Judgement

You have arrived at Station 8. In this station, you will learn how to apply judgement on top of the mechanical risk signals.

|

|

|

|

There may be information about your country that should inform the final risk rating, but is not reflected in the macroeconomic framework. Users are able to incorporate such information by combining the signals from the model on the risk

of debt distress with judgement. The application of judgement needs to be in line with the guidance as outlined below, and is not meant to be an open-ended exercise to change the mechanical rating.

Why is judgement needed?

The mechanical ratings are a first and core step in a DSA rating. However, the model cannot capture all country-specific factors relevant to debt sustainability analysis. The use of judgement is meant to assess ambiguities in the model with reference to material information that the model cannot take into account, such as:

- Short and marginal breaches;

- Country-specific vulnerabilities such as domestic debt, or market and external private debt; and

- Availability of liquid financial assets.

Short-Lived (1 year) Breaches

In the mechanical rating calculation for each of the debt indicators, short-lived (1-year, single) breaches are automatically disregarded under the baseline and/or most extreme stress tests.

However, they may be brought back in via judgement. For example, a large breach of a debt-service indicator in the near future is worrisome if mitigation factors, such as liquid assets, are not available to meet the payment.

Marginal and Temporary (more than 1 year) Breaches

These breaches can be disregarded taking into account mitigating factors.

