The Country Policy and Institutional Assessment (CPIA) for Africa is an annual diagnostic tool for Sub-Saharan African (SSA) countries eligible for financing from the International Development Association (IDA), the part of the World Bank that supports the world’s poorest countries. The CPIA Report aims to capture the quality of each country’s policies and institutional arrangements, focusing on the elements within the country’s control. The scores are designed to assess sustainable growth and poverty reduction supported through existing frameworks (in 16 criteria around four clusters).

The CPIA provides scores for each country, and an overall regional score, on a scale of 1 (lowest) to 6 (highest) in four areas: economic management, structural policies, social inclusion and equity policies, and public sector management and institutions. The scores inform governments of the impact of each country’s efforts to support inclusive growth and poverty reduction. The overall score helps determine the size of the World Bank’s concessional lending and grants to low-income SSA countries. The report includes scores for 39 IDA-eligible countries and acts as a touchstone for country monitoring and regional best practices.

Looking back at 2022, the political and institutional focus was again dominated by unprecedented international events. Following two years in which policy priorities reacted to the COVID-19 pandemic, early 2022 offered some hope that countries could shift back to long-term priorities for development, including addressing the urgent need for climate-change resilience. However, global events continued to deeply affect SSA countries. The ongoing war in Ukraine, supply chain constraints, and 2022 COVID-19 restrictions in China—as well as poor harvests in some countries—led to significant food and energy price shocks. Accordingly, SSA countries experienced varying changes in their CPIA scores, with the stable average score masking some of the larger trends.

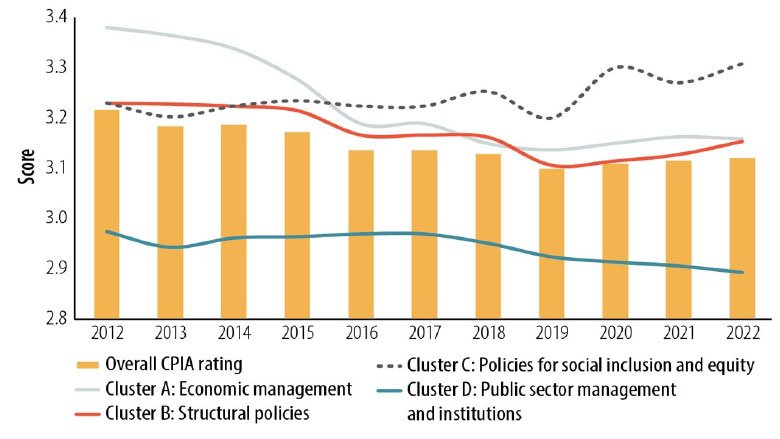

No. 1 - More countries in Sub-Saharan Africa saw improvements in their overall CPIA scores compared to 2021

Despite new international challenges, poor harvests, and price shocks of 2022, more countries in Sub-Saharan Africa saw improvements in their overall CPIA scores compared to the previous year. Nevertheless, the average overall CPIA score for the 39 SSA countries assessed stayed stable for 2022 at 3.1, as slight improvements in social inclusion and structural policies (clusters B and C) were offset by stagnation in economic and public sector management (clusters A and D).

Evolution of Regional Score and Trends over time

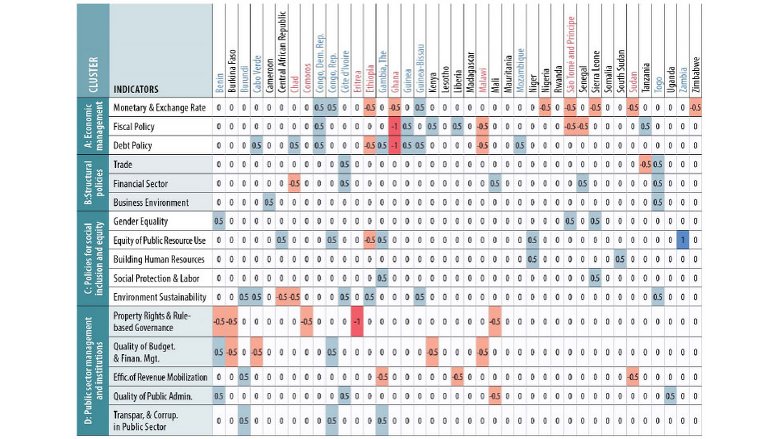

No. 2 - Economic management, social inclusion, and governance clusters were critical areas for score changes

