Data Inputs for the LIC DSF Template

You have arrived at Station 2. Here you will be guided through the numerous data inputs required by the LIC DSF Excel template and will learn how to do the following:

|

|

|

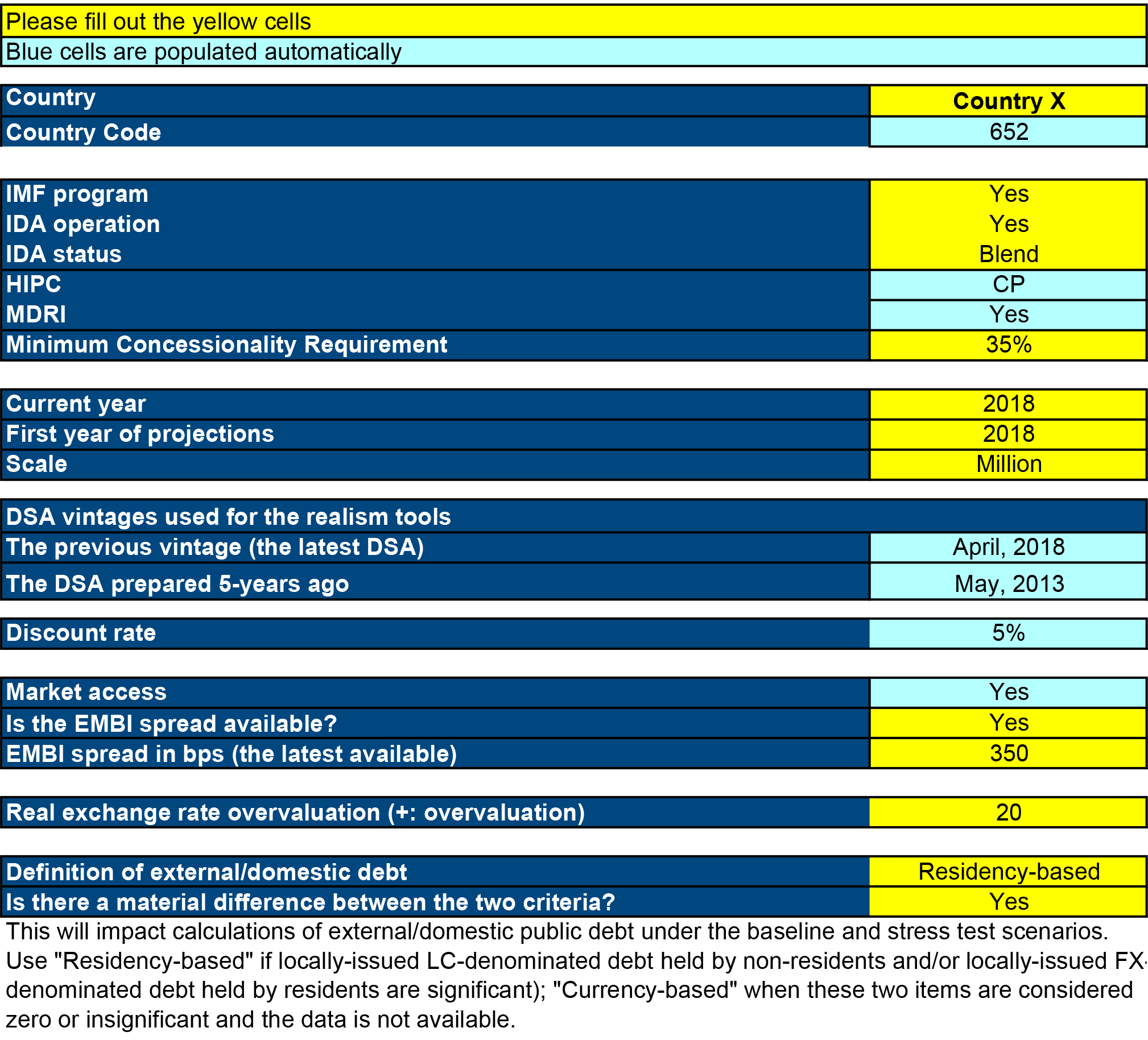

As you can see, cells in the LIC DSF template are color-coded. All the data inputs required for the template to function properly are shaded yellow and blue cells are populated automatically.

