This piece first appeared in the National Newspaper

Like their peers around the world, firms in the Middle East and North Africa region (MENA) have been deeply impacted by the COVID-19 shocks. One year into the pandemic, firms' recovery looks highly uncertain in MENA countries. Nonetheless, the impact on firms differ from other regions in a few unique ways.

To gather timely information about how firms are affected and navigating through the pandemic, the World Bank, often in partnership with national statistical offices, has been implementing the COVID-19 Business Pulse Surveys (BPS). Since May 2020, the BPSs have covered more than 50 countries — including Algeria, Djibouti, Morroco, Tunisia, Jordan and the West Bank and Gaza from the MENA region — with more than 100,000 businesses from different regions and countries of different sizes and income levels. Other MENA countries could still benefit from participating in the survey to generate timely information for policy makers to help firms cope and recover.

The MENA BPSs findings highlight that the key channels through which the COVID-19 pandemic affected the firms include revenue loss, financial distress and job loss. However, despite a drastic fall in business activities and sales, most MENA firms have been holding on to their workers and slow in adopting technology, possibly resulting from the underlying social contract in MENA. The surveys also show that MENA firms remain highly uncertain about the recovery and view a sharp decline in demand, production and work hours, while many also fear future pandemic waves and lockdown. While most of the firms seem to re-open at some capacity, a non-trivial share of firms (10-20%) across MENA's surveyed countries remains closed.

Job Losses

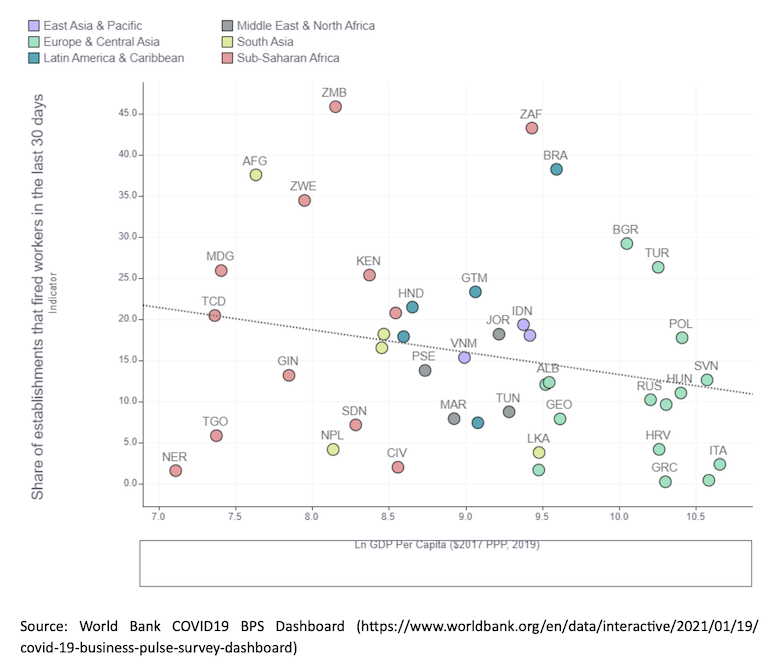

A significant share of MENA firms (e.g., 14% in the West Bank and Gaza and 17% in Algeria) have reduced their permanent employees. Nonetheless, the share of MENA firms that laid off workers seems to be less than that in some other regions (see figure 1). Most MENA firms have been trying to hold on to their permanent workforce in attempting to make adjustments by providing leave (often without pay), reduced work hours, salary reductions, and reduced temporary workers. Nonetheless, the persistent decline in sales and a prolonged pandemic episode risk permanent job loss for MENA firms. For example, while during the early stage of the pandemic (i.e., during July-August 2020), 26% of firms in Jordan reduced their permanent workers, 39% did so during November 2020-January 2021.

Figure 1: Share of Firms Laying Off Workers in Different Regions

Revenue loss and firm closure

The pandemic has negatively impacted 92% of the firms in the West Bank and Gaza (WBG) and 89% of the firms in Djibouti, Tunisia and Jordan. For most of these impacted firms, the sales have declined by more than 50% from the pre-COVID-19 situation. This magnitude of firm-revenue loss in MENA is in line with what has been experienced on average by the firms in developing countries.

