It is an honor and privilege to join you for the US SEC’s 26th Annual International Institute for Securities Market Development. My profound gratitude to the US SEC for inviting me to give the keynote address at this year’s Institute. The quality of the program over the years has ensured that it has remained a well-sought after program for capital market regulators around the world. I understand that there are over 150 attendees from several countries, this year. It is also evidence of the US SEC’s commitment to promoting robust capital markets around the world.

Let me also use this opportunity to acknowledge the US SEC for the support that they gave my colleagues and I during the five years, I was the Director General of the Securities and Exchange Commission, Nigeria. This support was invaluable to our numerous achievements and enabled us to reinforce integrity as the foundation of the Nigerian capital markets. Permit me also to specially acknowledge Mr. Scott Birdwell who was instrumental to nurturing this first class partnership.

I am delighted to be in your midst given the importance of capital market regulation. It is a unique occasion for me to reminisce about the fulfilling opportunities that my role as a regulator gave me. I have a number of my colleagues here with me because of our desire at the World Bank, to foster new partnerships given our work on the development of capital markets around the world.

In addition to the fantastic learning opportunity it offers, the Institute will enable you develop life-long friendships that will be useful throughout your career as you create the framework, enforce the rules, and in so doing, build world class capital markets that are not only trustworthy but also efficient, sound and powerful engines for economic and social development.

Let me first define what I believe a world class capital market is. A world class capital market is one that engenders investor confidence, has breadth and depth in terms of product offerings, is characterized by the highest levels of integrity, has a sound regulatory framework, a transparent disclosure and accountability regime, and is a fair, robust, and efficient market place. World class capital markets facilitate economic diversification, enable economic agents to pool, price and exchange risks, encourage savings and create wealth.

World class capital markets fund business expansion and opportunity and provide governments with long term funds for financing infrastructure and other important projects that transform economies. They enable socio-economic development because they foster a meritocracy, good corporate governance, innovation and entrepreneurship, which in turn, create much needed job opportunities. In addition, they broaden access to economic prosperity and provide efficient channels for democratizing business success. Indeed, in a world that has become increasingly insecure, wealth creation and distribution facilitate inclusive societies which in turn deter the recruitment of young people for terrorism and other atrocious crimes. Your role is no doubt key to tackling the global challenges the world currently faces.

In my remarks today, I will first present relevant highlights of the global economic environment, then review key lessons from my previous experience as a capital market regulator and finally describe some of our work at the World Bank that pertain to the development of capital markets.

With global growth expected to rise by only 3.4% in 2016, the world economy remains fragile despite aggressive monetary stimulus since the 2008 financial crisis. While the US is doing relatively well, there is insufficient support from other economies. De-leveraging, and accommodative monetary policies have kept interest rates low, with Europe and Japan currently experiencing negative interest rates. Growth in emerging market and developing economies rose by only 4 percent in 2015, the lowest since the financial crisis. The slowdown and rebalancing of the Chinese economy, lower commodity prices, and financial strains on some large emerging market economies will continue to weigh on growth prospects this year and in 2017. Emerging market economies that were therefore expected to lift global recovery have recently been experiencing serious challenges leading to increasing risk premia, capital outflows, and currency depreciation. Some might even question the soundness of opening capital markets to foreign investors in such an environment. I, however, do not share this view. Rather, I am a strong believer in the benefits of developing local capital markets that are open to foreign investors and partners.

