Second, logistics has a direct impact on poverty.

The poor farmer that produces pineapples in Costa Rica only receives 10 percent of what the same pineapple is sold for in Saint Lucia—and 60 percent is absorbed by logistics costs of all kind. If logistics costs could be lowered, the farmer could get a larger share, the consumer would benefit by lower prices, the logistics industry by higher wages, and undoubtedly production of pineapples would increase due to expansion of the market.

Logistics costs are indeed a double-edged sword: on the one hand, logistics are a source of income and employment and a necessary ingredient in the global supply chains we all benefit from.

At the same time, many of the costs incurred in the supply chain are unnecessary: they are time lost in traffic jams, congested harbors or inefficient transport interchanges; they are financing costs incurred due to long storage of good in inefficient supply chains; they are costs at the border: inspection fees, tariffs and bribes. And are the costs of empty containers or empty ships that return to their place of origin because the transporter could not secure a return load.

From the data we have—and these data are quite scarce, on average logistics costs make up some 13 percent of GDP. In the most efficient countries, such as the United States and the Netherlands—my home country, those costs are around 8 percent, whereas in the least efficient countries they can be as high as 25 percent.

China, at 16-18 percent, is not as efficient as OECD countries, mainly because of inefficient domestic logistics. This despite the relatively high score on the Logistics indicators, which measures international logistics. Note that these data are some 4-5 years old, and the most recent information suggests that logistics costs in China are now below 15 percent. I am convinced that many in this room today are seeking ways to further optimize China’s domestic logistics, and this number will continue to decline. However, it is unlikely to go as low at the USA’s any time soon, simply because China’s manufacturing, which is logistics intensive, has a much higher share in GDP than in most countries.

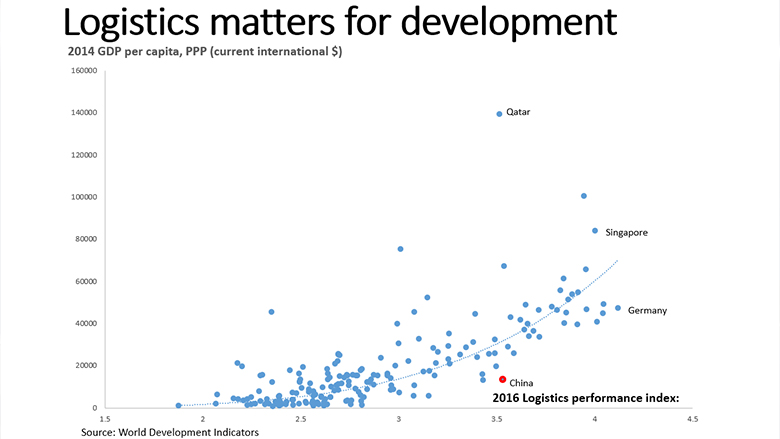

Not surprisingly, logistics costs are strongly (inversely) correlated with the Logistics Performance Indicator.

The statistics on Third Party Logistics or 3PL—which measures the part of logistics that is outsourced-- suggests that third party logistics is the most efficient approach. But policies, legal environment, and risks get in the way—especially in developing countries.

For example, in China in the past, a major impediment for third party logistics was that manufacturing and services were taxed in different ways—the former with the business tax, the latter with Value Added Tax. With the integration of the two, I foresee strong growth in Third Party Logistics in the years to come.

So what is the future of global logistics?

As the saying among economists goes “Predictions are hard, especially if they concern the future”

But the past can teach us something about the drivers of change.

What I take from history is that there are three driving forces in global logistics: Economics, Technology, and Policies. Allow me to illustrate:

Perhaps the very first intercontinental logistics route was the silk route, which finds its origin in Roman times. At the time, there were two big trading blocs—China and the Roman Empire, so it was only logical that trade between the two emerge. But it did not flourish—fragmentation, roving bandits and the means of transportation in between the two empires—camels and horses-- prevented large trade volumes to emerge.

The heydays of the Silk Route came during the Mongol Empire, which stretched from China to the Mediterranean, which provided a relatively safe passage, and backed it up by a postal service that spanned the Khan’s territory.

Competition from the Arab Dhows reduced the importance of the Silk Route over time, and Arabs became the main traders of goods between East and West. The Italian city states controlled the Mediterranean Trade and beyond—backed by two major commercial innovations: the letter of credit and double-entry bookkeeping.

By the late 14th century, though, the expanding Ottoman empire disrupted this East-West trade through Mediterranean and Arab sea, and it was the Portugese in the 15th century that had the courage to undertake the long and perilous journey around Africa—and with their Caravel ships, the technology to match. These were still hopelessly clumsy, but could make their way to the East—while hugging the coast of Africa and then picking up the old Arab trade routes across Asia.

The economics of this journey was overwhelming: profit margins of 1000-1500 percent on spices and other goods from the East made the risks and disease and violence along the journey acceptable.

The Portugese were soon overtaken by the Dutch, and later the British. International trade thrived because of another commercial innovation—the joint stock company, which allowed the spreading of the considerable risks involved in international trade among many parties.

Holland became the richest nation on earth as a result of it. And by some estimates, the Dutch East India Company, the first truly multinational logistics company, became the largest company in history by valuation, larger than Apple today.

China was surprisingly absent in this growing global trade—due to a policy decision. By the 15th century it was the largest economy in the world, and the richest nation. Admiral Zheng He had explored the cost of India and Africa, and shipping technology was far more advanced than in the west. However, the Ming dynasty banned shipping with the infamous Haijin edict, and China did not play a major role in global trade for another 5 centuries.

