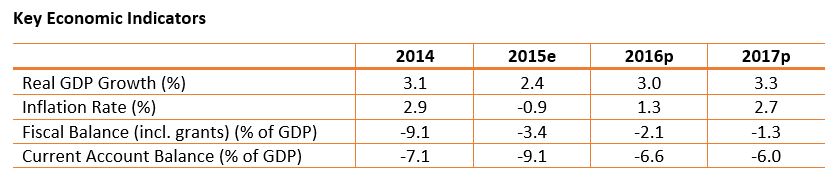

The latest MENA Economic Monitor Report - Spring 2016, expects Jordan’s growth to improve to 3 % in 2016, assuming no further worsening in the regional security situation and associated spillovers.

GDP growth moderated during 2015 to an estimated 2.4 %, the slowest pace in four years, magnifying already-high unemployment. Security spillovers from regional conflict worsened, negatively impacting tourism, construction, investment and trade. However, growth in a number of sectors held up well through the third quarter of 2015, including in finance and insurance services, transport, storage and communications, electricity and water, and mining and quarrying. Unemployment rose to 13.0 % in 2015, an increase of 1.1 %age points relative to 2014. There was a mild deflation for most of 2015 due to further falls in global oil prices, a weakened Euro, a negative output gap, and easing of supply side pressures experienced in previous years (notably on housing prices, due to the large influx of refugees in 2012-13). Monetary policy remained expansionary with the central bank reducing the key policy lending rate by 125 basis points during the course of 2015. International reserves slightly rose to $ 14.2 billion (7.5 months of imports) by end-2015.

The fiscal deficit was narrower in 2015 thanks to lower expenditures and lower transfers to the National Electric Power Company (NEPCO), which outweighed the fall in domestic revenues and grants. NEPCO resorted to borrowing from commercial banks instead of the government in 2015 providing a 7.0 % of GDP relief to the fiscal balance, without which the fiscal deficit would have widened. NEPCO’s debt continues to be government guaranteed and combined with the fiscal deficit and slowing GDP growth contributed to pushing the gross debt to GDP ratio to an estimated 93 % at end-2015.

The current account deficit is expected to have widened in 2015, mainly due to lower public transfers and a 7.1 % fall in tourism receipts, and despite a narrowing trade deficit. The merchandise trade balance narrowed by 14 % on account of a 40.4 % fall in energy imports. These outweighed a 7.1 % contraction of direct exports (themselves buttressed by 10.9 % growth in phosphate exports) affected by land trade route closures with Syria and Iraq, traditionally Jordan’s largest export partner. Remittances are slowing, growing by only 1.5 % during 2015.

Growth is expected to improve to 3.0 % in 2016, assuming no further worsening in the regional security situation and associated spillovers. This is driven by an expansion in mining and quarrying sector and positive base effect of tourism and construction sectors. Jordan is working towards an Extended Fund Facility (EFF) with the IMF. The EFF is anticipated to support further fiscal consolidation efforts in parallel with growth-enhancing and job-creating structural reforms. The baseline growth forecasts assume agreement on an EFF leading to a fiscal adjustment and a lower debt-to-GDP level. The balance of risks is on the downside. Managing repercussions from the regional security and political situation is a key risk in addition to the challenges of hosting a substantial number of Syrian refugees. Additionally, persistently low oil prices are a risk this year and in the medium term, given their potential impact on remittances, exports, FDI and grants from the GCC. Fiscal adjustment measures are likely to be difficult. Furthermore, the willingness and speed of reform implementation particularly to improve the business climate will be crucial to meet the country’s investment aspirations.