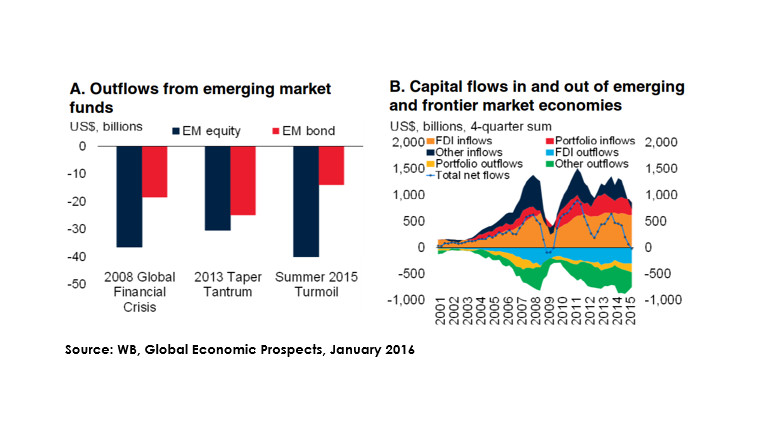

Capital flows to emerging and developing economies have already decelerated to their weakest levels since the financial crisis. Foreign direct investment has shown greater resilience, but short-term debt and portfolio inflows have been impacted significantly. Weakening capital flows have exacerbated currency and equity market pressures in many countries, particularly among commodity exporters. Borrowing costs have also risen in line with heightened risk-aversion, and corporate bond issuance has slowed significantly. From this perspective, deepening local capital markets represents a renewed priority.

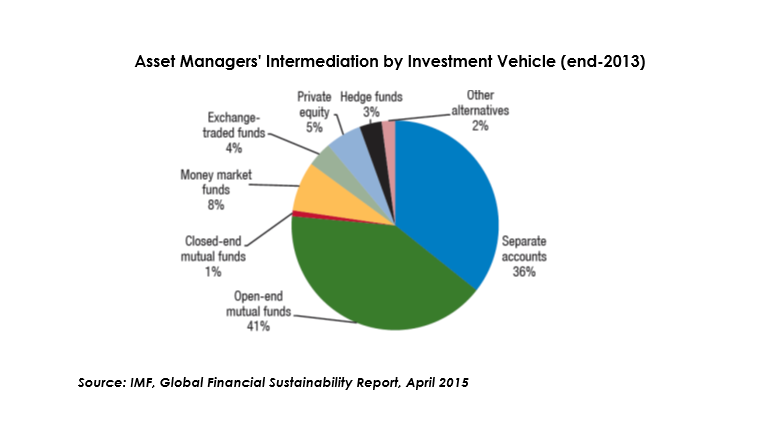

The outflows from emerging and developing markets are making headlines right now – highlighting the vulnerabilities that come with opening markets to international investors. The volatility of portfolio flows and the resulting systemic risks should be addressed through smart regulation. At the same time, we cannot overlook the fact that the stock of assets under global management has increased tremendously over the years. According to the April 2015 IMF Global Financial Stability Report, the asset management industry globally intermediates $76 trillion, equivalent to the aggregate GDP of the whole world. According to TheCityUK estimates, assets under management rises to US$163 trillion, if you add pension, insurance, and private wealth management funds. The majority of these funds are invested in equities, bonds, and other securities traded in international and domestic financial markets. This highlights the tremendous potential of capital markets as a tool for attracting financing for economic and social development.

While, the bulk of these funds are invested in developed markets, the weight of emerging and developing economies has increased steadily over the past 10 years. For example, the World Bank’s latest Global Financial Development Report on long-term finance found that assets under management of mutual funds domiciled in developing countries more than doubled between 2006 and 2013, yet they still represent a small fraction of world-wide assets. Another important trend has been the growth of international mutual fund investments in emerging markets as investors have sought higher-yielding assets during this period of low-interest rates. 2013 data on US and UK mutual funds investing internationally showed that 50 percent of investments was in Europe, about one-third in Asia, almost one-fifth in Latin America, and some interest in Africa, albeit still small.

Given the weak global economic environment, I hope that you agree with me that world class capital markets will be best placed to attract and retain the trillions of assets that are looking for safe places to invest. This was the position we took at the Securities & Exchange Commission (SEC) Nigeria, during my five year tenure. In the next section, I will like to outline the lessons, I learnt from the efforts that my colleagues and I made to build a robust capital market.

