The war in Ukraine has compounded the damage left by the COVID-19 pandemic and magnified the slowdown in the global economy. The risk of stagflation is increasing with potentially harmful consequences for middle and low-income economies alike. So what do the next few months have in store for the global growth? The latest edition of the Global Economic Prospects projects global growth will slump from 5.7 percent in 2021 to 2.9 percent in 2022. To help us learn more, Director of the World Bank’s Prospects Group, Ayhan Kose joins Expert Answers to discuss.

Timestamps

00:00 Introducing Ayhan Kose, Director of the World Bank’s Prospects Group

00:46 Headlines of the Global Economic Prospects, June 2022

02:07 Breaking down growth by income groups and regions

03:32 Downside risks ahead

06:06 Stagflation

10:17 Navigating stagflation without creating debt and financial crises

12:15 The case of the Middle East

14:02 Rising food prices, rising food insecurity

16:49 What can national policy makers do

20:11 Thanks Ayhan for sharing your expertise!

Transcript

[00:00] WB Expert: Things have gotten, unfortunately, much worse than what we expected. We were expecting a slowdown, that slowdown is much more pronounced now.

Host: On this episode of Expert Answers, forecasting the future of the global economy amid multiple shocks. There was the COVID-19 pandemic, now there's the war in Ukraine. Both are continuing to hit economic growth. The latest data from the World Bank Group warns of the sharpest deceleration in economic activity in 80 years. So what's driving this, how bad could it get, and are we headed for this so-called stagflation? For answers to this and more, we turn to the World Bank's Prospects Group's Director, Ayhan Kose.

[00:46] Host: So Ayhan, you and your team prepare the Global Economic Prospects every January, every June. We check in with you to see what you're forecasting. When we spoke in January, you talked about a pronounced slowdown in the global economy. What are the headlines for this edition of the report?

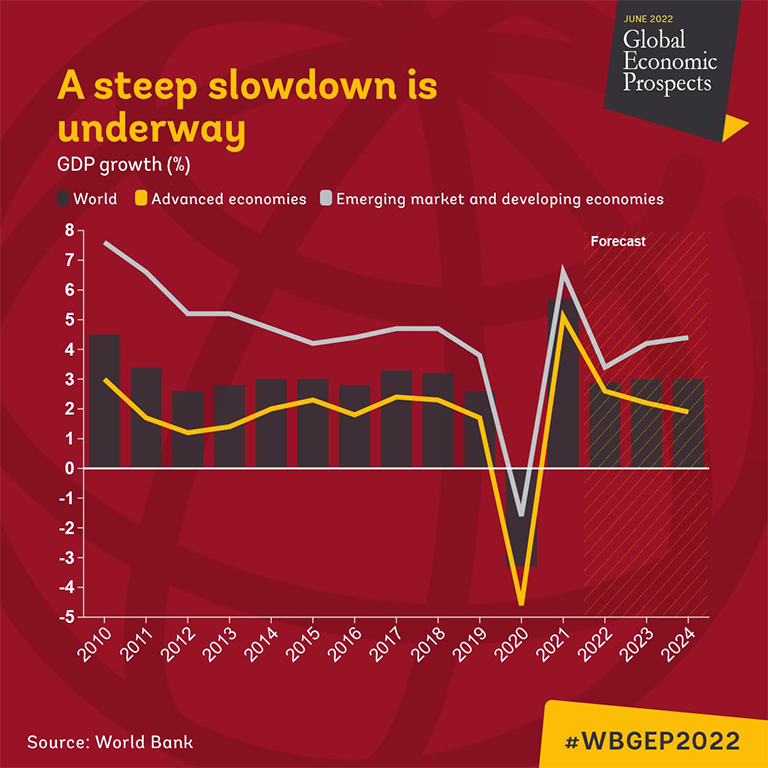

WB Expert: Things have gotten, unfortunately, much worse than what we expected. We were expecting a slowdown, that slowdown is much more pronounced now. Growth is going to go down to 2.9%. At the global level, last year it was 5.7%. So global economy is facing overlapping crisis. Of course, we have the war in Ukraine and its repercussions. We have increasing interest rates, tightening financial conditions. And the third crisis that's still with us is the health crisis. Of course, the COVID showing its ugly face in different parts of the world, as we see in China.