To begin working on the template, choose your country and enter some basic information in the “Input 1 – Basic” sheet as illustrated below. Please note the “IDA Status” field in the template, which has implications for external financing. The terms are shown in Input 4 of the template.

In the template, this table is in the “Input 1 – Basic” sheet.

Coverage

In this first substation, we will discuss how to determine public sector debt coverage.

Determine Debt Coverage

Comprehensive public debt coverage is vital to accurately assess the risk of debt distress. A narrow definition of public debt could result in unexpected risks from sources outside the defined public sector perimeter.

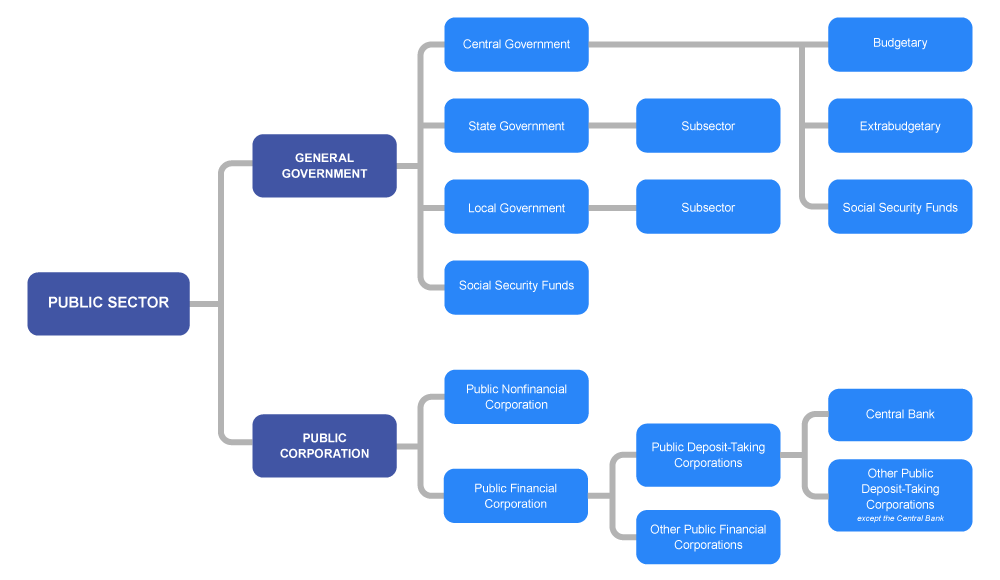

Public sector debt, in its broadest definition, is comprised of debt from several different sub-sectors. The LIC DSF covers both external and domestic debt in two areas:

- Public sector: defined as central, state, and local governments; social security funds and extra budgetary funds; the central bank; and public enterprises

- Private sector: defined as debt guaranteed by the public sector

Public financial corporations are generally excluded, but the LIC DSF toolkit offers options to consider them as contingent liabilities.

Considerations

Considerations

-

Central bank debt: there should be no netting out (the only exception to this, is if for some reason, the central bank is consolidated with the central government).

-

State-owned enterprise (SOE) debt: all available information on the debt of fiscally-important non-financial public enterprises should be included in the DSA (unless an SOE is to be excluded).

Contingent Liability

The scope of debt coverage determines the definition of a contingent liability. A contingent liability stress test will apply to all countries.

A narrower coverage of public debt in the LIC DSF will automatically trigger an additional contingent liability stress test. This test will assess risks from other omitted sectors that may affect the risk rating. The magnitude of this contingent liability shock can and should be customized in the template reflecting your country-specific public debt coverage.