When I joined the SEC Nigeria, in 2010, Nigeria was still smarting from the brutal correction it suffered following the global financial crisis. There was general malaise, investor apathy following an unprecedented 70% stock market decline from March 2008 to February 2009. The market had been characterized by various forms of market abuses, on the heels of a market that grew rapidly but was not supported by adequate regulation and oversight. While others saw gloom, my colleagues and I saw an opportunity for Nigeria to build a world class capital market using the lessons we and other countries had learned from the global financial crisis.

In addition to fulfilling our mandate of regulation and market development, we felt that a robust capital market had a key role to play in rebuilding the Nigerian economy. The goal of our reform agenda was therefore to build a world class market that would enable Nigeria diversify its economy, finance its huge infrastructure needs and enhance its business climate.

We started by restoring integrity, the backbone of a robust capital market which in turn fostered trust and investor confidence. This was through actions on several fronts. First, our annual inspection of the Nigerian Stock Exchange revealed governance issues that had eroded investor confidence and undermined market integrity. Since an exchange is a visible symbol of any securities market, the market welcomed the decisive steps we took to strengthen the NSE including replacing its leadership. Since then the NSE has taken important steps to reposition itself as an important gateway into Africa.

Second, we adopted a posture of zero tolerance for wrongdoing and strengthened our enforcement machinery through partnerships with the Office of the Attorney General of the Federation and the Nigerian Police Force. We specifically had a resident Nigerian Police Desk to deal with matters that involved criminal violation of the securities law. We instituted legal proceedings against 260 individuals and entities for various forms of market infractions seeking the disgorgement of any illegally gained profit. We signaled that there were personal costs to market infractions and that the cost of market abuse would be higher than any benefits that could accrue. People decided that a new ‘Sheriff’ had come into town as they had seen concrete evidence that we would do whatever it takes to punish wrongdoing.

We revamped our investor protection and dispute resolution mechanisms by strengthening SEC’s quasi-judicial Administrative Proceedings Committee (APC), developing a robust complaint management framework, setting up the National Investor Protection Fund and strengthening Anti-Money Laundering and Counter Terrorism Financing (AML/CFT) framework.

Robust markets are based on trust, and trust is built on consistently enforcing the rules and punishing wrong behavior. Scott Birdwell brought to my attention, the study carried out by Professor John C. Coffee of Columbia University’s School of Law, on the relationship between enforcement by securities regulators and the development of financial markets. One of his key findings is that the United States is an outlier amongst its peers with enforcement efforts that not only dwarf those of other nations, both in terms of expenditure on securities regulation, but also in the amount and severity of the penalties it imposes. As a result, according to Professor Coffee, investors in the US capital markets benefit from less information asymmetry and issuers enjoy a lower cost of equity capital.

You will agree with me that rules are meant to shape behavior, set standards and ensure a level playing field for all market participants. They also promote orderly trading, transparency and market efficiency. The impact of the financial crisis on the Nigerian stock market was exacerbated by inadequate rules. For example, excessive risk taking was fueled by the absence of adequate margin trading regulation. We used rulemaking to enable best practice and ensure adherence to the principles of securities regulation as espoused by the International Organization of Securities Commissions (IOSCO). We also enhanced market transparency through implementation of global best practice in corporate governance and financial reporting, issuing a new world class code of corporate governance and supporting the adoption of the International Financial Reporting Standards (IFRS).

You must have world class standards to build world class capital markets. Implementing international best practices is crucial, but contributing to the work of the international standard setters is also important to ensure that the rules are relevant for all countries and address the various challenges faced across the globe. All too often regulators and officials from emerging and developing economies do not participate as much as they should in relevant discussions and decisions. Your leadership as securities regulators in this area is essential. It is for this reason that I, as Chairperson of IOSCO’s Africa Middle East Regional Committee (AMERC) and a Board member of IOSCO ensured greater voice for developing countries.

