● Download Report (PDF)

● Download Overview: English | عربي | Español | Français

● Visit Executive Summary Visualization

● Download Report (PDF)

● Download Overview: English | عربي | Español | Français

● Visit Executive Summary Visualization

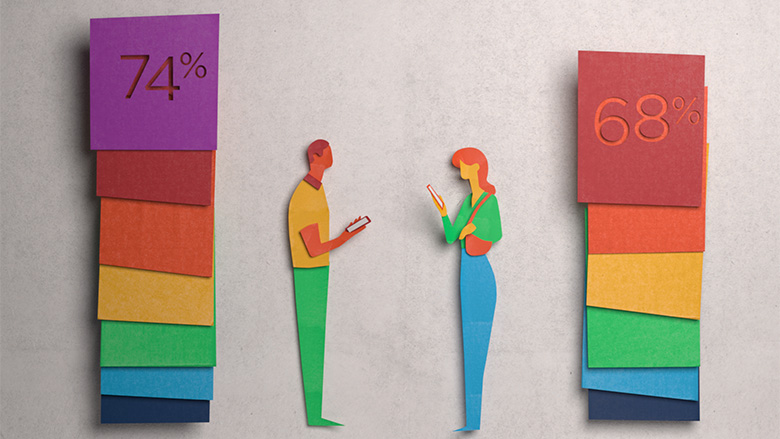

From 2017 to 2021, the average rate of account ownership in developing economies increased by 8 percentage points, from 63 percent to 71 percent. In Sub-Saharan Africa, this was largely due to the adoption of mobile money. The gender gap in account ownership across developing economies also fell to 6 percentage points from 9 percentage points, where it had hovered for many years. Despite this progress, millions of people worldwide remain unbanked. A lack of money, distance to the nearest financial institution, and a lack of documentation are consistently cited by unbanked adults among the primary reasons why they do not have an account. Global efforts for inclusive access to identification and mobile phones could be used to increase account ownership for hard-to-reach populations.

Chapter 1 Interactive Executive Summary | Chapter 1 (.pdf) | Chapter Figures (.jpg) | Chapter Data (.xls)

Chapter 2 Interactive Executive Summary | Chapter 2 (.pdf) | Chapter Figures (.jpg) | Chapter Data (.xls)

In addition to the findings on resilience, the Global Findex 2021 also captured data on the degree of financial stress people feel about common expenses. Unsurprisingly, poor adults and women in developing countries are more likely to experience financial stress and to report that they would need help using financial services. This points to opportunities to encourage more effective use of resilience-enabling services such as savings, and to ensure that consumer protection policies account for the low level of financial literacy in unbanked and underbanked populations.

Chapter 3 Interactive Executive Summary | Chapter 3 (.pdf) | Chapter Figures (.jpg) | Chapter Data (.xls)