At a recent Policy Research Talk, World Bank Lead Economist Leora Klapper presented key findings from the Global Findex 2021—a nationally representative survey of adults that has taken place roughly every three years since 2011 and quantifies financial account ownership and usage in economies around the world. Initially delayed by the outbreak of the COVID-19 pandemic, the Global Findex 2021 captured data from more than 128,000 adults in 123 countries—bringing the global total of survey participants to more than half a million adults since 2011.

The talk spanned subjects such as the impact of mobile money on financial inclusion and equity in Sub-Saharan African and other economies; how COVID-19 influenced changes in financial usage patterns, particularly for digital payments; new insights on financial resilience; and how focused policies and well-designed products can help close remaining inclusion and usage gaps.

In the aggregate, the Global Findex 2021 shows much cause for celebration among financial inclusion advocates. Since the first Global Findex survey in 2011, the share of adults worldwide with a financial account rose from 51 percent to 76 percent. In developing economies, account ownership has increased by 30 percentage points, bringing the total account ownership for adults in developing countries up to 71 percent. Digitalization facilitated that increase, as millions of adults opened accounts and began using them.

“Financial inclusion means that adults have access to appropriate financial services and can effectively use them to safely manage their money, save, and invest in their financial wellbeing,” said Klapper.

An impressive array of research has tallied the many benefits of financial inclusion, including enabling greater investments in businesses, increasing control over money (especially for women), reducing fees and increasing the security of money, and helping households cope with shocks through savings and insurance.

The trends driving increased account adoption and usage were already underway when the COVID-19 pandemic struck and catalyzed remarkable digital payment adoption as a work-around during lock-downs and other restrictions.

Three key messages emerged from the Global Findex 2021

To paint a picture of the current global situation surrounding financial inclusion, Klapper summarized three key messages from the Global Findex 2021 data and accompanying report.

The first message highlights the importance of technology-enabled accounts. Digital financial services such as mobile money, cards, e-wallets, and direct account-to-account payments have driven tremendous growth in account ownership and account usage around the world.

The second message emphasizes the way in which increases in financial inclusion have gone hand-in-hand—at least at the global level—with reductions in the account ownership gender gap. On average in developing economies, the gap between men and women in account ownership fell to six percentage points for the first time in the past decade.

The third message is that the COVID-19 pandemic accelerated the use of digital payments. During the pandemic, digital payments helped governments transfer money to those who most needed it, supported consumers when the use of cash was not possible, and became a lifeline for many small businesses.

The impact of digital financial services on account adoption and usage

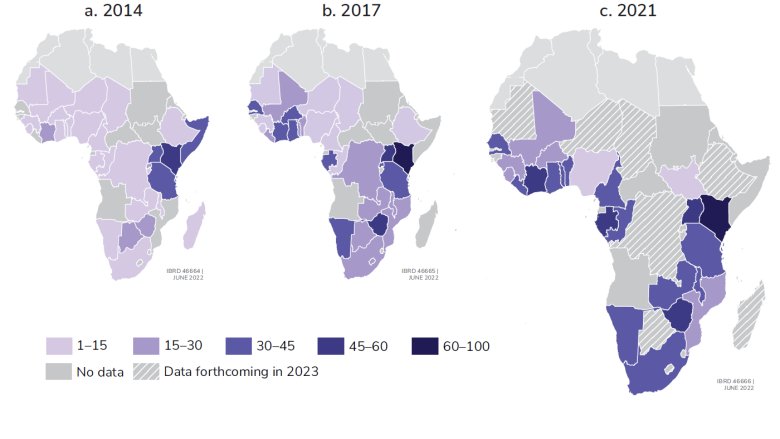

Mobile money accounts offered by telecom and fintech companies have been a key enabler of financial inclusion as well as a major contributor to the increase in account ownership in Sub-Saharan Africa, as well as in select economies such as Bangladesh and Peru (Figure 1).

“Mobile money accounts, which are easily accessible and offered through companies already familiar to the user, can be less intimidating and more convenient,” said Klapper. “Mobile money is also designed for small, high frequency transactions—which is exactly what they are being used for.”

Figure 1: Visualization of Mobile Money Accounts in Africa for 2017, 2017, and 2021

Mobile money accounts have increased dramatically since Global Findex data collection began.

The gender gap has narrowed, though there is still room to prioritize equity

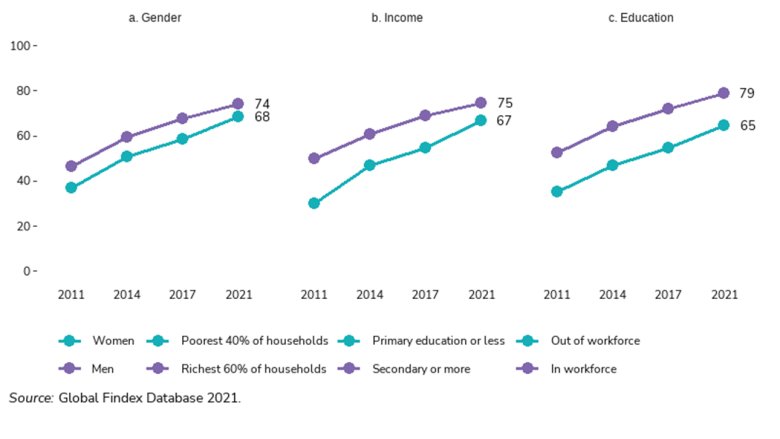

Despite recent advances, key gaps in account ownership still exist based on gender, income, and education levels (Figure 2). While social norms undoubtedly play a large role in the gender gap, more resolvable regulatory and technical issues are also at play. For example, men in some countries are more likely than women to have valid documentation such as government-issued IDs, which people need to open a financial institution or mobile money account as well as to purchase a mobile phone and SIM card.

“In Pakistan, for example, 88 percent of men have their own phone, compared to 42 percent of women,” said Klapper. “This presents a barrier for financial and digital inclusion as well as e-commerce opportunities, online education opportunities, and more.”

Figure 2: Three Key Gaps in Financial Inclusion

Account Ownership in Developing Economies by Gender, Income, and Education

Adults now use a variety of financial services—and COVID-19 catalyzed wider adoption of digital payments

Digital payments are the most popular financial service. Fifty-seven percent of adults in developing economies made or received a direct payment in 2021, compared to only 35 percent in 2014.

One type of payment that has been enabled by account adoption is domestic remittances. In many countries across Sub-Saharan Africa, mobile money accounts were originally marketed as an option for domestic remittances (both sending and receiving). Now, mobile money account holders use them for a variety of financial services, including saving. More broadly, saving in any kind of account saw a boost in 2021—for the first time, more than half of adults who chose to save did so through a formal account, whether provided by a bank or similar institution or a mobile money provider.

Payments are a gateway for further financial inclusion

Governments and other actors can leverage the trends in digital payment adoption to further spread the benefits of financial inclusion to the approximate 1.4 billion adults worldwide who still lack a financial account. Digitizing payments is a start.

One third of the adults who receive government payments still receive them in cash or through some method other than directly into an account. Government-led policies could help put more of these payments into accounts and thus enable safer access and usage.

“The goal of financial inclusion is to design the right financial products and digitize payments in a way that enables people to alleviate their biggest worries, like saving for emergencies, making sure they can pay their bills, and having a secure place to keep their money,” said Klapper. Addressing the remaining barriers for adults in opening financial accounts and achieving financial security remains a key priority area for research and policy.