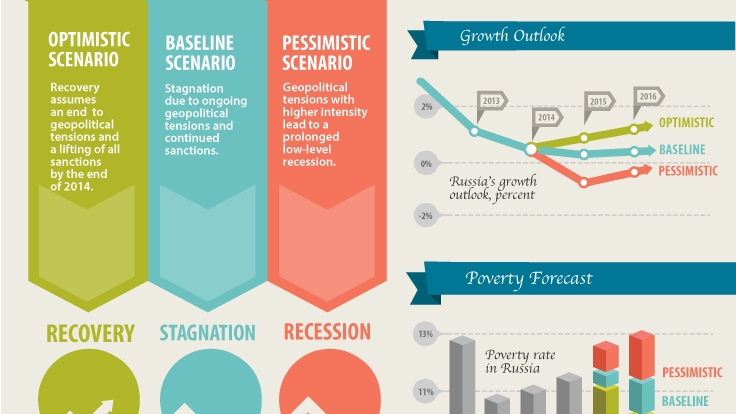

Russia’s economy is stagnating. Increasing uncertainty has impacted investor and consumer decisions. There are substantial risks to Russia’s medium-term outlook. Economic recovery will need a predictable policy environment and a new model of diversified development. Prospects for further poverty reduction and shared prosperity are limited.

Structural impediments slowed economic expansion to near stagnation even before the impact of increased policy uncertainty amid increased geopolitical tensions took hold.

GDP growth was just 0.8 percent in the first half of 2014 compared to 0.9 percent in the first half of 2013.

The reasons for Russia’s slowdown remain, on balance, of a structural nature, with the economy operating at close to its potential output level.

Although Russia’s growth was not dissimilar to that of the Euro Zone, it dipped under that of other country comparator groups, such as emerging and high-income economies.

Due to Russia’s integration into the world economy with exports of resource-intensive products to high-income countries, their growth paths remain closely entwined. Current geopolitical tensions are adversely impacting these trade relationships.

Outlook

Over the medium term, growth will continue to be determined by slow progress in structural reforms and policy uncertainty emanating from geopolitical tensions.

The main challenges for Russia’s outlook are twofold: consumption growth is likely to weaken even further than previously projected and recovery in investment demand will be slower than previously expected.

The effects of weak growth for a second consecutive year, an increase in household debt burden, and continued high inflation expectations, are likely to depress consumer demand further, slowing this main engine of growth in Russia. These effects are expected to persist for the next two years.

With no major structural reforms planned, and microeconomic fundamentals unchanged, investment will remain subdued and there will be only a limited positive effect from import substitution.

Similarly, the multiplier effect from the planned increase in public and quasi-public investment expenditures is likely to be modest.

Towards Diversified Development

Russia’s portfolio is heavy in tangible assets such as oil and gas, and hard infrastructure such as schools, but it is light in intangible assets such as institutions for managing volatile resource earnings, providing high-quality social services, and even-handedly regulating enterprises.

Russia’s institutional weaknesses are now the main stumbling block on the road to greater economic efficiency and higher growth rates.

Developing a more balanced portfolio of national assets, namely natural resources, capital and economic institutions, can help Russia overcome structural constraints to growth.

Structural reforms would need to focus on improving economic institutions to ensure that public finances are stable and volatility is well-managed; that there are improvements in education and infrastructure to make workers more productive; and that there are strong competition regimes to encourage private enterprise and entrepreneurship.

Stabilization, transparent rules, better quality of public investment, and competition should be the reform priorities for the next decade.

This report series is produced twice a year by World Bank economists of the Europe and Central Asia Region Poverty Reduction and Economic Management Department.

You have clicked on a link to a page that is not part of the beta version of the new worldbank.org. Before you leave, we’d love to get your feedback on your experience while you were here. Will you take two minutes to complete a brief survey that will help us to improve our website?

Feedback Survey

Thank you for agreeing to provide feedback on the new version of worldbank.org; your response will help us to improve our website.

Thank you for participating in this survey! Your feedback is very helpful to us as we work to improve the site functionality on worldbank.org.