Turkey Economic Monitor 6: Sailing Against the Tide

Turkey Economic Monitor 6: Sailing Against the Tide

The World Bank, February 25, 2022

Turkey experienced an accelerating economic recovery in 2021 amidst the COVID-19 pandemic, but also rising macro-financial volatility, with impacts on households.

In the recovery, the economy grew 11.7 percent year-on-year in the first three quarters of 2021 supported by external and domestic demand; the external and fiscal balances improved, and unemployment fell.

However, the Lira depreciated to record low levels in the fourth quarter in 2021, losing over half its value by early December before appreciating but remaining volatile.

Following the reopening and loosening of restrictions, Turkey entered the fourth wave of infections, driven by the Delta variant, in early July 2021. The expansion of COVID-19 cases in the second half of 2021 followed a similar path to many European countries and the United States.

The recent surge in cases has not led to reintroduction of stringent measures thanks to low fatality rates. An accelerated vaccine rollout helped Turkey’s fully vaccinated adult rate to rise to over 84 percent as of January 2022.

The COVID-19 pandemic amplified existing income and labor disparities. The regional inequalities of the Covid-19 crisis also manifested in larger impacts for women from Eastern regions, widening pre-existing gender gaps.

Following very high growth in 2021, Turkey’s economic growth outlook is beset by macro-financial uncertainty. As in 2021, growth in 2022 is expected to be largely driven by a continued strong rebound in exports. The composition of growth is projected to continue shifting towards external demand. Net exports are expected to drive more than two thirds of growth in 2022.

On the production side, the services sector is expected to increase its contribution to growth in 2022-23. The services sector would generate around two thirds of the growth in 2022, on the back of the strong recovery in the tourism sector.

Vaccine challenges may undermine good vaccine progress to date; continued Lira depreciation and high inflation may further exacerbate macro financial vulnerabilities, erode real incomes, distort price signals, and disrupt production and supply channels. High inflation also poses a risk to Turkey’s progress on poverty reduction.

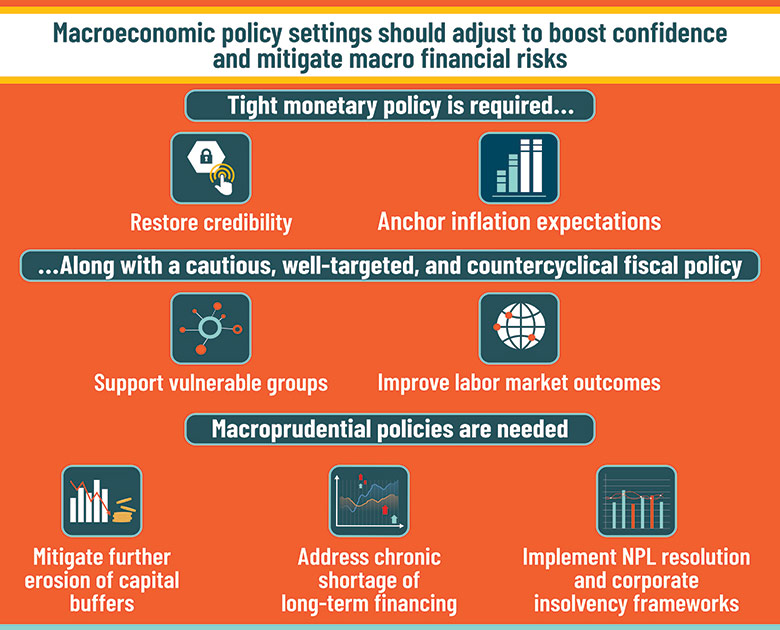

Macroeconomic policy settings should adjust to boost confidence and mitigate macro financial risks. Further monetary policy loosening will likely continue widening external and internal imbalances. Tight monetary policy effort is warranted to restore investor confidence and anchor inflation expectations.

Policies should also focus on supporting vulnerable groups and improving labor market outcomes. The rapid recovery in economic activity in 2021 has helped reverse the pandemic’s impact on employment, but underlying challenges have resurfaced. There is a greater need to stimulate the demand for labor and increase the inclusion of women and vulnerable youth including those not in employment, education, or training (NEET).

A focus on improving Turkey’s longer-term global competitiveness is also needed as the country has not been attracting as much foreign direct investment (FDI) as in the past or compared to other emerging markets. Good quality FDI, which is productive and higher tech, is important for countries like Turkey that aim to catch-up to high income levels.

Turkey would also do well in anticipating and preparing for the impacts of the EU’s Carbon Border Adjustment Mechanism, which will affect Turkish exports to the EU.

The World Bank, April 27, 2021

The World Bank, August 11, 2020

The World Bank, November 2019

The World Bank, December 2018

The World Bank, May 2018

Tunya Celasin

(495) 745-7000

Email