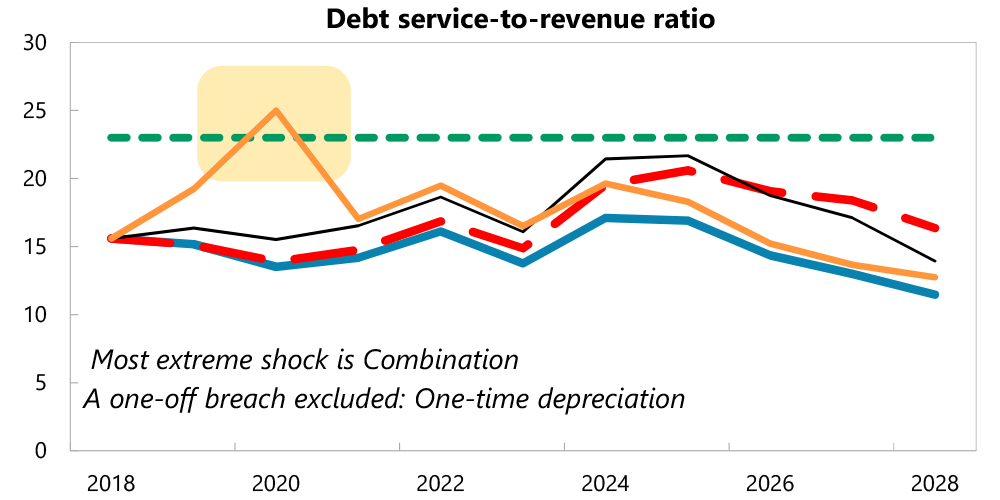

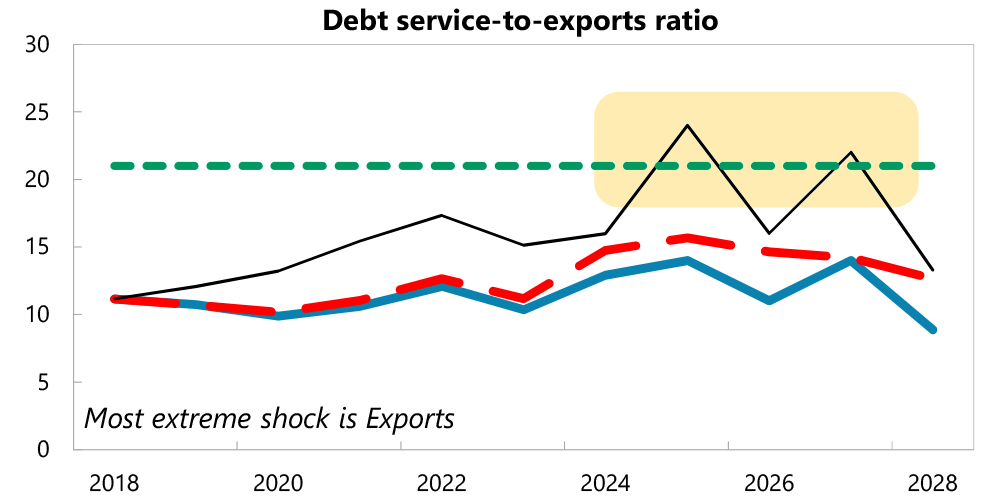

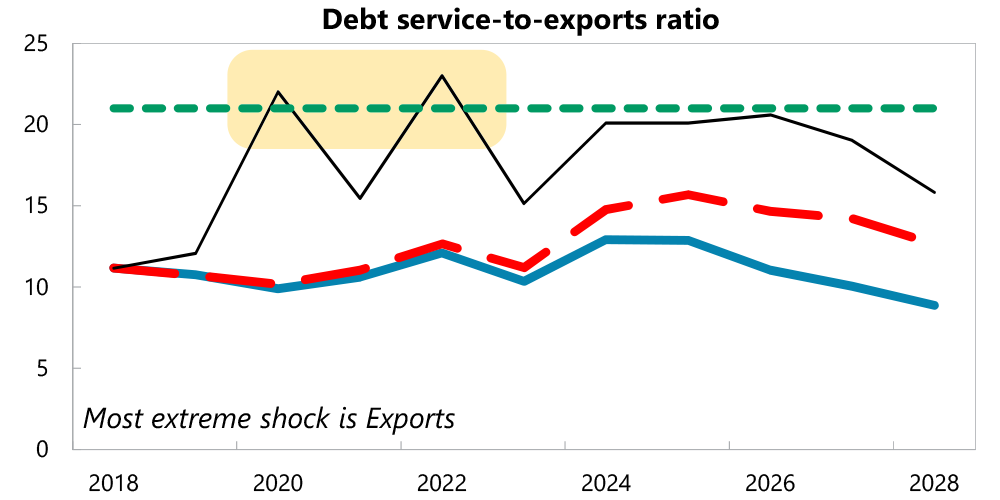

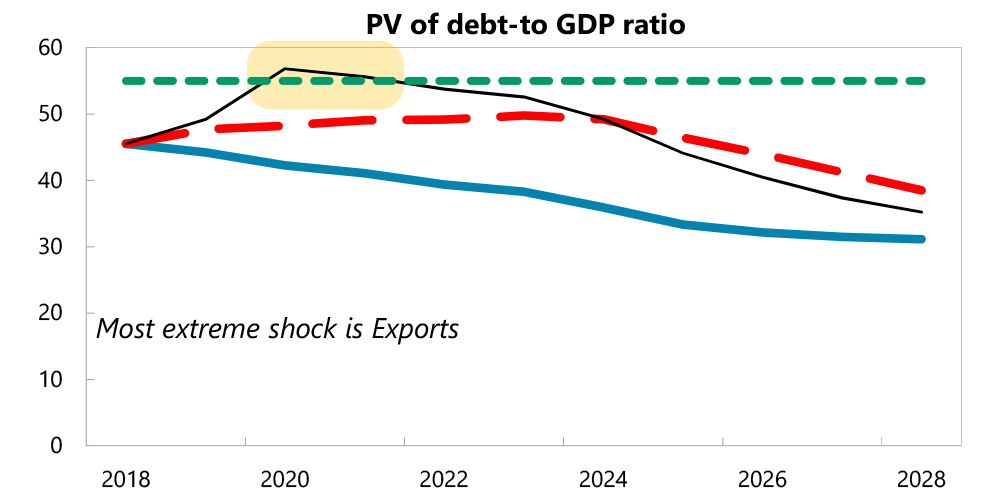

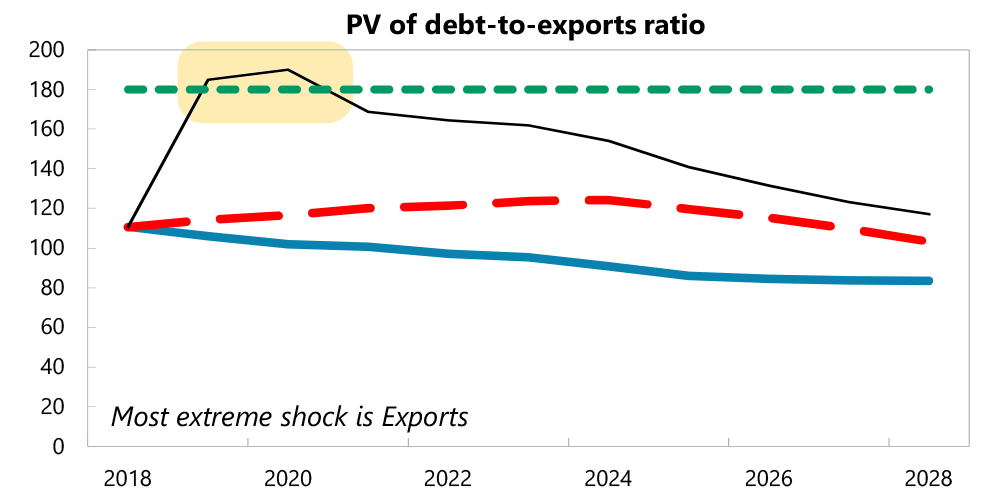

The timing of the breaches may be taken into account with breaches in the distant future (left chart directly below) being less worrisome than breaches in the near future (right chart directly below).

The breadth of the breach and breaches of multiple indicators should also be considered. The example below shows breaches in both a stock indicator (PV of debt-to-GDP) and flow indicator (Debt service-to-exports).

Additionally, take into account the dynamics of the breach. Sharp prior increases in indicator signals are of greater concern.

Considerations

Considerations

Domestic Debt and Market Financing Vulnerabilities

- More generally, a high total public debt service may crowd out other spending priorities, and may compromise other obligations. Since this may create a risk for the government’s willingness and ability to service its debt, it needs to be considered.

- If the DSA is conducted on a currency basis, but there are some non-resident debt exposures and this information suggests significant vulnerabilities, concerns about external risks may need to be revisited.

- When the market financing module signals a high risk, users should consider whether or not it should affect the final risk assessment.

External Private Debt

- In cases of a rapid accumulation of private external debt, does the private sector have enough liquid and readily available assets to mitigate the resulting risks?

- Large net open positions in the banking sector are red flags.

Availability of Liquid Financial Assets

- Readily available assets may be considered a mitigating factor if they are sufficiently liquid (e.g. foreign exchange deposits and amounts in sinking funds generally would qualify).

- Local currency denominated assets may also qualify, considering the minimum needed level of deposits, ability to withdraw deposits from domestic financial institutions without creating systemic stress, and whether they can be exchanged without impacting the exchange rate.