Major technological breakthroughs in the 19th century paved the way for the first golden age of globalization—and I mean “golden” for the west, not necessarily the East. They were the steamboat, the train and the telegraph—which together transformed the efficiency, reliability and timeliness of communication and shipping.

The steamboat turned the hazy and dispersed shipping routes that were literally all over the map, determined as they were by the wind, into straight lines from A to B on the map.

Infrastructure was another technological game-changer—the Suez Canal and the Panama Canal meant a major reduction in travel time from the East Coast the West Coast of the United States and from Europe to Asia. They practically eliminated trade around Africa and Latin America.

Today’s hyper-connected world is in many ways the extension of the inventions of the past—but put on steroids by the internet and aviation, and by a post-world war II economic order that allowed nations that opened up—such as China—to thrive.

Indeed, China is now the center of global trade—and by implication of global logistics. China is the second largest economy of the world, the largest manufacturer and the largest exporter in the world—and the country has the infrastructure to match—some 10 out of the 15 largest harbors in the world are in China—with Shanghai at the very top.

So what does history tell us for the future?

It tells us there are three main drivers of global trade and logistics—economics, technology and policy.

It was the economics of the letter of credit, the joint stock company, and the great wealth, the silk and the spices of the East that drove global commerce.

It was the technology of the Dhow, the steam boat and telex, and the Suez Canal that drove global logistics in the past.

And it was the policies of the Mongols, the British empire and the WTO that spurred globalization and global value chains.

So what does this imply for the future of global logistics?

Let’s have a look at the future of each of these drivers.

The biggest economic trend of this century is the shift of economic gravity towards Asia—or some would say, the re-emergence of Asia as the global economic powerhouse it used to be.

The consuming middle class is rising rapidly in those countries—300 million in China alone, and a rapidly growing number in India, Indonesia, Vietnam and Bangladesh.

This means that emerging economies are becoming origin as well as destination for a large share of the World’s manufacturing. This implies a greater need for intraregional infrastructure, transport, travel and logistics. Freight intensity will decrease with Asia’s countries moving to higher value goods manufacturing—with labor intensive industries moving to South Asia first, but surely to Africa over time, as demographics shifts to that continent’s advantage.

Technology is a second and major driver. The digital revolution has already changed the global economic landscape in a major way: by allowing the separation of R&D, management, and production, the digital revolution has enabled global value chains to emerge since the 1980s.

And of course, the internet has unleashed e-commerce, a disruptor that is only in its infancy. E-commerce today only constitutes about 20 percent of all retail sales in China, less than 10 percent in the US, and even less in Europe.

Aside from the global supply chains in production, international e-commerce to consumers has hardly started, shackled down as it is by national regulations, cumbersome border procedures and inefficient postal delivery.

The use of the possibilities of information technology is only at the beginning: Autonomous trucks may arrive on the roads as early as the 2020s, radically changing the use of trucks versus trains. Drones or autonomous carts could soon bridge the last mile. And robots rather than humans could staff the warehouses along the supply chain. The Ueberization of shipping and trucking that is bound to happen could disrupt today’s transport and shipping companies.

Big data is becoming a tool for predictive analysis, which can realize efficiency gains in supply chains and performance monitoring. It will impact pricing strategies, optimized routing and scheduling, customer profiling, privacy and security protection (4).

By 2025, 3D printers will be able to print complex products from a variety of different substrates—and anywhere in the world. Where would manufacturing be done, if 3-D printing can produce a wealth of products close to the market? The demand for transport/physical connectivity will drastically decrease if 3D printing were to be used on a large scale at locations closer to the markets than production today.

The third driver of future global logistics is policy: Policies are driven by the problems of our time, and perhaps the biggest policy challenge today is Global Warming. There is no doubt in my mind that this will drive the demand for green logistics—by taxing polluting logistics or by restricting their emissions through emission capping and trading. This will induce changes in mode of transport to greener solutions and/or intermodal solutions. Road transport will continue to play a major role, esp. in the first and last mile but vehicles will have to become cleaner—more so ships and planes.

As an aside, in the long-term, global warming could bring new trade routes along the northern route. Impact would be a shifts in trade flows between Asia and Europe, diversion of trade within Europe, heavy shipping traffic in the Arctic and a substantial drop in Suez traffic*.

A second policy challenge is growing economic nationalism and protectionism. There is growing concerns about the effects of globalization on jobs and income distribution in some countries, and domestic interests will continue to clash and compete with the forces of global integration. Therefore, trade policies may derail the benefits of globalization, and with it the future of global trade and logistics.

Finally, with the IT revolutions only in its infancy and about to revolutionize many industries—not just logistics—politicians are becoming aware of the potential impact on people’s jobs and livelihood. In fact, some estimates suggest that some 50-70 percent of all current jobs are at risk for automation. The logistics industry is in many ways at the forefront: truck drivers, warehouse attendants, sailors, and booking clerks are among the professions at risk of automation.

We are only starting to come to grips with such a dramatic change for people’s future, and how politics and policies will react to this trend will determine the very nature of society we will live in.

So how does this all add up? Well, I can only imagine. I can imagine that some 10-15 years from now, my hologram self meets in New York with a producer, and upon conclusion of the contract, I order my virtual assistant to book space on a shared ship about to leave from China, powered by solar cells. The ship will take the northern route, unloads on a fully automated dock in Rotterdam, onto autonomous trucks, which in turn are unloaded by robots on delivery drones that deliver on the doorstep of my clients in Amsterdam. In other words, I can imagine a future of logistics that is dramatically different from the logistics of today

As William Gibson, the famous science fiction writer wrote: “the future is already here, it is just unevenly distributed.”

Xie xie dajia.