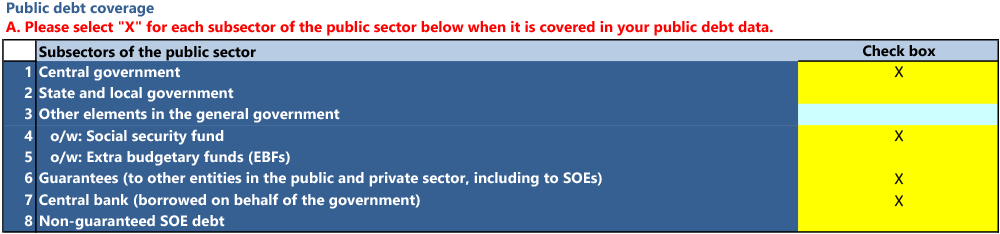

To define debt coverage, specify the subsectors in the template.

In the template, this table is in the “Input 2 – Debt Coverage" sheet.

Based on the debt coverage identified, you are encouraged to customize the magnitude—if your country-specific information is available—by entering values in the yellow-shaded cells. Doing so will override the default settings in blue-shaded cells.

In the template, this table is in the “Input 2 – Debt Coverage" sheet.

Key Messages

Key Messages

- Full coverage of the public sector is crucial for an accurate assessment.

- Narrower coverage would result in a larger contingent liability stress test, (see Station 5 for more details).

Macro Data

In this substation, we will focus on macroeconomic inputs and fiscal projections.

The DSA must be informed by an accurate macroeconomic framework. Such a framework is referred to as the baseline scenario, and it represents the most likely scenario given current data.

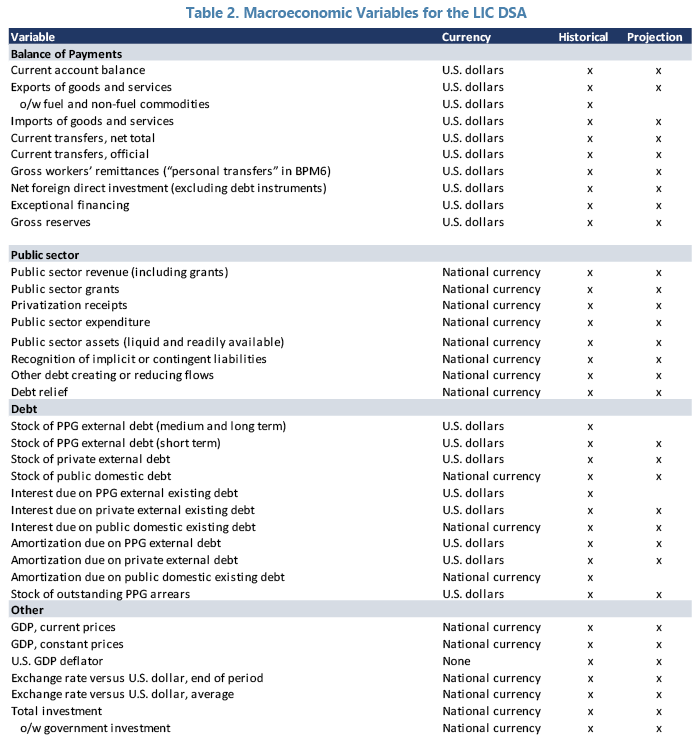

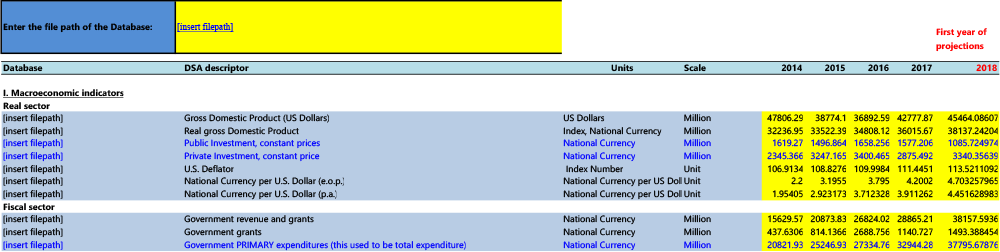

You are required to input both historical (previous 10 years) and projected (next 20 years beyond the current year) values for the following key macroeconomic and fiscal indicators, grouped by real, fiscal, and external sectors:

- Data on the real sector, such as nominal GDP, GDP deflator, and exchange rates;

- Data related to public accounts, such as revenue, primary expenditure (that is, expenditure excluding interest payments), and grants; and

- Data related to external accounts, such as exports, imports, and current transfers.

Exercise: The chart below illustrates historical and projected data with stylized numbers. The sliders can be used to zoom-in or out using the slider below.

See the full list of variables required to produce a DSA. As explained below, the detailed list is found in the “Input 3” sheet of the template.

DSAs are only as good as their underlying assumptions! Forecasting over a long-period of time, such as the 20-year projection horizon, has many challenges. The key challenge to avoid is being overly optimistic about the macroeconomic

and fiscal assumptions.

The 20-year forecast horizon can be broken up into medium-term and longer-term projections, with the following considerations.

The baseline should be based on policies that are already in place, and those announced that are likely to be implemented. In the case of a country under an IMF/WB program, these policies would correspond to the adjustment program scenario that has been agreed to with the IMF/WB.

Typically, over the medium-term horizon, all gaps are assumed to close including the output gap and the real effective exchange rate (REER) gap.

Long-term projections should avoid excessive optimism.

- Projections on fiscal policy: Permanent improvements need to be justified. Are they backed by the introduction of a fiscal rule or other structural changes to policies or institutions?

- Projections on monetary policy: Permanent improvements to inflation dynamics need to be justified. Are they derived from the introduction of a rule or other structural changes to policies or institutions?

- Projections on external sector developments: High growth rates and increases in productivity in the tradable sector are usually expected to lead to higher wage growth and an appreciation of the equilibrium real exchange rate over time.

- As income levels rise, the average growth rate tends to fall. This is referred to as the “catching-up” effect.

- Natural disasters or persistent domestic instability lower long-term growth prospects. The average annual expected impact can be captured in the baseline.

- The discovery of natural resources does not always result in production.

- Achieving development goals usually requires additional spending.

- Long-term projections should incorporate trends in the equilibrium real exchange rate.

- Other relevant country-specific factors should be considered.

Key Messages

- DSAs are only as good as the realistic projections underlying them.

- The baseline scenario requires 10 years of historical data and 20 years of coherent and realistic, rather than optimistic, projections for key macroeconomic and fiscal variables.

Debt Data

This section will help you understand how to input comprehensive information on the current stock of debt.

The DSA requires comprehensive information on debt/liabilities.

Government debt, which generally requires payment of interest and principal, is the most common form of government liabilities.

| Government Liability | Limited cases where debt should be excluded from the DSA | Liquid Financial Assets |

|---|---|---|

| Debt securities, loans, other accounts payable | Disputed claims—the amount disputed should be treated as a contingent liability | These mitigate, but do not eliminate risks for debt sustainability (Note: These are considered later at the level of judgement.) |

| Verified and recognized obligations that are not debt arising from a financial claim (for example, arbitration awards) | Claims that are eligible for debt relief that have already been agreed upon |

A DSA should be conducted on the basis of gross debt capturing the face value of debt and including appropriate consolidations.

Public debt should be included in the DSA based on actual and best estimates of disbursement from undisbursed and expected loans.

The DSA should ideally define external debt based on the residency of the creditor, given the external DSA is built on a balance of payments, which is prepared on a residency basis.