WB Expert: So it is a difficult period for the global economy. Demand is going to slow. There was pent-up demand last year. There was significant policy support that's being withdrawn, and we have supply disruptions still there. And we are going through one of the largest commodity shocks we have seen over the past 50 years.

[02:07] Host: I want to ask you about stagflation in a second. But first, that headline figure the 2.9% growth, what does that look like when you cut it by income groups by regions? Can you break that figure down a little bit more for us?

WB Expert: That is very important. Yes, the growth slowed, but what happened is that because of the war in Ukraine, it is repercussions how commodity prices have been increasing, how inflation has been rising. We have a serious food crisis around the world. As I mentioned, we have supply disruptions. But what happened is that we downgraded forecast across the board. In the case of advanced economies, forecast are downgraded. In the case of emerging developing economies, forecast are downgraded.

WB Expert: And then you look at the global economy as a whole, we downgraded growth numbers for this year for 70% of countries relative to what we had in January. Now for advanced economies, we're expecting growth to slow from 5.6% last year to 2.6% this year, and growth will continue slowing next year. For emerging market developing economies, growth is going to slow from 6.6% last year to 3.4% this year. So the slowdown is highly synchronized and risks are quite sizeable confronting the global economy.

[03:32] Host: One of the things that strikes me is, when we spoke in January, the idea of the war Ukraine was pretty unthinkable at that point. We're now over a hundred days into that conflict. These risks, they come at you fast. Talk about the downside risks here. What's the worst that could happen over the next few months?

WB Expert: Now, because of the war, we have a much larger menu of risks. And these risks, unfortunately, they mutually amplify each other. So Russian invasion of Ukraine escalated geopolitical tensions. Of course, those geopolitical tensions can easily intensify.

WB Expert: We have a very serious threat of stagflation that comes with higher interest rates. Higher interest rates come with the risk of financial stress. We still see supply disruptions. Because of the war, those supply disruptions, of course, magnified. There is risks associated with even larger food prices down the road. And when you have these types of challenges, the risk of social tensions, of course, increases.

WB Expert: Now, over the medium-term, we are worried about the fragmentation of trade investment and financial flows. And we are, of course, worried about even weaker growth than what we are expecting. This is, by the way, on top of the climate-related challenges global economy is facing.

WB Expert: Now, what is the big challenge when we think about these risks? I think one issue is the, of course, the intensification of geopolitical tensions. It is implications for commodity markets. Another one is the faster than expected tightening of financing conditions because of policy interest rates going up and COVID-related disruptions.

WB Expert: When you put three of them together, if those three risks materialize, we can easily find ourselves in the midst of a perfect storm. That type of storm will push growth rate this year to 2%, and next year, at the global level, 1.5%. And when you have growth rate at the global level around 1.5%, that means you are in a very serious, severe downturn.

[06:06] Host: You mentioned a second ago the word stagflation that caught my ear, remind us what exactly that is, and is that your call? Are you saying we're in stagflation, we're headed towards stagflation? What exactly is the call here?

WB Expert: Now, stagflation is a concept that basically describes you have high inflation and weak growth. It is a toxic mix. For economists, it is the type of problem difficult to overcome. Now, you need to, of course, find a way to increase supply so you reduce price pressures or to reduce demand. Again, to reduce price pressures. But both of them of course have its own challenges.

WB Expert: Most people think about stagflation is a problem specific to the US. It's a global problem. Now you look at inflation rates, inflation nowadays around the world close to 8%. That is the highest rate we have seen since 2004. Now, when you think about inflation in emerging market developing economies, it is above 9%. Again, one of the highest rates we have seen in this past two decades.

WB Expert: Now what the policy makers are going to do, as we have seen already what Federal Reserve is doing, is going to increase interest rates to contain flat price pressures, and that comes with weaker growth.

Host: Because the rising interest rates dampen growth. The problem is you already have slow growth.

WB Expert: Yes. So we are in the midst of a slow down, and we need to basically cope with the problem of stagflation. So, in a sense, you what the solution is if you are going to solve the problem with monetary policy, but there is a side effect associated with that. And that side effect is not the side effect you would like to see, even weaker growth. Now, here that we have one episode of stagflation in the 1970s.

Host: Because we often think of it in a US context, stagflation that it was here in the US. It was in the '70s. But it's a global phenomenon, and it hits developing countries quite hard.