The economic management, social inclusion, and governance clusters were critical areas for score changes, reflecting policy performance and institutional challenges. High debt levels, inflation, and tightening financial conditions presented economic stability and growth risks, indicating the need for improved fiscal management and structural reforms.

Twelve SSA countries registered improvements in their overall score, compared to seven the previous year. The overall score increased by 0.1 point for 11 countries—Benin, Burundi, Cabo Verde, Côte d’Ivoire, the Democratic Republic of Congo, The Gambia, Guinea, Guinea-Bissau, Mozambique, the Republic of Congo, and Zambia—while the score for Togo increased by 0.2 points. In contrast, the overall score decreased for eight countries—Chad, the Comoros, Eritrea, Ethiopia, Malawi, São Tomé and Príncipe, and Sudan each decreased by 0.1 points, and Ghana decreased by 0.2.

For the most part, countries receiving downgrades were positioned toward the lower end of the scale, while countries receiving upgrades were positioned toward the upper end, indicating a growing divergence in scores across the region.

CPIA 2022 Changes in Scores at a Glance

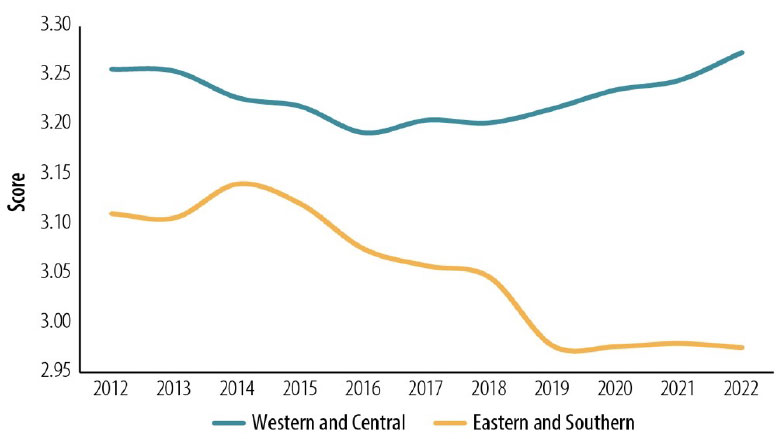

No. 3 - The gap between Western and Central Africa and Eastern and Southern Africa continues to grow

The gap between subregions grew, as Western and Central Africa (AFW) continued its upward trend, improving slightly from 3.2 to 3.3, while Eastern and Southern Africa (AFE) remained unchanged at 3.0, roughly even with its 2019 average. In AFW, the overall score increased for eight countries, compared to four countries in AFE. AFW’s overall scores have recovered from the falls that followed commodity price decreases in 2014–15, while the average CPIA scores for AFE continued to decline up to 2019 and have remained depressed since. Macro-fiscal management is a crucial factor contributing to this gap, with AFW consistently outperforming AFE in economic and public sector categories.

