The latest MENA Economic Monitor Report - Spring 2016, expects Morocco’s growth to slow down to 1.7% in 2016.

Assuming the full implementation of a comprehensive reform agenda following the autumn 2016 parliamentary elections, economic growth could accelerate and sustainably exceed 3.5% over the medium term.

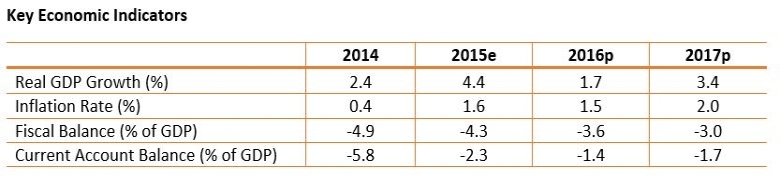

Economic activity rebounded in 2015 after a mixed economic performance in 2014. Supported by a strong agricultural season, economic growth accelerated from 2.4 % in 2014 to 4.4 % in 2015. However, growth outside agriculture was sluggish at below 2 %; the good performance of the “new” industries (automobile, aeronautics, and electronics) could not compensate for the decline in traditional sectors (such as textile and clothing) and tourism. Inflation has been under 2 %, reflecting a prudent monetary policy and the fall in international commodity prices. Total unemployment declined to 9.7 %. Yet, the unemployment rates among the urban young and educated remained disproportionally high at around 40 % and 20 %, respectively. The fiscal deficit decreased from 7.2 % of GDP in 2012 to 4.3 % in 2015 as a result of the authorities’ efforts to solidify the tax base and sharply reduce spending on energy subsidies. The central government debt stabilized at around 64 % of GDP in 2015. The current account deficit was also reduced from 9.2 % of GDP in 2012 to 2.3 % in 2015. The current account was supported by the good export performance of Morocco’s new industries, the crash of international oil prices, and an increase in workers’ remittances by 3 %. Tourist receipts have been adversely impacted by the current regional security situation and slumped by 1.3 % in 2015. The capital account was also strengthened by steady FDI inflows, access to international bond markets, and the continued financial support from development partners. International reserves increased by almost 13 % at end-2015 to reach $22.7 billion or the equivalent of 6.9 months of imports.

In 2016, economic growth is projected to decelerate to 1.7 %, under the assumption of a below average cereal output and a limited rise of nonagricultural GDP. The economy has been hit hard by a drought in the fall of 2015, which compromised the 2016 cereal production. The authorities’ emergency plan to safeguard livestock, protect plant resources and support rural income should however help contain the contraction of the agriculture GDP below 10 % in 2016. Non-agricultural GDP growth is expected to remain in the neighborhood of 2.5 % in the absence of more decisive structural reforms. According to the 2016 Budget law, the fiscal deficit is expected to decline further to 3.6 % of GDP in line with the government’s commitment to bring down the deficit to 3 % by 2017. With low oil prices, the current account deficit is projected to decrease further to 1.4 % of GDP in 2016.

The economic prospects over the medium-term hinge on the pursuit of sound macroeconomic policies and an acceleration of structural reforms. The emergence of new growth drivers in higher value-added export industries and the expansion of Moroccan companies in Western Africa are potentially creating the conditions for Morocco to become a hub for trade and investment between Europe and Africa and boost its position in global value chains. Assuming the full implementation of a comprehensive reform agenda following the autumn 2016 parliamentary elections, economic growth could accelerate and sustainably exceed 3.5 % over the medium term. Key challenges include structural orientation toward non-tradable activities; a volatile, weakly productive agriculture; and the need to increase productivity and competitiveness through comprehensive reforms of empowering market institutions (competition rules, labor code, and trade and investment regimes), strengthening the rule of law and the overall governance of public administration and services, boosting human capital, especially primary and secondary education.