WB Expert: Yes. In the '70s as well, stagflation was a global challenge. Now it's a global challenge because we have highly synchronized inflation and we have a highly synchronized slowdown when it comes to growth. In the '70s, we had commodity price shocks in the mid-'70s, at the end of '70s. And now again, we have commodity price shocks quite sizable. In the '70s, we had a long period of monetary policy accommodation. We had exactly the same thing in 2010s.

Host: Rates were really low. There were policies in place to try to increase growth.

WB Expert: Exactly. So rates were so low, real interest rates were negative in the '70s, as well as what we have now, of course, in 2010s.

Host: But that also increases inflation when there's that accommodating policy.

WB Expert: This accommodating policy. And, of course, the challenge now, are there good reasons to be optimistic? There is at least one good reason. In the '70s, central banks did not have the type of monetary policy frameworks they have now. In the '70s, they were targeting multiple things, the employment output, inflation. Now, they have a clear inflation stability mandate. They have three decades of credibility they built.

WB Expert: When you look at inflation expectations, long-term inflation expectations have been more or less stable, so that we need to see central banks, especially the major central banks like the US Fed and ECB, containing inflation with interest rate cuts, and hopefully they are going to do that without a hard landing.

[10:17] Host: And I imagine one of the fears here is that when the stagflation happened in the '70s, there was this monetary tightening. And that, if I'm not mistaken, that led to debt crises in a lot of countries. So the challenge here is navigating this stagflation without creating debt crises, financial crises in EMDs around the world.

WB Expert: So, Paul, history does not repeat itself, it rhymes. And unfortunately in this case, in the '70s, emerging developing economies accumulated significant amount of debt. And because of the delay in monetary policy response in advanced economies, there was a very aggressive monetary policy response at end of 1970s, early '80s, what we call Volcker disinflation. And with that, global economy went into a recession, a global recession, and there were a string of crisis, debt crisis, in Latin America, in low-income countries Sub-Saharan Africa.

WB Expert: Now when you look at what happened since 2010, we had an even larger, faster, and more synchronized debt accumulation in emerging-

Host: Debt is quite high right now.

WB Expert: ... developing economies. Yes. So that is quite high, and fiscal space is limited. Deficits are quite large. We are still trying to reduce the deficits from the pandemic era. And, of course, if interest rates increase quite rapidly, that is a serious threat for emerging developing economies with elevated debt levels and with debt in foreign currency. So the possibility of a string of debt crisis is in front of us because of the stagflation threat.

[12:15] Host: Shifting gears a little bit. One of the things that stood out to me in this addition of the Global Economic Prospects, we're seeing these growth downgrades across the board, we're seeing a economic contraction, negative growth being forecast for Europe and Central Asia. The Middle East sticks out as a place where it's actually, growth is going to accelerate. Can you explain that to us, and does that mean the Middle East is without its challenges?

WB Expert: Every region has a challenge. When you look at the headline numbers, Middle East, the North Africa region, is going to see higher growth this year relative to last year. That's entirely because of energy producers in the region. When you look at the importers of energy, and of course food, the region is not in good shape. As I mentioned, we downgraded the forecast across the board.

WB Expert: And the big challenge is that we want these countries, the countries in the Middle East, emerging market developing economies, to grow at rates, in per capita terms, faster than the growth rates of advanced economies. That's the only way they can close the income gap and their income get closer to the incomes of advanced economies and they have better living standards.

WB Expert: When you look around the world now, what you see, if you take out China, developing countries, per capita growth rates actually, through this year and the next year, will be slower than advanced economies per capita growth rates. What does that mean? They are going to be relatively poorer when you compare them with advanced economies, and that is the worst outcome we would like to see.

[14:02] Host: One other big challenge across the board, I'm sure this is the case in the Middle East, but across the board is rising food prices, rising food insecurity. What are you seeing in terms of what's driving that? How significant are the increases, and what needs to be done there?

WB Expert: The food insecurity was a problem, of course, last year. But with the war, Russian invasion of Ukraine, it reached a new dimension. So the type of increase we have seen in food prices since 2020 is third largest in over the past five decades.

Host: Wow.

WB Expert: So it's truly a historical food price shocks we are experiencing.

