For the latest East Asia and Pacific Economic Update (December 2012), please go to https://www.worldbank.org/en/news/2012/12/19/east-asia-and-pacific-economic-update-december-2012-remaining-resilient.

Key findings:

- Growth in developing East Asia and Pacific has remained strong, though it has been slowing from its post-crisis peaks.

- In 2011, developing East Asia grew by 8.2 percent, a sharp decline from the nearly 10 percent growth rate recorded in 2010.

- This was largely due to lower growth in manufacturing exports as well as supply disruptions in the wake of the Japan earthquake and Tsunami and severe flooding in Thailand, Lao, PDR, and Cambodia.

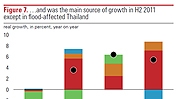

- Domestic demand and investment were generally strong and aided by loosening of monetary policy in some countries.

- For 2012, we expect that East Asia will remain the strongest performing region, even though annual growth will further moderate as a result of a continued weak external environment.

- Developing East Asia is projected to grow by 7.6 percent in 2012, with slower expansion in China pulling down much of the regional aggregate.

- Poverty continues to fall, with the number of people living on less than US$2 a day expected to decrease in 2012 by 24 million.

- Overall the number of people living in poverty has been cut in half in the last decade in East Asia and Pacific

- Risks emanating from Europe have the potential to affect the region through trade and financial linkages.

- The EU, along with the US and Japan, accounts for more than 40 percent of the region’s exports. European banks provide one- third of trade and project finance in Asia.

- Most East Asian economies are well positioned to weather renewed volatility.

- Domestic demand has proved resilient to shocks; most countries run current account surpluses and hold high levels of international reserves; and banking systems are generally well-capitalized.

- As external demand is likely to remain weak, countries in developing East Asia and Pacific need to rely less on exports and more on domestic demand to maintain high growth.

- China’s growth pattern is also changing as it moves up the income ladder, and is likely to rely more on consumption and less on investment and exports, and more on services and less on industry – offering opportunities and challenges.

- Already, many countries are moving in this direction, but there is further scope for rebalancing.

- Some countries will need to stimulate household consumption. In others, enhanced investment, particularly in infrastructure, offers the potential to sustain growth provided this does not exacerbate domestic demand pressures.

- With a changing financial sector in the aftermath of the financial crisis, new ways to finance higher levels of infrastructure investment need to be developed.

- In the medium-term, investment will enhance productivity and drive growth through higher value-added activities and innovation. Although large gains have been made in labor productivity across the region since the Asian financial crisis of 1997-98, there is still large room for further gains.