WASHINGTON, October 9, 2013 – Economic growth in South Asia will be modest this year and in 2014. At such a pace, the goal of ending extreme poverty by 2030 will not be attained. Governments must work harder on reforms to raise growth in a region where most of the world's poor live, the World Bank said today.

According to the South Asia Economic Focus report, South Asia was the second-fastest growing region in the world in the aftermath of the global crisis. However, its recent performance has been less stellar, and it has been sustained by potentially volatile portfolio inflows. More stable Foreign Direct Investment (FDI) in the region is low, half that of other regions relative to GDP; inflation is twice that of other regions and fiscal deficits and debt-to-GDP ratios are high.

![]()

“South Asia must return to the growth rates achieved before the global financial crisis of at least eight percent a year so that it can significantly reduce poverty,” said Philippe Le Houérou, World Bank Vice President for the South Asia Region. “South Asia is critical to the World Bank Group goals of ending extreme poverty and boosting shared prosperity by 2030 and we will work with governments in the region to overcome barriers to growth and provide greater opportunity for all.”

Recent global capital rebalancing, driven by fears of unwinding of easy monetary policy in the US, has highlighted structural weakness and vulnerability in South Asia. This provides a wake-up call for policymakers not to lose focus on tackling key economic and investment constraints.

Regional GDP is projected to grow by 4.4 percent in the 2013 calendar year, 5.7 percent in 2014, and 6.2 percent in 2015, driven by an improvement in export demand, measures to speed up the implementation of large infrastructure projects in India, stronger private investment activity, and a good monsoon.

India, the region’s main economy—around 80 percent of South Asian GDP— is projected to grow by 4.7 percent at factor cost in fiscal year (FY) 2013/14, a slight decline from an estimated five percent real GDP growth in FY 2012/13. Although partly reversed, India’s rupee depreciation of around 20 percent between May and August 2013 reflected changing market sentiment toward the region and the increasing vulnerability to external shocks.

Other countries across South Asia are either growing slowly or slowing down. Overall, South Asia regional growth is expected to moderate in 2013 compared to prior projections. Regional growth has deteriorated in the second and third quarters of 2013, mainly due to supply-side constraints and weak domestic demand.

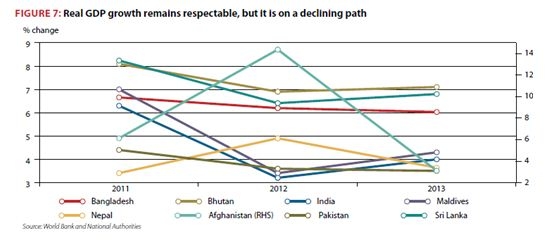

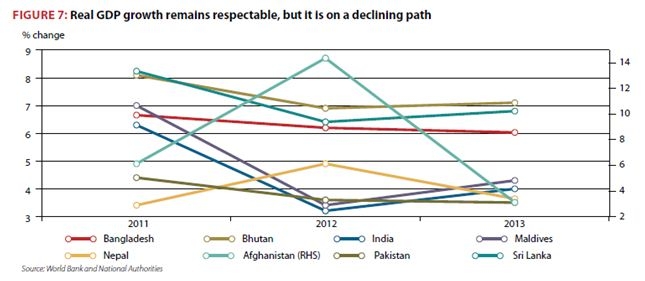

- Afghanistan sticks out in terms of the size of its slowdown, expecting a 2013 growth rate of just 3.1 percent down from 14.4 percent in an exceptional 2012, mainly driven by increased uncertainty stemming from political and security transition.

- Bangladesh’s projected growth for 2013 at 6 percent notes a 0.2 percentage point decrease vis-à-vis 2012, reflecting political uncertainties, supply side constraints and lower investment.

- Bhutan’s real GDP growth is set to fall to 6.9 percent in 2012/13 down from 8.1 percent.

- Nepal’s real GDP growth is set to fall to 3.6 percent in 2013 from 4.9 percent in 2012.

- Pakistan where a marginal 0.1 percentage point decrease to 3.5 percent for 2013 is estimated.

- Maldives and Sri Lanka, on the other hand, expect a slight increase in their growth rates. Maldives real GDP growth is set to increase from 3.4 percent in 2012 to an estimated 4.3 percent in 2013 and Sri Lanka is projected to increase from 6.4 percent in 2012 to 6.8 percent forecast in 2013.

The report, a twice-yearly look at South Asia’s economic prospects, said that despite recent volatility in international capital flows, fundamentals determining long-run growth and stability in South Asia have not changed significantly over the last 12 months. Like other developing regions, South Asia is facing greater turbulence as markets reassess sources of global growth and risks.

“Exuberance has given way to deep pessimism, particularly in the case of India, while the underlying potential remains somewhere in-between,” said Martin Rama, Chief Economist for the South Asia Region at the World Bank. “However, short-term capital market turbulence is manageable and the return to sustainable growth in the developed world is a positive development for South Asia,” he added.

India’s slowdown has significant spillover effects to the rest of South Asia, even more so after the financial crisis. Overall, while South Asia countries vary in terms of political, economic and financing challenges, accelerating the long term reform momentum remains the best policy for coping with turbulent global capital flows—not dramatic shifts in short term fiscal or monetary policy.

Two highly complementary policy areas are central building blocks of much needed higher and sustainable growth.

“First, continuing with a gradual tightening of fiscal and monetary policy, macroeconomic stability and higher tax revenue will create fiscal space and reduce volatility. In this context, letting exchange rates adjust will allow depreciation to enhance the region’s competitiveness and stimulate exports," said Rama. “Second, removing supply side constraints, both regulatory and physical, will pave the way for increasing investment and growth,” he added.

Both regulatory efforts to ease doing business in the region and attract investment, and providing the necessary infrastructure to avoid structural bottlenecks remain at the center of any policy strategy towards bringing South Asia back to its potential and previous performance.