The gender roles in sending, receiving and utilizing remittances is oftentimes overlooked given the general focus on the household. However, the World Bank experience with Project Greenback[1] in the Western Balkans[2] revealed some clear differences between men and women in terms of behaviors and attitudes related to remittances. Accounting for these differences is important for public authorities and remittances industry in their efforts to maximize the development impact of remittances in the region as a vital source of income and a gateway to broader financial inclusion.

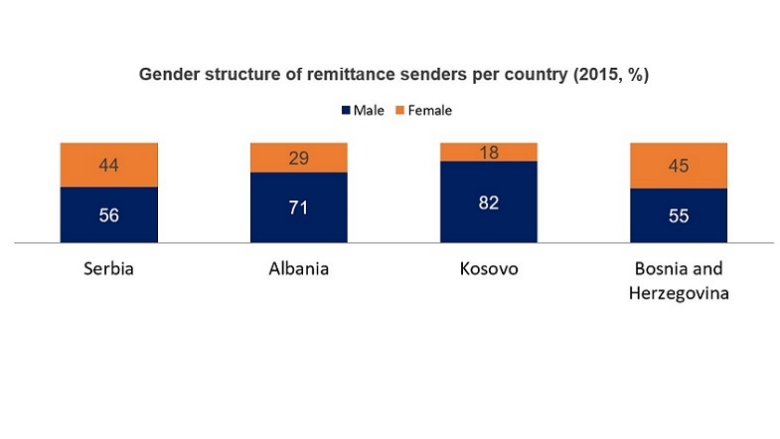

Women’s role as remittance senders is increasing over time, prompting greater focus on women and confirming the need for tailored support to this target group. For the Western Balkans, the man in migration has been traditionally deemed the breadwinner of the household, while the woman has typically stayed in the home country to raise the children and cater to the family needs. This was also true for remittances, as men represented the bulk of remittance senders. However, there is a noticeable shift in the migration dynamics over time. While at first many men would migrate alone particularly towards Western Europe, over time families have reunited once documentation and financial barriers have been overcome. Furthermore, women have also started to migrate more on various capacities. The gender-equalizing trend is most notable in some corridors, such as Greece – Albania or Italy – Albania, where women represented only 20 percent of the migrant stock in early and mid-90s, but their share doubled in the early 2000s[1]. This increase in migrant stock has also affected the remittance volumes sent back to Albania.

[1] The insights presented here originate from focus group discussions with at close to 400 remittance senders and receivers from the Western Balkans as well as data from the Baseline Survey on Remittance Beneficiaries’ Financial Behaviors in East Europe and Central Asia by the World Bank (2017).

[2] Project Greenback in the Western Balkans is being implemented in Albania, Bosnia & Herzegovina and Kosovo as part of the SECO-funded Remittances and Payments Program since 2015.

[1] According to the Baseline Survey, for both Greece and Italy, the 2001 census highlighted the fact that females accounted for around 20 percent of total Albanian migrants in the early and mid-1990s and by 2000-2001 the share had increased to approximately 40 percent of total Albanian migrants.