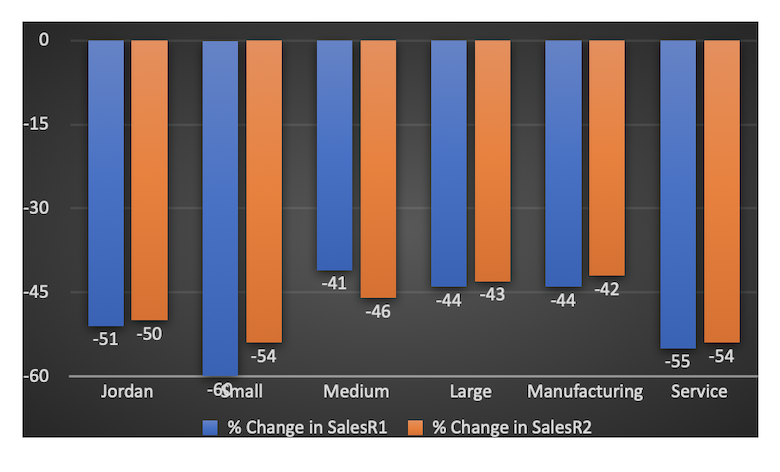

Across the developing world, the loss of sales appears to be persistent, which is also likely to be the case in MENA countries. For instance, in Jordan, where 601 firms were surveyed between May and November 2019 (i.e., pre-COVID-19 context), and then subsequently between July and August 2020 (COVID-19, round 1) and again between November 2020 and January 2021 (COVID-19, round 2), showed that the average decline in sales seems to be persistent around 50% in both the COVID-19 survey waves (see Figure 2). Moreover, smaller firms and firms in the service sectors seem to be affected the most.

Unable to cope with the persistent decline in sales, a significant share of firms across MENA countries, particularly smaller firms, have permanently closed down their businesses. For instance, 17% of firms in Jordan during November 2020–January 2021 found their businesses to be permanently closed; this share is up from 11.6% during the early stage of the pandemic (i.e., between July and August 2020). Similarly, while on average, around 9% of firms seem to close their businesses in Morocco permanently, that share is 11% for small firms while 2% for large firms.

Financial Distress

The declining revenue has left most firms in financial distress. Nearly 90% of firms in the West Bank and Gaza, 93% in Jordan, 78% in Tunisia, and 72% in Morocco reported a decline in cash-flow. Financial distress seems to be most acute for smaller firms. Delaying payments to suppliers, landlords, or tax authorities and being overdue on obligations to financial institutions have been adopted by most firms to cope with the declining cash-flow. Besides the financial distress, disruptions in transport and logistics and supply of inputs appear to be some of the key impediments the MENA firms face.

Figure 2: Average Change in Monthly Sales Compared to the Prior Year for the Two Rounds of the Surveys

Notes: The R-1 series shows the average change in monthly sales in June/July 2020 vs. June/July 2019, and R-2 shows the average change in monthly sales in November 2020 – January 2021 vs. November 2019 - January 2020. Source: World Bank BPS.

Going Digital as a Coping Mechanism

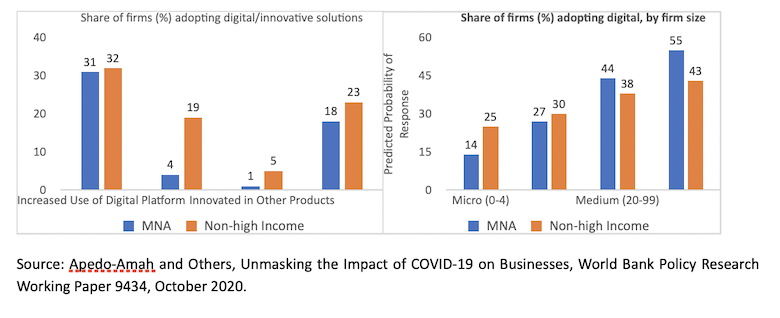

Despite its multiple adverse impacts, the COVID-19 pandemic motivated firms across the developing world to leapfrog and take advantage of digital technologies. The digital presence also seems to be an essential coping mechanism for a significant share of firms (20-30%) across MENA's surveyed countries. Increased use of the internet, online social media, specialized apps, or digital platforms seems to be some of the firms' essential tools to continue business operations, sales, or seeking supplies of inputs and raw materials.

Nonetheless, MENA firms have considerable scope to catch-up with their peers on digital solutions (see figure 3). Moreover, the gap between micro and small firms and the large firms in digital technology adoption is the highest in MENA. Several structural impediments in many MENA countries are likely to inhibit firms' digital technology adoption and innovation. These include a high degree of informality, particularly among the micro and small firms, lack of digital payment solutions and services, underdeveloped and costly digital infrastructure (contributed by lack of competition in the network industries), and the lack of domestic competition and export competitiveness that reduces the incentive to innovate.

Figure 3: Digital Adoption During COVID-19

Policy Support

The majority of the MENA firms stated they need subsidies or deferral for utility and rent payments, tax exemptions and deductions, and salary subsidies as priority policy support. Policy support in different MENA countries enabled firms to avoid falling into arrears and cope with uncertainty. However, based on BPSs in different MENA countries, it appears that the policy support is reaching to a minority of firms. For instance, while 33% of firms in Jordan reported receiving government assistance, that share is less than 10% in Algeria and Tunisia. A well-targeted, time-bound, and effective policy support will be much needed to keep the MENA firms afloat and able to navigate through the turbulent waves of COVID-19 shocks.