- Illiquid assets, such as equity shares in state-owned companies and untapped natural resources, cannot directly mitigate debt risks and generally should not be considered as a mitigating factor.

- Assets held at sovereign wealth funds (or stabilization funds) and through other extra-budgetary funds can be considered. However, it is important to consider the constraints on using these assets, when they cannot be legally withdrawn to repay or service debt, they should be excluded.

Long-Term Considerations

- Large, protracted, and highly probable breaches in years 11-20 may change the risk rating. For example, high debt services, climate change, population aging, and resource exhaustion could have an effect.

Other Country-Specific Considerations

- Consider gains from greater balance of payments protection from reserve pooling arrangements (currency union). However, their credibility and availability in the face of liquidity constraints should be assessed.

- Take into account the availability of insurance type arrangements. For example, hurricane clauses in bonds and GDP-linked bonds.

- Consider the true degree of confidence in the macro baseline, particularly in customized scenarios. For example, a contagion risk from trade partners or delays in investment projects may affect this level of confidence in the baseline.

Takeaways for Station 8

Takeaways for Station 8

- The mechanical risk rating for the PPG external and total public debt constitute the first and core step in doing a DSA.

- Judgement is used to account for ambiguities not captured in the DSF’s underlying model.

- The use of judgement is not an open-ended exercise to change the mechanical risk rating.

- Vulnerability signals from other factors, such as domestic debt and market financing module, should be brought in through judgement.

Travel to Station 9 for the next part of your journey

|

|

|

|

|

|

|

|

|

|