A world class securities market is one that also has breadth and depth in terms of well-regulated product offerings. The regulatory environment must therefore foster sound innovation. When I joined SEC Nigeria, the Nigerian capital markets had a very narrow set of product offerings. Indeed, the stock market dominated with the banking sector making up at the peak over 60% of the stock market. This made the Nigerian capital markets vulnerable to shocks in the Nigerian banking system. The stock market was not reflective of the richness and diversity of the Nigerian economy. To address this weakness we implemented a number measures. We approved new listing rules to attract more listings including small and medium scale enterprises (SMEs) and businesses in strategic sectors of the economy. We also approved rules on securities lending and market making to boost liquidity.

We revamped the fixed income market, a key asset class for pension funds, and insurance companies. We streamlined the bond issuance process, introduced shelf registration and book building, and reduced issuance costs. Other products introduced include exchange traded funds (ETFs), real estate investment trusts (REITs), and other varieties of collective investment schemes. We broadened Islamic finance product offerings. All these initiatives are helping Nigeria tackle its huge US$ 35 billion annual infrastructure deficit, its 18 million housing deficit and is helping Nigerian state governments fund their investment plans. There are other benefits including enhancing governance since rating agencies and other players need to provide independent assessments of state governments as part of a bond issuance process.

I believe that another element of a robust market is an environment that promotes knowledgeable investors who know their rights and understand the product offerings as well as the benefits and risks of investing. To build strong markets, you must therefore emphasize investor education. At SEC Nigeria, we leveraged innovative platforms like Nigeria’s Nollywood industry, cable television, and social media to expand investor education. We reached out to people directly through our health and wealth days, catch-them-young programs, secondary school quiz competitions, a SEC Integrity Award initiative, programs for market men and women, and academies for shareholders and journalists. What I want you to take away here is that for the benefits of capital markets to be shared by the population, you must invest in education and build public awareness.

As a result of these initiatives, the Nigerian securities market witnessed remarkable progress in all spheres. The historical dual listing of a Nigerian oil and gas exploration company on the NSE and the London Stock Exchange was evidence of the positive impact of our reforms. Similarly, domestic bond issuance by the African Development Bank and the International Finance Corporation, two prestigious Triple-A rated institutions was another evidence of the positive results of our efforts to build a world class market. I knew however that we were not done as the capital market could still play a much greater role in enabling Nigeria actualize its aspirations to become one of the top twenty economies in the world. I believed that a key legacy that will ensure that we continued to progress in a strategic and organized manner had to be a ten year capital market master plan that will be the blue print that will guide the development of the Nigerian capital markets. We worked with the market to produce one that is guiding the development of the Nigerian capital markets from 2015 to 2025. Others, including the European Union, Kenya and Malaysia, have relied on similar initiatives to continue to build robust markets.

The World Bank Group recognizes the importance of capital markets and provides support in a variety of ways. This is because we believe that deep, diversified, efficient, inclusive, and stable financial systems, are key to the achievement of the World Bank Group’s twin goals of ending extreme poverty and boosting shared prosperity. Along with our partners, we are also working towards achieving the ambitious goal of Universal Financial Access for adults by 2020. We are championing the global expansion of financial inclusion, particularly, market/financial access for MSMEs and individual entrepreneurs. We are also promoting the use of new technologies to foster financial inclusion and market development. One example is the Treasury Mobile Direct Project in Kenya, where the Bank is partnering with the government and other stakeholders to develop the distribution of government securities to retail investors at auctions through mobile phones.

The Bank Group is also exercising leadership in key standard setting bodies, such as the Financial Stability Board (FSB), and contributing to country analytical and assessment work essential for increasing financial sector stability. Given its membership and mandate, we are committed to ensuring that the voice of developing countries is heard in international regulatory bodies.

Last but not least, the World Bank Group is delivering tailor-made solutions to complex issues faced by emerging market countries in developing domestic capital markets and accessing international capital markets. We do this through results-based, multi-year engagements with government authorities and stakeholders at all points along the road to reform. We assist governments in developing and implementing critical reforms as well as enhancing the safety, efficiency and reliability of national payment systems as well as systems for clearing and settlement of derivatives and other capital market infrastructure. We provide technical assistance on policy, legal and regulatory issues. The Bank draws on its global reach, depth of technical competency, and daily presence in national and international capital markets for the benefit of our 75 client countries. Let me give you some concrete examples from the work we are doing with Indonesia and South Africa.