Evolution of AFE and AFW over time

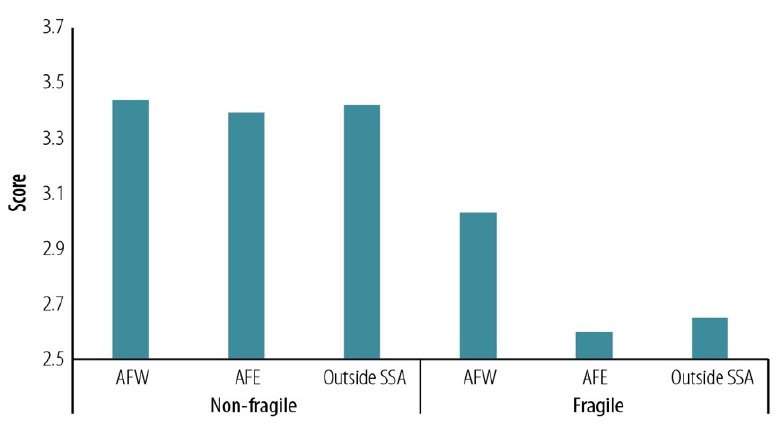

No. 4 - Differences between subregions can be partly attributed to Fragile and Conflict States

Most of the differences between subregions can be attributed to fragile and conflict situations (FCS), where countries experience high levels of social fragility. AFE exhibits a wider range of scores, from 1.6 to 4.1, compared to 2.5 to 3.9 for AFW; the highest scoring country, Rwanda, is located in AFE. The divergence between subregions can be largely attributed to the impact of repeated crises and shocks in a handful of countries: The four lowest-scoring countries—South Sudan, Eritrea, Somalia, and Sudan—are located in AFE and continue to experience conflict and fragility. The average score for AFE without these four FCS states is almost identical to the score for AFW. In contrast, FCS states in AFW performed relatively well, driven largely by improved performance in economic management scores (Cluster A). One contributing factor could be the prevalence of currency unions in West Africa—the West African Economic Monetary Union (WAEMU) and Communauté Économique et Monétaire de l'Afrique Centrale (CEMAC), or the Economic Monetary Community of West Africa.

CPIA scores by fragile and conflict state status

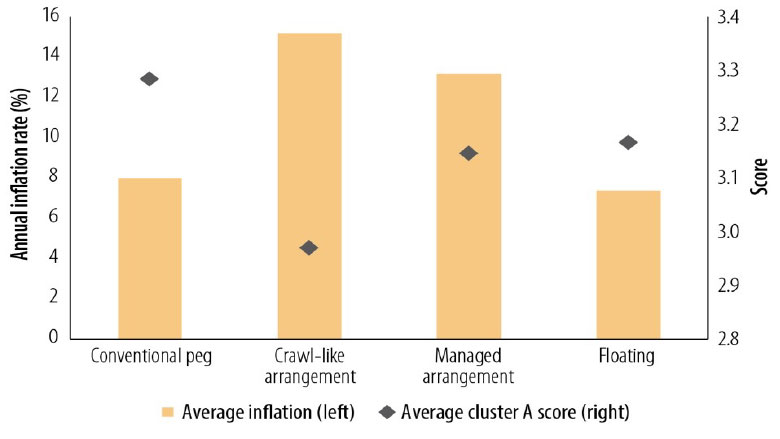

No. 5 - Members of the monetary unions have shown resilience against high energy and food prices

Countries with currency pegs, notably members of monetary unions, maintained lower inflation levels and stronger economic management scores than their peers in the region.

As the region is home to diverse exchange regimes, managing the volatility of exchange rates and inflation is a key concern for policymakers. In 2022, exchange rates in many countries in the region depreciated, making imported goods, including food and energy, more expensive and contributing to elevated inflation rates. However, countries with fixed exchange rates sustained relatively low inflation at an average of 8.0 percent for 2022. Similarly, those that employed a floating exchange rate regime (Madagascar, Somalia, and Uganda) also maintained inflation at an average rate of 7.4 percent. In contrast, countries using crawl-like pegs or actively managed exchange rates experienced double-digit inflation, averaging 15.2 and 13.9 percent, respectively, in the same year. This difference in performance on inflation could partly be attributed to costly fiscal measures used to limit exchange rate pass-through to inflation. While aiming to mitigate inflationary pressures, such measures could lead to fiscal deterioration, add stress to the exchange rate, and ultimately exacerbate inflationary pressures.

This site uses cookies to optimize functionality and give you the best possible experience. If you continue to navigate this website beyond this page, cookies will be placed on your browser. To learn more about cookies, click here.