For LICs, external debt is sometimes defined on a currency basis. This is a reasonable approach if non-resident holdings and/or foreign currency-denominated locally-issued debt is insignificant.

| Definition of external/domestic debt | Currency-based | Residency-based | ||

|---|---|---|---|---|

| Locally-issued debt | held by residents | LC | Domestic | Domestic |

| FX | External | |||

| held by non-residents | LC | Domestic | External | |

| FX | External | |||

| Externally-issued debt | held by non-residents | FX | External |

The "Input 3" sheet in the template is setup so it can be linked to a compatible database.

In the template, this table is in the “Input 3” sheet.

Key Messages

- Existing stock of debt should be entered on a gross basis.

- Existing stock of debt should reflect the debt outstanding and disbursed, not commitments.

Financing

In this final substation, we will discuss how to make financing assumptions about future debt, as well as how this debt may be rolled over and refinanced.

Both public and external debt dynamics for the projected horizon derive from three elements: the underlying macroeconomic projections of key debt drivers; the profile of the existing debt stock amortizations and interest repayments; and the projected financing assumptions that drive amortizations and interest repayments from the newly contracted debt. Together, these elements cover the planned gross financing needs (GFN).

Template Inputs

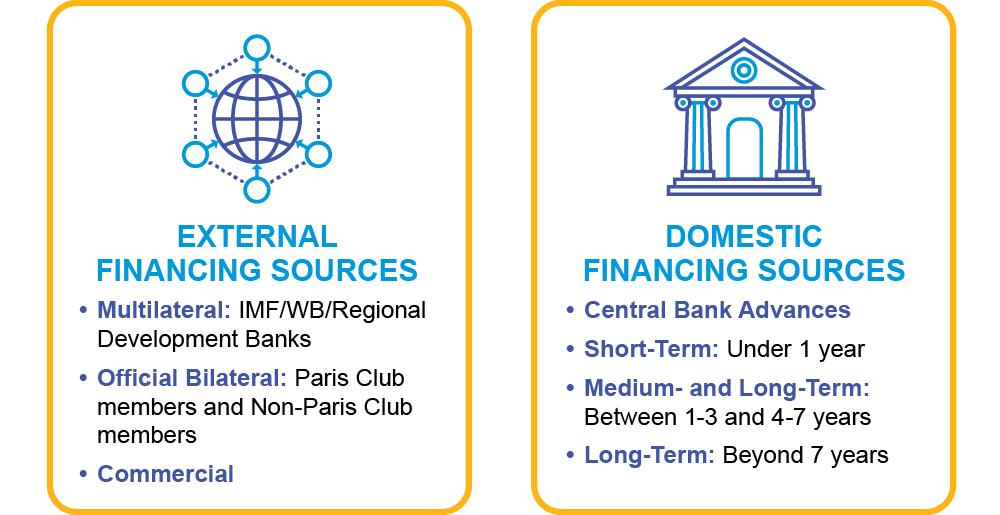

Financing assumptions to cover the planned GFN should take into account both shifts in borrowing terms and the overall financing mix of short-term (ST) and medium- and long-term (MLT) debt over time.

Amounts from each source, including internal and external, domestic, and financial terms such as interest rates, grace periods, and maturities, should follow the published medium-term debt management strategy (MTDS) document and/or donors' financing plans for grants, concessional, and non-concessional borrowing.

There will likely be a shift in available external financing from grants to concessional loans for the poorest and most vulnerable countries, and from concessional loans to loans on commercial and market terms for other countries.

This outlook should be considered with regard to potential new main creditors, availability of donor grants, development trends, and Eurobond issuances.

Similarly, domestic debt is expected to shift from central bank and short-term sources to borrowing via a broader range of competitively issued market-based securities, such as bonds.