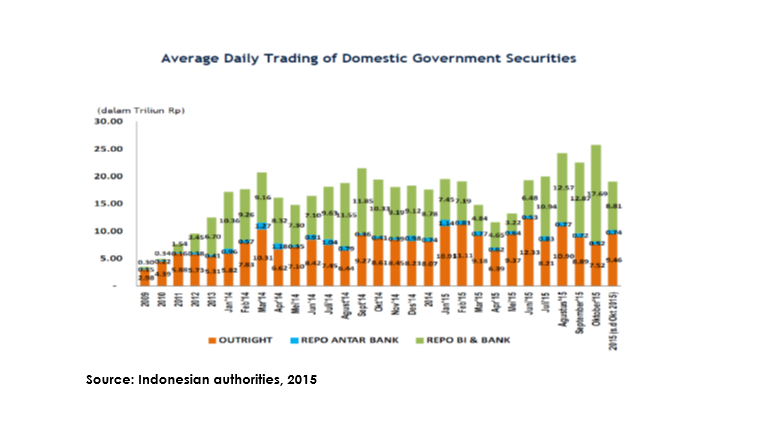

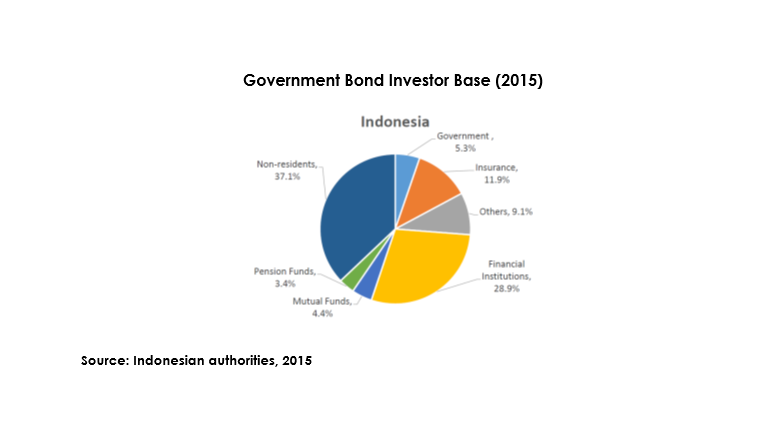

As you know, government bonds are the backbone of fixed income markets. They provide a benchmark yield curve and help establish the overall credit curve for the whole economy. This is in addition to meeting the fiscal needs of the government. Establishing a strong government bond market is therefore one of the early steps in developing domestic capital markets. This was indeed the case in Indonesia.

With the support of the World Bank, the Indonesian authorities have identified and pursued a series of strategic priorities in the development of bond markets, lately through the Capital Market and Non-Bank Financial Industry Master Plan 2010-2014, which set out a big picture view of desired technology and market developments. A comprehensive debt management strategy implemented by the debt management office and continuous reforms have ensured the smooth functioning of the government bond market. These reforms included: (i) the establishment of the Indonesia Bond Pricing Agency (IBPA), (ii) the establishment of a robust and efficient market infrastructure (trading, clearing and settlement); and (iii) the supply of a broad selection of government securities. As a consequence, the government has been able to establish a reference yield curve going out to 30 years, with some reasonable liquidity. We are proud to have been able to support Indonesia, particularly by partnering with the debt management office, to improve debt management in line with international best practice.

This is, however, a long road and we continue to partner with Indonesia to help elevate the government bond market to the next level. For Indonesia, this means reducing the weight of non-resident investors by growing the local investor base, to include most notably, pension funds, insurance companies and mutual funds. A diversified investor base can reduce herding and hence, the impact of shocks. Different investor groups have different risk appetites and liability structures and tend to react to new information in different ways.

