A new World Bank Country Economic Memorandum (CEM), titled Poland: Saving for Growth and Prosperous Aging, is attempting to address this issue of saving by looking at whether the Polish economy is saving enough to finance its growth and whether citizens in the country are saving enough to ensure they are financially secure into old age.

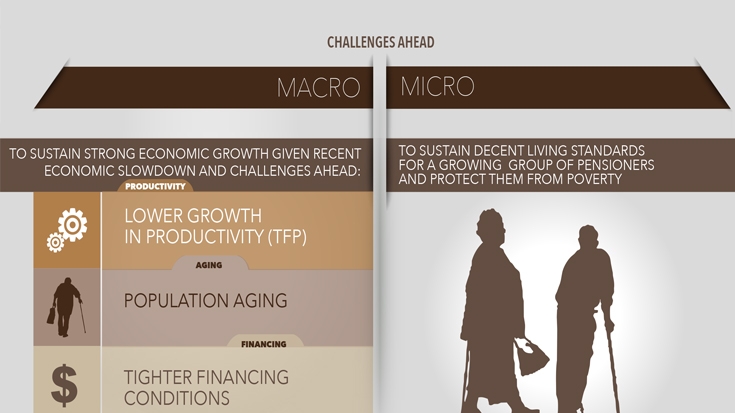

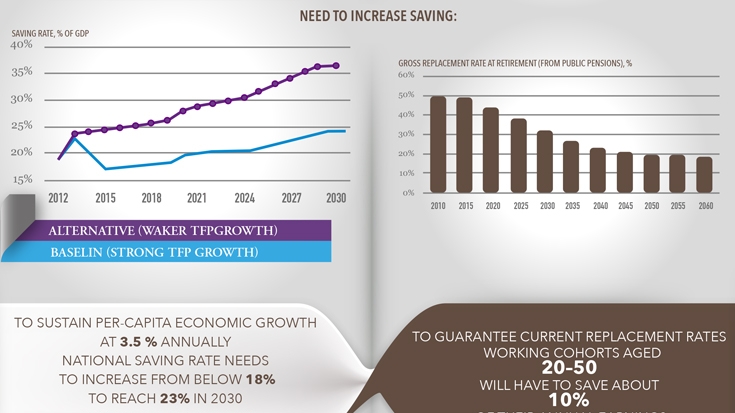

As the country continues to age, a greater share of its population is heading into retirement, while fewer and fewer workers are entering the workforce to replace them. This trend not only affects the future supply of labor in the country, it also impacts social systems such as pensions. This is particularly worrisome in Poland, where retirees draw 80 percent of their income from their pensions – compared to just 60 percent in other, similar economies. As the population ages, household savings - which amounted to just 3% of Gross Domestic Product (GDP) in 2012 - are expected to reduce even further. As pensions transform in response to reforms introduced in 1999, household savings will need to increase in order to bridge income gaps not filled by public pensions in the future and avoid old age poverty.

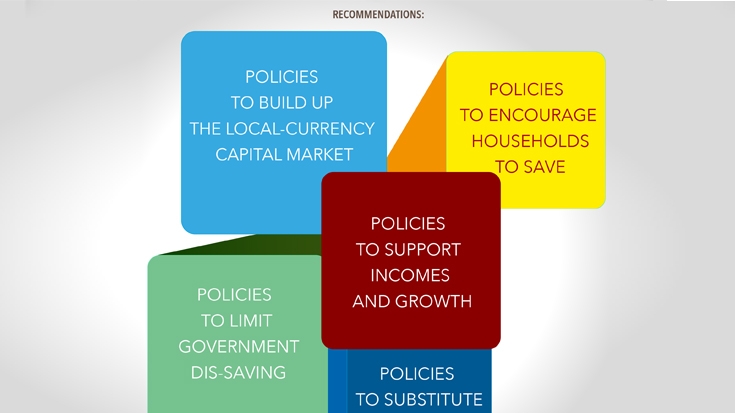

According to this CEM, individuals are not the only group that needs to alter its saving habits. At the macroeconomic level, both the state and the corporate sector will need to make adjustments to their savings to help the country meet the economic challenges of the next phase of Poland’s development. Today, government policies do not provide incentives to private savings, while corporate savings often occur in the absence of reinvestments into new technologies, training, and innovation. Policies and regulations may need to be reformed at the state level in order to better incentivize savings at the individual level, while the corporate sector is tasked with a difficult balancing act – the need to sustain high saving and translate these into productive investments.

In addition to identifying key areas of engagement, the CEM also provides a series of actions and recommendations that can help mitigate the negative impacts of aging. For individuals, the report argues that increased levels of education and a higher retirement age can help bolster income and savings in the future. By supporting income and growth – through the introduction of measures that can increase employment and remove disincentives to work – the government can play a key role in encouraging households to save more for their futures.

Finally, further development of Poland’s financial sector beyond the current credit penetration of 54% of GDP would benefit saving and growth. The promotion of savings and their efficient use is closely linked to the issue of developing a local currency capital market. Local currency capital markets can provide savers with long-term investment instruments. In order to promote capital market development the report advise regulatory changes to improve functioning of the second pillar (OFE) and third pillar and facilitate bond issuance such as covered bonds or corporate bonds.

A complex understanding of both the causes and solutions of Poland’s growth dilemmas, like the one offered in the latest Country Economic Memorandum, can be an invaluable tool in helping policymakers design appropriate measures today that can have a lasting impact tomorrow. But time is of the essence. The cost of delaying this response is high. If Poland takes immediate action to moderate the impacts of the challenges being posed by aging – primarily by handling projected growth in health spending – GDP in 2050 could be 1.5% higher than in the baseline developed in the report.

{kind=link}