November 17, 2021 — The size of the informal economy as a share of GDP in Africa is the largest in the world and with most jobs expected to be created in the informal economy, they will continue to be the lifeblood of economies. Informality in these economies is often characterized by low human capital, low productivity, limited access to basic services, limited financial inclusion, low earnings, and irregular, unpredictable income.

Despite these vulnerabilities, informal economy workers are not typically covered by social protection programs. Coverage of existing social insurance programs is also limited to the small formal economy in the region.

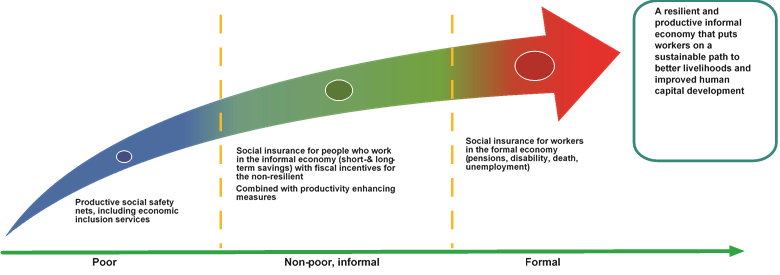

In light of existing vulnerabilities, high and persistent rates of informality, and limited ways to assess needs of informal sector as evidenced in the pandemic, governments in Africa and beyond are looking to revisit their social protection programs. Expanding coverage to workers in the informal economy is now at the forefront of social protection priorities in these economies.

The report begins with a synthesis of social protection responses to COVID-19 from Africa underscoring the gaps in coverage arising because of the “missed middle.” Policy makers and social protection practitioners need to understand the characteristics of the missed middle — composed largely of workers in the large and diverse informal economy — to design appropriate risk mitigation instruments.

The key questions policymakers and practitioners face when launching or scaling social protection schemes for workers in the informal economy are addressed in this report. A suite of social protection instruments including safety nets, economic inclusion programs, productivity enhancing measures as well as social insurance implemented with support of coordinated policies would ensure a continuum of social protection to the informal economy across the income spectrum.