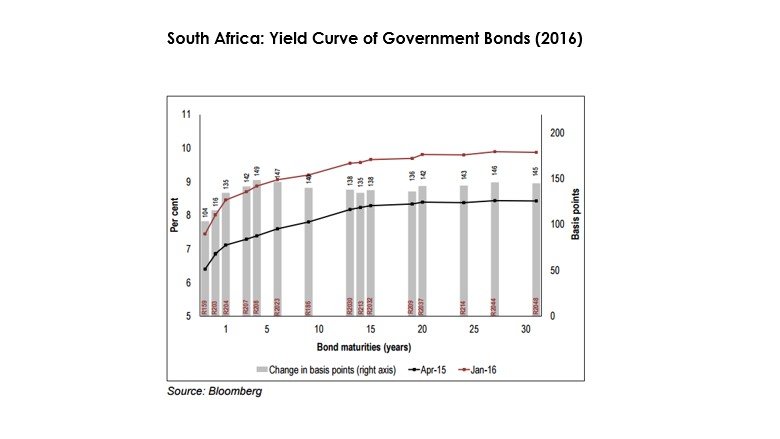

In South Africa, the World Bank is supporting the government in establishing an electronic trading (ETP) platform. As most of you probably know, this is a country with a deep government bond market with various market players including banks, institutional investors, and brokers. South Africa enjoys a well-developed yield curve extending out to 30 years thanks to active over-the-counter secondary market trading. The government is looking to improve the financial market architecture to increase market transparency and improve the functioning of both the primary and secondary markets. Once implemented, the electronic trading platform model proposed by the World Bank will be instrumental in better price discovery, higher liquidity, and improved transparency.

The World Bank and IFC have each done significant work raising the global visibility of fixed income markets in developing countries, adding product and credit diversity to domestic markets. The World Bank, which works primarily with governments and public entities, enables international investor awareness, through global bonds issued in local currencies. The IFC which has a private sector focus, is a global leader in domestic bond markets.

First, let me describe the World Bank “World Supporter Fund”. It is a unique mutual fund, which allows investors to buy shares of a professionally managed, globally diversified emerging market currency fund made up of World Bank bonds. This fund is designed to enhance investor awareness of frontier local currency markets, and specifically, World Bank bonds issued in these currencies. We established this fund in partnership with an asset management firm with just over US$100 million and in seven years have raised more than US$7 billion from mainly Japanese investors in 290 separate bond issues, in 22 different currencies. For several of these currencies, the bonds issued by the World Bank were first time bond issues by a foreign issuer in the currency. These bond issues have subsequently attracted investors from other parts of the world, and many were reopened to fill new international demand from Europe and the United States.

Second, IFC is a leader in using domestic bond programs to fund its local investments in its client countries. Since its first landmark bond in the West African CFA Franc in 2006, IFC has created issuance programs in many domestic markets in many regions of the world. Through its issuance program, IFC brings international best practice to areas such as legal documentation, clearing and custody of securities. The bond issues raise awareness of local markets with international investors and intermediaries and often lead to “crowding-in” of international demand for domestic sovereign and corporate issues.

Let me highlight the important role of supranational entities in attracting foreign investors into a local market using a 10-year World Bank Turkish lira bond, issued in 2007. At the time of issuance, this bond had the longest maturity in the currency – five years longer than the longest government bond. This was possible due to the government’s open attitude towards foreign issuer participation and developments in both cash and derivatives markets. One investor in this bond was a US State pension fund that wanted exposure to the currency and interest rate, but was not prepared to take the credit risk of the government or establish custody arrangements to buy local bonds. Once this fund had the exposure to the World Bank bond, it established internal protocols to monitor its risk position and became increasingly comfortable with the credit and market. A few months later, after partially accessing the market using the “bridge” provided by the World Bank, the pension fund took the necessary steps to buy the government bond obtaining higher yielding assets, liquidity and diversifying its investment options. It subsequently remained an active player in that market. I suspect this facilitated the success of the 10 year domestic benchmark bond that the Turkish government now regularly issues.