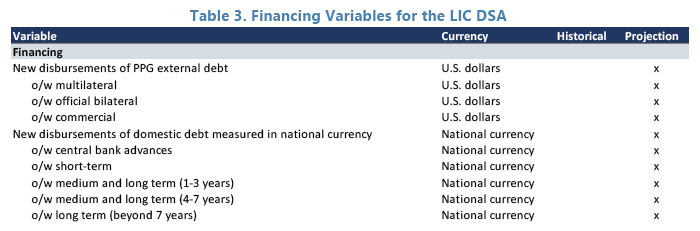

The following variables require assumptions to ensure the planned GFN are covered for the entire projection horizon:

In the template, assumptions on projected debt and gross financing needs are captured in three input sheets: Input 3, Input 4, and Input 5. Enter the values of known (confirmed) disbursements expected in the near-term and projected disbursement for outer years in Input 3. Enter external borrowing assumptions in Input 4 and assumptions on terms and disbursements of domestic debt in Input 5.

Amounts of new disbursements are entered in Input 3, under the two sub-sections:

- New medium- and long-term debt external disbursements

- Locally-issued debt disbursements

The terms of new PPG external debt disbursements (financing) by creditor groups are entered in Input 4. These terms include the interest rate, grace period, and loan maturity.

The interest rates are specified in nominal terms.

The lending terms or creditors are assumed to be identical to those used for existing (historical) debt service and new external borrowing.

While annual disbursement schedules are typically imported from Input 3, you can freely design/modify the external financing strategy in this worksheet using the light-yellow shaded cells.

The assumed total external borrowing (aggregate external debt) should be made consistent with external financing gaps in the Balance of Payments (BoP).

Considerations for Input 4:

Multilateral debt: This creditor group includes the IMF, World Bank, and other regional development banks (such as ADB and AfDB). While IDA’s lending terms can be selected from the pull-down menu, you will need to make sure that selected lending terms are available to your country, consistent with its IDA classification, and that automatically-populated information is up to date as IDA quarterly reviews its lending terms. IDA’s repayment schedule is sometimes not standard equal repayment and has a tail-heavy repayment structure. Though the template automatically selects the repayment schedule corresponding to the pull-down menu, you should make sure the repayment schedule is up to date.

Commercial debt: This category covers lending where new loans can have vastly different terms should market conditions worsen. Borrowing from private creditors normally falls under this category while official lenders tend not to change their lending terms dramatically when market conditions worsen. The latter should be treated under multilateral or bilateral creditors even when their lending terms are non-concessional.

Terms and disbursements of locally-issued debt are entered in Input 5. This input sheet allows you to conduct a detailed analysis on domestic debt dynamics by explicitly estimating public Gross Financing Needs (GFNs) to be financed with domestic debt.

Often, (net) domestic financing may be treated as a residual financing item in the fiscal analysis without thoroughly taking into account different domestic financing instruments or the availability of such domestic financing. This could lead to implausible domestic debt dynamics.

The template allows you to identify public GFNs and think about how to meet them using available domestic and external financing. Gross flows related to external financing (disbursements and debt service) are then linked to the Ext_Debt_Data sheet, and residual financing needs are supposed to be filled by domestic financing.

Note that changes in liquid assets are also an important factor that should turn negative in cases of over-financing. In addition, purchases from the IMF are typically used to build up foreign reserves at a central bank (BoP support) and do not finance a budget (budget support). You should therefore adjust public GFNs to take into account scheduled purchases and repurchases, which are not supposed to affect domestic borrowing. Those used for budget support do not have to be adjusted.

Considerations for Input 5:

Domestic instruments should meet identified residual public GFNs after accounting for external financing and other items, such as changes in liquid assets and purchases or repurchases from the IMF. They should also reflect the depth of the domestic financial market and the availability of domestic financing. Further, the residual between public GFNs identified by the template and the sum of new external and domestic disbursements are assumed to be filled by short-term local-currency T-bills.

In general, the residuals should be minimized to the maximum extent possible to serve as a check against baseline financing assumptions.

