STORY HIGHLIGHTS

- The first edition of the Eswatini Economic Update shows an economy with positive prospects but trapped in low growth by domestic and external headwinds, hindering poverty reduction. Growth rebounded to 7.9% in 2021 but slowed in 2022.

- The report argues that though the fiscal situation is improving, Eswatini needs to continue its fiscal consolidation plan to sustain macroeconomic stability, reduce public debt, eliminate expenditure arrears, and increase its external reserves.

- It finds that though there are not many commercial State-Owned Enterprises (SOEs), they retain a considerable presence. SOEs drain fiscal resources and, as regulators in the sector in which they operate, create an uneven playing field for private sector firms.

Mbabane, August 7, 2023 – This first edition of the Kingdom of Eswatini Economic Update focuses on State-Owned Enterprises (SOEs) and analyzes the role they can play in efforts to improve the country’s economic performance. It assesses both their contribution to the economy and their limitations to suggest directions for reform.

The Update projects economic growth to slow in 2023 to 3.0% from 3.6% in 2022. The public sector is likely to drive growth, buoyed by an almost doubling of Southern African Customs Union (SACU) receipts. But, without reform of the business environment, the private sector is likely to remain subdued. Inflationary pressures have increased, partly due to the war in Ukraine. Sustaining high growth rates will require Eswatini to shift from state-led to private sector-export-led growth.

The fiscal situation is improving but more reforms are needed. Fiscal consolidation has helped the deficit drop from 8.6% of GDP in 2016 to 4.6% in 2021. Initial efforts were promising, but by 2022 implementation was uneven, and the overall fiscal deficit rose to 5.3% in 2022. A decline in 2023 owes more to high SACU revenues than to consolidation. Even when SACU revenues increase the authorities should prioritize long-term aspirations over short-term needs.

Eswatini needs to continue with its fiscal consolidation plan to sustain macroeconomic stability, reduce public debt, eliminate expenditure arrears, and increase external reserves. Public finances remain extremely exposed to the volatility of SACU revenues, hence any increase in receipts should be carefully managed and used to smooth future shocks in revenue. The SACU Revenue Stabilisation Fund is a step in the right direction.

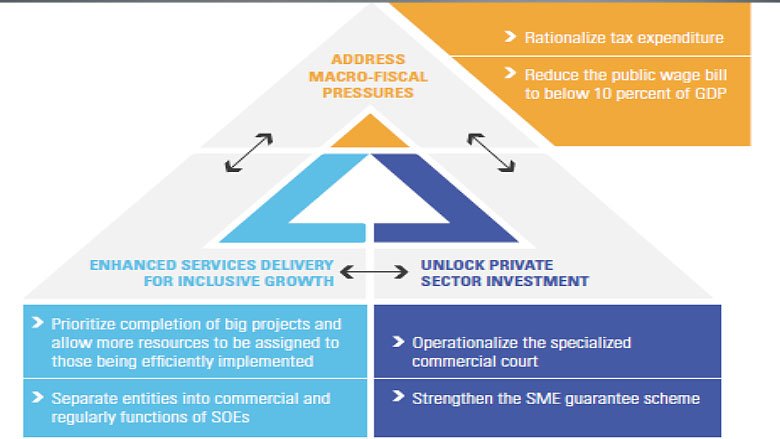

The report proposes policy options to improve Eswatini’s growth prospects based on three pillars:

1. Address macro-fiscal pressures through prudent macroeconomic management,

2. Unlock private sector investment through structural and governance reforms, and

3. Enhance service delivery for inclusive growth through an improvement in public spending and SOEs reforms.

Although there are not many commercial SOEs, they retain significant direct and indirect effects on the economy. The government recognizes SOE reform as an important priority if the country is to accelerate growth and ensure fiscal sustainability. This is contained in various documents such as the National Development Framework 2019–22, the Fiscal Adjustment Plan, and the government-commissioned study on improving the performance of SOEs by the Eswatini Economic Policy Analysis and Research Centre.

Eswatini’s seven commercial SOEs have been marginally profitable over the past five years, but most cannot pay dividends to the state, despite a dividend policy. The commercial SOE sector remains a net drain on the national budget: the cumulative outflow to SOEs (grants/direct subsidies and equity) over the past five years was $158 million, whereas the inflow (dividends and income taxes) was only $47 million. Their debt-to-equity ratio almost doubled between 2020 and 2022. SOEs constrain private sector investment in various ways, including through direct competition, higher operating costs, and presenting barriers to the entry of efficient private sector providers.

Reforming SOEs is key to the country’s success. The report suggests three directions for policy reforms to take:

Rethink the state’s role in the economy through enacting an SOE ownership policy that explicitly includes a clear rationale for maintaining state shareholding in SOEs.

Strengthen the legal framework to include a clearer definition of SOEs, separate from regulatory agencies. This involves amongst others, clarifying the definition of SOEs and reclassifying public enterprises.

Strengthen SOE governance and oversight. This will involve interventions such as improving the monitoring of SOEs including of equity stakes held by the state and enhancing the transparency of SOE information.