At the World Bank we see thousands of projects with social impact potential that could be matched with funds interested in bringing these causes to the market. You probably have had the same experience in your respective countries and can share the frustration of seeing these types of projects left unfunded. IBRD and IFC have been leaders in addressing this challenge. In fact, IBRD issued the first plain vanilla green bond in 2008. This green bond combined earmarked proceeds for climate change lending and external, third party opinions of the soundness of the principles used for project selection. To date, IBRD has raised a cumulative US$8.5 billion in more than 100 green bonds in 18 currencies, attracting new investors globally and raising awareness about climate focused investments in developing countries. We are also contributing to the development of this important segment of the capital markets by advising other issuers and sponsoring the principles that guide green bond issuance.

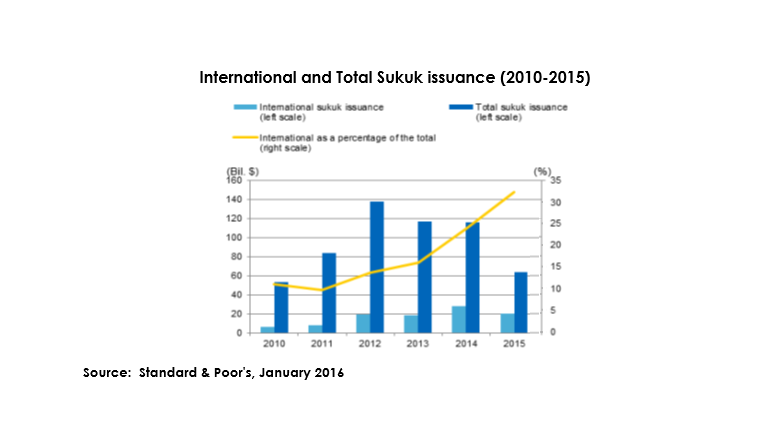

One area of the capital markets that has experienced particularly rapid growth is the Islamic Sukuk market. This market, which barely existed 15 years ago, has seen at least $100 billion of new international issuance annually since 2012. While still only a fraction of the global bond market, Sukuks have become a viable funding option for issuers, including those outside the Islamic world. In 2014, for example, we saw first time international sovereign Sukuk issuance from South Africa, the UK, Hong Kong and Luxembourg.

More generally, growth in Sukuk is a consequence of an increasing demand for Sharia-compliant assets in the Islamic world as well as its utility for infrastructure financing. One promising prospect for the Sukuk market is the potential overlap between Sukuk and conventional socially responsible investing or “SRI.” Islamic finance and SRI investors both look for investments that not only make sense financially, but also conform to their beliefs. We see a compelling market opportunity for socially responsible Sukuk that could appeal to both sets of investors. In fact, we have empirical evidence that just such a convergence of investor bases is possible.

Since December 2014, the World Bank, as treasury manager for the International Finance Facility for Immunization or “IFFIm,” has issued US$700 million of Sukuk, in two separate transactions, to fund the immunization of children in many of the poorest countries of the world. These transactions appealed to both traditional Sukuk investors in the Gulf and Southeast Asia and to European SRI investors, some of which had never purchased sukuk before. These transactions won six separate international awards for innovation and market development, including the Financial Times’ Top Achievement in Transformational Finance Award and Euromoney’s Islamic Finance Initiative of the Year. The visibility afforded by these transactions and the follow-on success has attracted a number of issuers and non-Islamic investors to this fast growing market.

Additionally, the World Bank continues to offer interest and currency conversions to help client countries manage their liabilities. The Bank leverages its presence and preferential pricing in the markets, to pass on cost savings to clients. This includes conversions of World Bank loans and more recently has been expanded to include conversions of clients’ other foreign currency denominated debt. For example, in South Africa, we were able to provide local currency financing to a sub-sovereign entity by conducting sizable, multi-decade swaps into South African rand. Countries like Colombia, Mexico, Uruguay and Turkey have also benefitted from similar local currency financing. We also helped Morocco convert a US$1 billion dollar 10-year Eurobond issuance into EUR, in line with its debt management strategy.