Please make sure that there is no over-financing; that is, the residuals (which are assumed to be filled by T-bills) are small and positive. Overfinancing will be signaled by “negative” residual financing, which is too large in the absolute terms to be absorbed by originally-assumed T-bills. If, for example, you want to assume domestic financing beyond public GFNs to accumulate liquid assets for cash management purposes, it should be reflected in changes in liquid assets.

You may import yearly disbursement schedules from a macro framework or design/modify in the template. You can import a domestic financing schedule through Input 3 by selecting “0” rather than “1” in the Domestic Financing Strategy section, whereas with “1” you can design a domestic financing strategy in this worksheet usually when a sufficiently detailed domestic financing strategy is not available in the macro framework. In the case of the latter, you can:

1) directly put the volume of disbursements for each of projection years in light-yellow; or

2) set percentage shares for different domestic instruments for every 5-year period during the 20-year projection period.

Under option (2), this structure can be easily comparable to the country’s Medium-Term Debt Management Strategy (MTDS), if any.

Domestic residual financing to close any remaining gap is assumed to be filled by T-bills after allocating volumes of other domestic instruments based on assumed percentage shares highlighted in yellow. Please note that locally-issued debt held by non-residents is not shown when a currency-basis is chosen as holders of debt are not relevant on a currency basis.

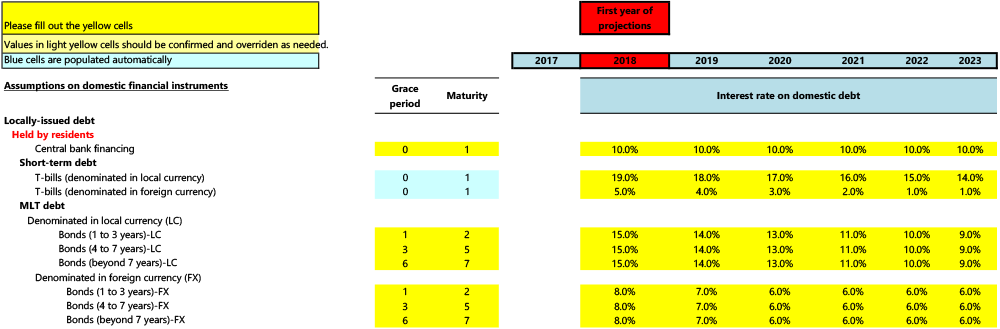

Exercise: What are the terms of locally-issued debt in your country?

Pick the maturities of long-term debt instruments and change the interest rates over the two projections years so see the impact on the average weighted interest rate of the debt portfolio (shown at the bottom of the table). Note that the shares of each instrument (last column) are fixed.

The table for baseline locally-issued financing assumptions is in the "Input 5 - Local-Debt Financing" sheet of the template.

In the template, this table is in the “Input 5 - Local-Debt Financing” sheet.

The LIC DSF template automatically runs a number of stress scenarios for each of the two built-in DSAs: the External Debt DSA and the Public Debt DSA. For each, the financing assumptions under the respective External DSA and Public DSA Stress Scenarios should be entered in Input 7. The customization assumptions for the Stress Scenarios are entered in Input 6 of the template and will be discussed in station 5.

The LIC DSF assumes that additional financing needs (residual financing) are filled using projected average lending terms assumed under the baseline (specified in Input 4 and Input 5). The terms of the residual financing are found in Input 7.

