Recent Economic Developments

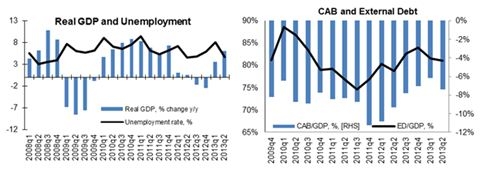

Moldova’s economy recovered from the recession of 2012. In the second quarter of 2013 growth accelerated to 6.1 percent y/y, bringing the GDP growth in the first half of the year to 4.9 percent. Manufacturing grew by 9.4 percent, while investments in road infrastructure and construction stimulated an expansion of output in quarrying by 18.8 percent in the first half of 2013. Private consumption was the main growth driver on the expenditure side (+5.8 percent), fueled by remittances and wage growth. Despite relatively good increase (+4.5 percent), fixed investments still underperformed as a driving force of economic growth.

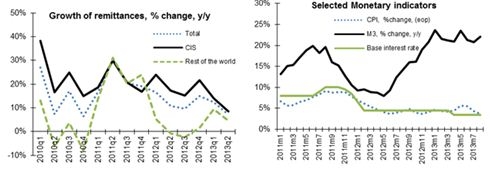

The current account (CA) deficit remains in single digits, while the National Bank of Moldova (NBM) managed to boost foreign exchange reserves. The CA deficit was 8.6 percent in 2013H1. While trade deficit remained large, export growth (7.5 percent) outpaced import growth (6.3 percent) in 2013H1. Growth of remittances (mainly from CIS countries) was strong, increasing by 9.5 percent in 2013H1, almost reaching pre-crisis levels. Foreign Direct Investment (FDI) recovered by 53 percent to 3.3 percent of GDP, but still has not reached pre-crisis levels. In mid-2013, total external debt stood at 81 percent of GDP. Overall, the external position was strong and enabled accumulation of foreign exchange reserves, now covering over 4.5 months of import and 138 percent of short-term external debt.

Monetary policy has been consistent with inflationary target of 5+/-1.5 percent. By August 2013, consumer inflation decelerated close to lower bound of the target range, to 3.7 percent y/y, due to good 2013 harvest and no adjustments in utilities tariffs. In response to disinflationary pressures, the NBM has loosened monetary policy. Base interest rate is at historically lowest levels since April (3.5 percent). The National Bank allowed moderate depreciation of local currency. Money supply M3 accelerated to 22.1 percent y/y, while credit to private sector grew by 14.1 percent y/y in August 2013.

Driven by higher economic growth, budget revenues remained strong. Revenues grew 8.6 percent y/y over the first 8 months of 2013. Meanwhile, government spending lagged behind the plan to date, so that the deficit narrowed in Jan-Aug 2013 to 1.6 percent of estimated GDP, compared to 3.1 percent of GDP same period last year.

Medium Term Outlook

We expect the GDP growth to accelerate to 5.5 percent in 2013, before decelerating to 3.5 percent in 2014. In the medium-term, we project the growth to settle around 4.5 percent. Recovery in agricultural production, after the severe drought and contraction of output in 2012, will be the key factor behind the expected higher outturns in the second half of 2013. In addition, strong growth of remittances, in particularly driven by the large-scale infrastructure investments in Russia, is expected to support continued growth of consumption and investment. In 2014, both factors mentioned above will weaken, reducing the expected growth trajectory. Meanwhile, external demand from largest trade partners is likely to be muted: economic growth in Russian Federation is slowing down, while the recovery in the EU is still going to be weak. From 2015 onwards we expect the external demand to pick up, fuelling both Moldovan exports and remittances to Moldova.

As a small open economy, Moldova is vulnerable to global economic conditions, underscoring the importance of prudent macroeconomic management. In recent years authorities made a substantial progress in macro management: inflation is under control, fiscal deficits are below 3 percent of GDP and public debt is low. However, the challenges posed by of the electoral cycle and the still fragile external environment require strong institutions to be in place. According to our projections, CA deficit will widen in the coming years. Implementation of recurrent expenditure increases adopted earlier this year and higher capital spending will increase the fiscal deficit to 2.5 percent of GDP in 2013 and to 3 percent in 2014. While aggregate banking performance indicators show positive trends, there are vulnerabilities related to corporate governance and transparency of ownership of the banks, as well as effective enforcement powers of the regulator.

To enhance growth prospects, Moldova needs to accelerate pro-investment and pro-export reforms. The authorities are pursuing an ambitious program of structural reforms for growth embedded in the National Development Strategy “Moldova 2020,” which the World Bank is supporting through the recently approved Country Partnership Strategy for 2014-17. While challenges are numerous, the Government could concentrate reforms efforts in three areas over the next year. First, improving predictability of the business enabling environment, creating even conditions for competition, and reducing regulatory compliance costs. Second, strengthening financial sector stability, promoting transparency and improving access to finance. Third, improving the efficiency and equity of public investment, investment subsidies in agriculture and social assistance.