Over the past few decades, a growing body of evidence has pointed to the importance of an efficient and stable financial sector in enabling growth, supporting firms, and reducing poverty. While banks play a critical role in this process, capital markets in the form of debt and equity are especially important in supporting the growth of new firms, which can help drive higher productivity and create new jobs. Over the past decade capital flows to emerging markets have grown tremendously, but have they delivered on their promise?

At a recent Policy Research Talk, World Bank research economist Alvaro Pedraza highlighted the case of Colombia to begin to answer this question. While data on the role of banks in international finance is relatively comprehensive, much less is known about international flows of debt and equity. Working together with Universidad de la Sabana and Bolsa de Valores de Colombia (Colombia Stock Exchange), Pedraza was able to piece together a complete picture of all transactions and ownership of Colombian stocks and bonds since 2006—a truly remarkable window into an otherwise opaque world.

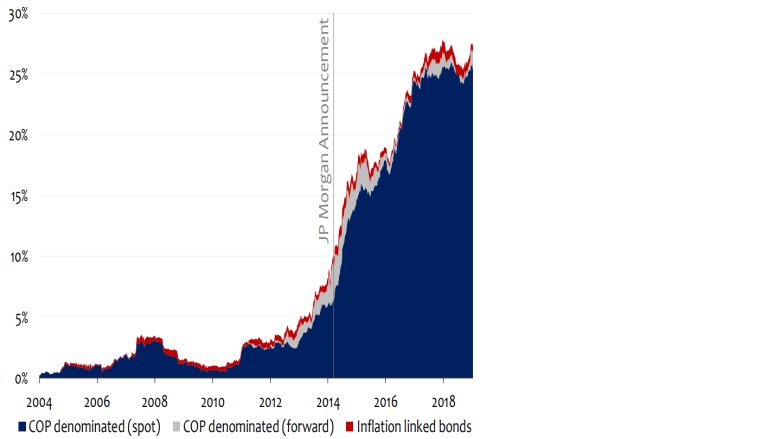

As Figure 1 shows, Colombia is no exception to the broader trend of growing international capital flows into emerging markets. Up until the mid-2010s, the holdings of sovereign bonds by non-residents as a percentage of total debt were miniscule. Things looked very different by 2020, with holdings of sovereign bonds by non-residents reaching more than 25 percent of total outstanding debt.

Figure 1: Holdings of Colombian Sovereign Bonds by Non-Residents: Until the mid-2010s, holdings by non-residents in Colombia were small, but have grown substantially since. (Romero et al., 2020)

Pedraza first turned his attention to a basic but fundamental question: how have stock prices responded when demand has gone up for stocks of Colombian firms? To answer this question, Pedraza and his co-authors examined what happened after Colombian firms were added to or removed from Morgan Stanley Capital International (MSCI) Indices—a group of international indices of stocks tracked by many types of global investors. Following the announcement that a particular company would be included in one of these indices, active investors quickly bought significant amounts of stock, followed many days later by passive investors once a given stock was finally added to MSCI. Hedge funds counteracted this upward pressure, but their activity proved too small to have much of a countervailing effect, resulting in a large increase in stock prices. According to Pedraza, for every one percent increase in demand for a stock, prices increased on average by three percent.

Research has found that this type of increased demand has real effects on the economy. For example, inclusion of Colombian government bonds in the JPMorgan Emerging Markets Sovereign Bond index was followed by increased credit availability in municipalities. However, Pedraza pointed out that over the time period he examined the number of listed companies on the Colombian stock market declined, with more delistings than initial public offerings even as foreign finance in Colombia increased. This fact suggests that increased finance alone had a limited impact on stock market development, as measured by a smaller total market value and fewer listed companies.

Pedraza’s second set of findings helps illustrate one reason why more finance alone is not enough. Like many middle-income countries, Colombia’s economy is dominated by business groups—collections of legally independent companies with a significant amount of common ownership. These overlapping interests often include institutional investors, which often face incentives that blunt their ability to act as impartial market participants.

