The DE4LAC assessments will take stock of existing digital economy initiatives and identify reform and investment opportunities to accelerate the transition to an inclusive digital economy.

The DE4LAC assessments will follow the digital economy framework that includes six pillars:

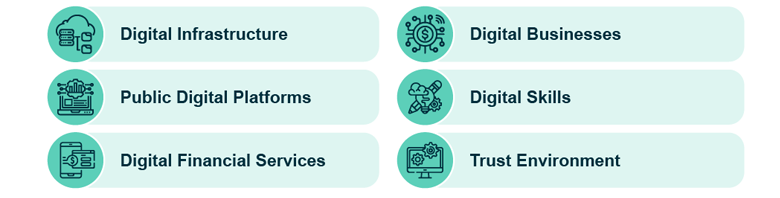

Digital Economy Foundations- 6 Pillars

- Digital Infrastructure: Availability of affordable, high-speed internet, which is instrumental to bringing more people online. Digital infrastructure provides the essential input for people, private and public sector to get online, and untap the value of digital services. Broadly, digital infrastructure consists of connectivity (such as with high-speed internet and internet exchange points), internet of things (such as with mobile devices, computers, sensors, voice-activated devices, geospatial instruments, machine to machine communications, vehicle to vehicle communications), and data repositories (such as with data centers and clouds). For the digital economy to flourish, users’ access to a meaningful connectivity plays a key role.

- Digital Platforms: Presence and use of digital platforms that can support greater digital exchange, transactions, and access to public and private services online. Digital platforms offer products and services, accessible through digital channels, such as mobile devices, computers, and internet, for all aspects of life. Their role of intermediary between one or more parties can be covered by both public and private subjects. Digital public platforms, offered by government and public institutions, can serve people and government agencies in all aspects of life, such as healthcare, education, government business or services. Examples are digital ID systems, online facilities to pay taxes, etc.

- Digital Financial Services: Ability to pay, save, borrow, and invest through digital means supports financial inclusion by removing geographic and market barriers. Digital financial services provide individuals and households with convenient and affordable channels by which to pay, as well as to save and borrow. Digital payments are often the entry point for digital financial services and provide the infrastructure for additional products, and use-cases can be developed. A digital financial services ecosystem requires forward-looking and proportionate legal and regulatory frameworks allowing market entry and innovation, robust financial infrastructures supporting fast and interoperable payment infrastructures, and development and deployment of low-cost delivery channels through agents, point of sale devices, and mobile phones.

- Digital Business: Presence of an ecosystem that supports new and established firms’ growth to drive employment and innovation. Digital businesses, which comprises two categories: 1) Digital start-ups and 2) Established digital businesses, represent a unique opportunity for developing economies to boost productivity growth, generate more jobs, and promote integration of lagging populations and regions. For growth and proliferation of digital businesses, government should ensure that the enabling regulatory environment is set in place, while keeping in mind distortions that may arise as adoption increases.

- Digital Skills: Development of a tech-savvy workforce, with basic and advanced digital skills to support innovation and employment. Economies require a digitally savvy workforce to build robust digital economy and competitive markets. Digital skills constitute technology skills, together with business skills for building or running a digital start-up or enterprise. Greater digital literacy further enhances adoption and use of digital products and services amongst governments and the larger population

- Trust Environment: Presence of a governance framework balancing data enablers and safeguards, and supporting digitalization while protecting the individuals, businesses, and institutions from cybersecurity risks. To improve trust in digital transactions, it is critical to enhance data protection regulations, cybersecurity capabilities, and the digital ID system. Particularly,

- Data protection: Data protection regulation could significantly improve the trust environment, enabling the development of digital financial services and digital businesses

- Cybersecurity: Growing digitalization around the world is exposing states, economies, and societies as a whole to new and more significant cyber risks. Digital technologies underpin personal lives and business activities across many sectors, cybersecurity must become an integral part of the overall digital ecosystem.

- Cybersecurity governance structure

- Effective national level computer emergency response to combat cybercrime

- Cybersecurity professionals

- Digital ID: The ID system provides an effective means of enabling access to digital services

Five cross-cutting themes

The digital economy framework also includes five cross-cutting themes:

- High levels of concentration and anti-competitive market practices in key sectors and the consequent impacts on access, affordability, and quality of digital services

- LAC-specific social and economic exclusion dynamics, for example high rates of inequality and exclusion among indigenous, Afro-Latino, and migrant populations

- Calibrating the role of the State across all the pillars of the diagnostic

- Environmental considerations, including internet pollution, greening of the financial sector and the role digital technologies can play in the implementation of the green agenda

- Digital technology risks including related to cybersecurity, data protection, social exclusion, and dominance of Big Tech

- Constraints and opportunities revealed by the Covid-19 pandemic, for example related to e-commerce, digitization of emergency social transfer payments, shift towards e-platforms for education, etc.