Executing lending and funding transactions in local currency, relies on the use of cross-currency swaps, which has an added advantage of contributing to the expansion of these markets by providing more liquidity, especially in long tenors. We provide dedicated training on the use of derivatives to public debt management officials in our client countries to help build capacity for dealing with derivative products.

Guarantees are also important vehicles for developing capital markets, expanding access to financing and mitigating risks. The World Bank Group, through the Multilateral Investment Guarantee Agency or MIGA, has helped Senegal access the cross-currency swap market by providing a guarantee to market dealers, enabling the sovereign to hedge its Eurobond issues in USD into EUR.

We also help countries access the capital markets through the use of credit guarantees. Recently, Ghana issued a 15-year $1 billion Eurobond with an IDA Policy Based Guarantee of $400 million. It was one of the longest international currency bonds ever issued in the Africa Region. Given that the transaction was executed in an extremely challenging market environment, the credit enhancement allowed Ghana to access the market, while extending the maturity of the issuance and obtaining good pricing.

Notwithstanding the urgent and ongoing need to continue building markets for traditional finance, there are a great number of non-traditional products and areas that are increasingly being used across the globe to address today’s unique challenges. We are facing commodity price shocks, weather catastrophes –which threaten infrastructure, and amplified volatility in foreign exchange markets. In response, we are seeing technological improvements in risk mitigating tools, a fast growing sector of investors interested in environmental and social impact, and an increased number of collective approaches to problem solving between donors and regional groups of recipients.

A particularly exciting area of development is weather and catastrophe risk mitigation. The World Bank offers contingent financing and direct loans to deal with the aftermath of natural disasters. We have also played a leadership role in the development of the market for disaster risk management in emerging markets, having executed or arranged 19 market transactions to date for a total of US$1.5 billion on behalf of Bank clients. We have assisted in several key transactions around the world, as arranger of catastrophe bonds for Mexico, as market intermediary for contracting rainfall hedges in Malawi and Uruguay, to executing hurricane and earthquake damage protection transactions for groups of similarly exposed nations in the Caribbean and in the Pacific. The Caribbean and the Pacific transactions, which are rolled over year after year, are good examples of small size countries with limited access to the market joining together to buy protection against hurricanes and cyclones under global coverage, therefore benefiting from economies of scale and lower costs due to diversification. It is worth noting that a country’s size and stage in development does not limit its use of cutting edge, capital markets instruments.

We are also working on designing innovative financing structures to leverage donor funds to help support special initiatives. Following the experience of leveraging donor money for immunization, the Bank is now designing a multi-donor structure to channel contributions to support countries in the Middle East affected by the refugee crisis or in need of reconstruction. We are working everyday with our partners to expand this list. Let me call on you too to do your part to create strong and resilient markets that can drive and sustain developmental gains.

I have highlighted several examples of our work at the World Bank Group to share with you the variety of ways we can partner with you.

Let me conclude by reiterating three key messages:

The world needs world class capital markets for economic and social development, ending extreme poverty, boosting shared prosperity and tackling the world’s most difficult challenges.

Only smart capital market regulation will build world class capital markets. Smart regulation entails fostering best practice standards, transparency, efficiency and innovation. Its foundation is however market integrity.

Building market integrity requires capital market regulators that are competent, committed and courageous. It may require great sacrifice and you may even face threats to your life. You will however feel fulfilled when you see the huge difference that your efforts are making. David Saperstein’s 1935 letter to Joe Kennedy, the first Chairman of the US SEC, suggests so. He noted in the letter, "The [US SEC] will undoubtedly make new advances and arrive at fresh triumphs. But whatever it achieves, the men and women who have toiled for it during its infancy, who have nourished it and cherished it, will remember that it was Joe Kennedy’s strength and courage and Herculean labors which really put it over."

As with Joe Kennedy, you can painstakingly build a world class capital market that other nations will seek to replicate.

Thank you.