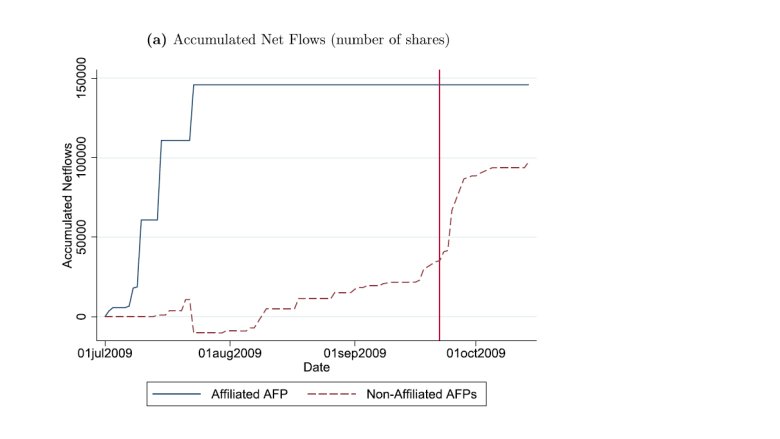

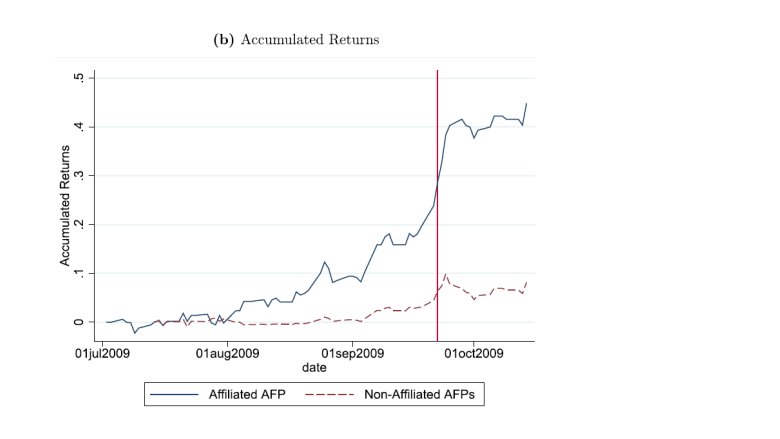

In fact, Pedraza’s research found evidence of exactly this. Institutional investors affiliated with business groups traded stocks of affiliated companies prior to public announcements of corporate news, earning outsized returns (Figure 2). While trading stocks of affiliated firms might benefit institutional investors and incumbent firms, it is detrimental to the overall health of the market. It dissuades outside investors from participating, raises the overall cost of capital, and ultimately contributes to making it more difficult for new and innovative firms to raise equity finance.

Figure 2: Trading Around Corporate News: Graph A shows that institutional investors affiliated with business groups traded in advance of public corporate news announcements. Graph B shows the higher returns that accrued to affiliated institutional investors.

The challenges in developing effective capital markets don’t stop with firms and institutional investors. Pedraza also highlighted research on retail investors that demonstrates the risks for individual investors. A national program in Colombia provided classroom training to nearly 20,000 students on the basics of stock market investing. Pedraza found evidence of a phenomenon that is perhaps as old as stock markets themselves—peer influence in the classrooms led inexperienced investors to adopt risky investment strategies. Students with previous exposure to stock investing who had gotten lucky with high volatility investment strategies had an outsized influence on these new investors, promoting overtrading and the adoption of risky strategies, which often led to underperformance. In the absence of better regulation and education, active trading may be very costly for individuals and potentially even become a threat to financial stability.

The findings from this body of new research point to three key policy lessons. First, good data is crucial in revealing opportunities and challenges in developing equity and bond markets. Second, evidence of access to private information by institutional investors points to a broader need for more transparent disclosure requirements, better financial market regulation, and improved enforcement. Third, the social transmission of volatile trading strategies points to the need to better reach people with accurate information—especially those who hold central positions in social networks.

“This body of research is just a start to better understanding the evolving role of international capital flows in developing countries,” said Pedraza. “Given the current lack of comprehensive global data, I hope these results can serve as a call to regulators to better coordinate data collection and analysis around this increasingly urgent topic.”