WB Expert: With the war in Ukraine, Russia and Ukraine being very large major producers of wheat, grains, maize, this has huge implications for how much supply is out there. Given Black Sea shipping routes close, of course, difficult to get Ukraine's harvest and that multiplies the problem.

WB Expert: And in that context, policy makers need to be extremely careful. There are certain policies we are recommending them to avoid, introducing export bans, introducing food and fuel subsidies-

Host: These need to be avoided

WB Expert: ... introducing price controls. In the past, these types of policies implemented, they were tested, and everywhere and always, they failed. There are political constraints. Policy makers, in some cases, need to employ these types of policies. If they employ, these policies need to come with clear sunset clauses. There are policies in the context of social protection, in the context of targeted relief efforts, those are the types of policies we are recommending policy makers to employ. And the worst thing policy makers can do now is to save the day and then have bigger problems down the road.

Host: So avoiding short-term gain for long-term pain.

WB Expert: Exactly.

[16:49] Host: It's better to look for something that would allow you to have long-term prosperity and sustainability. Zooming out from the food price issue, looking at the challenges across the board, I reckon we can kind of look at this two different ways. We can look at it as both the global community, what the global community can do, but we can also think about what can national policy makers do? What are some of the recommendations? If a finance minister were to phone you up and say, "Ayhan, what can I do to help my country? What can I do to help my region?" What would you tell them? What's the advice you're giving people?

WB Expert: Now, the global community has to deliver while the world economy going through an extremely difficult period. We are talking about multiple overlapping crises and ending the war is a priority. There is a humanitarian crisis in Europe taking place. We have the largest refugee crisis since Second World War. We need to make sure humanitarian relief efforts are there. In the context of Ukraine, in other parts of the world, there is conflict. And, of course, we just talk about the issue of food insecurity. These are the types of problems if you do not attend to at the global level, they can easily get out of control.

Host: And lead to other problems, presumably.

WB Expert: Exactly. And, of course, the global economy enjoyed for an extended period of rules-based global order, and that has brought a lot of dividends. We need to find ways to protect that rules-based international order and build on that. It's difficult to do given the war, but it is a public good, and we need to embrace that.

Host: And it'll lead to prosperity.

WB Expert: Of course. And at the national level, credibility of policies, obviously very important. Monetary policy, fiscal policy, financial policies, it starts with credibility when you are going through this type of difficult period. And, of course, we are talking about slowing economies with elevated inflation. That means calibration of policies.

WB Expert: If there is fiscal space that can be utilized, but it should be utilized in a manner that is targeted, well-defined. If there is revenue base, there is a need to expand that revenue base a bit further to generate revenue so you can actually help the segments of the society that needed most help. And eventually, policy makers need to have a well-defined, medium-term plan, and they need to communicate that plan clearly.

Host: Rather than firefighting crises in the short-term.

WB Expert: Exactly. Exactly. So I think that here we are discussing issues, the issues on the ground are more difficult, more complex than when we think about the big picture. Policies should respond to the local circumstances, but this is the time policy makers need to stick to the fundamentals and execute fundamental policies in the best way they can execute.

[20:11] Host: Ayhan, thank you so much. Really appreciate it.

WB Expert: Thank you. Thank you, Paul.

Host: If you found this interesting and want to take a deep dive into all of the analysis and data, be sure to check out the latest edition of the Global Economic Prospects, which you can find for free at worldbank.org/gep. This edition also contains a special chapter on so-called stagflation, including the first analysis of what this low-growth, high-inflation phenomenon means for developing countries. And, as always, we welcome your feedback. You can drop us line at expertanswers@worldbank.org.

Host: Until next time, goodbye.

ABOUT WORLD BANK EXPERT ANSWERS

Every episode of Expert Answers sits you down with a World Bank specialist: an expert answers with expert answers. From debt relief to gender equality. From COVID-19 response to inclusive growth, and much more. Our goal is to help you understand some of the biggest issues in international development today by asking our colleagues about what works on the ground and what we can do to meet the biggest global challenges. Watch previous episodes of Expert Answers!

ABOUT THE WORLD BANK GROUP

The World Bank Group is one of the world’s largest sources of funding and knowledge for low-income countries. Its five institutions share a commitment to reducing poverty, increasing shared prosperity, and promoting sustainable development.