need for urgent attention to the regulatory measures for financial consumer protection.

- 25% of Moroccans reported having experienced a conflict with a financial service provider, a much higher rate than in the few countries where a comparable indicator is available. Only 43% of Moroccans who faced a dispute took actions to try to resolve it, in 69% of cases subsequently asking their relatives, friends, or community elders to step in and help find a solution outside of the legal or regulatory system. Following a dispute, 50% of Moroccans stop using services before their contract expires.

Financial education initiatives needs to be complemented by stronger financial consumer protection framework, including regulations in the area of consumer disclosure. This would level the playing field between suppliers and consumers of financial services. Consumers should be able to obtain sufficient information that allows selecting the most affordable and suitable financial products. In line with the recommendations of the World Bank's Good Practices for Financial Consumer Protection, financial service providers should therefore be required to provide a standardized 'key fact statement' that explains in plain language the key terms and conditions for each product and includes options and contacts for conflict resolution. Pilot tests can help ensure completeness of information and that consumers properly understand it. The conflict resolution information should be disclosed not only in the products’ terms and conditions but also be visibly posted in branches and online. Consumers should be informed about that formal redress systems such as BAM or legal courts that can be approached in the event of a dispute with a financial service provider.

Given the high rate of reported conflicts , BAM should analyze consumer complaints statistics and use this information to enhance supervision and regulation. BAM's existing formal system of redress All financial institutions and banks in particular should be obliged to share their complaints data with BAM. Based on the analysis of complaints and inquiries, BAM could propose guidelines, instructions or conduct public awareness campaigns that address the main problems identified in such analysis.

Since the trust among the users of financial services in the formal conflict resolution methods is so low at just 31%, BAM should consider re-visiting its existing formal system of redress in order to quickly and effectively resolve disputes that are not resolved by financial providers' internal complaints procedures. More user-friendly and relevant formal redress systems that provide on alternative or backup dispute resolution option for consumers can help significantly reduce the incidence of conflict and improve the quality of resolution. BAM should clearly explain to consumers its role in market conduct supervision and consumer protection. - Moroccans report much lower satisfaction rates of 43% when using financial services provided by the banks, as opposed to 70% satisfaction with the other types of providers.

Additional research is necessary to understand why banks are struggling to satisfy their customers. Mystery shopping and focus group discussions are the primary ways to gather definitive information on the issue.