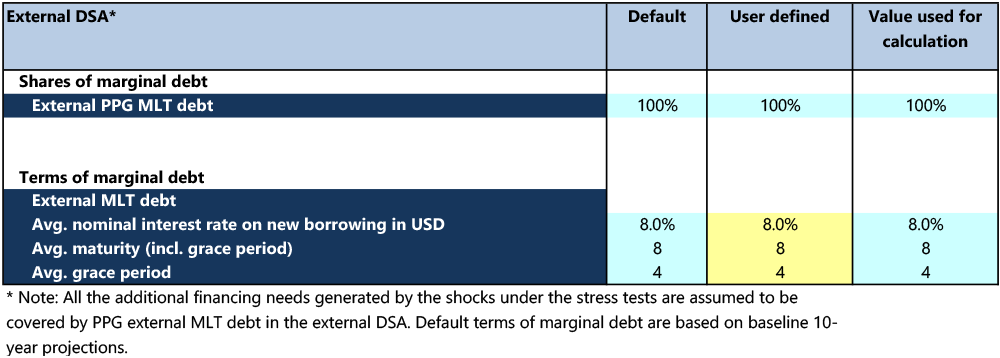

External DSA: For the External DSA, additional financing needs are assumed to be fully financed by medium- and long-term (MLT) external debt. While assumptions on the terms for such additional financing are pre-populated based on the baseline financing assumptions (a weighted average of external debt instruments), you can modify the default settings if necessary in the yellow-shaded cells. The terms used for an analysis are also shown in Output 2-1 – Stress_Charts_Ex. Interest rates are specified in nominal terms for FX borrowing and are assumed to be in U.S. dollars.

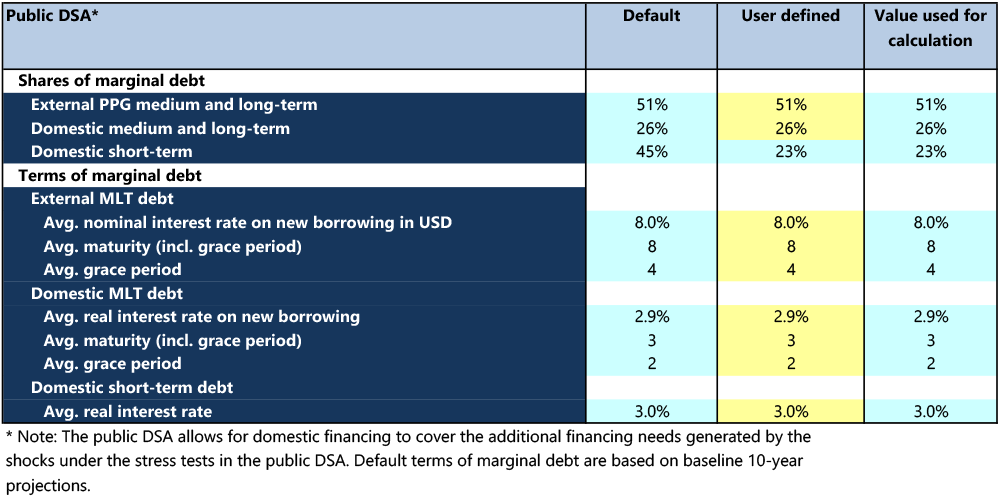

Public DSA: Assumptions on the terms used for filling additional financing needs under stress tests are also automatically populated based on the baseline assumptions, along with the corresponding lending terms. You can, however, manually modify such assumptions for residual financing in the yellow-shaded cells if warranted, and such changes should be fully explained in the DSA write-up. Terms for domestic borrowing should be in real terms as nominal interest rates are defined as the real interest rate, plus an annual inflation rate (GDP deflator). These assumptions are shown in output sheet Output 2-2 – Stress_Charts_Pub. External financing terms should be the same as those for the external DSA.

In the template, this table is in the “Input 7 - Residual Financing” sheet.

In the template, this table is in the “Input 7 - Residual Financing” sheet.

Takeaways for Station 2

Takeaways for Station 2

- The LIC DSF applies to Public and Publicly Guaranteed (PPG) debt. It requires as broad of a coverage of the public sector and its explicit guarantees as possible.

- The LIC DSF produces two full Debt Sustainability Analyses (DSAs): one for external PPG debt and one for the overall public debt.

- To produce these DSAs, the template requires multiple data inputs, including at least 10 years of historical data plus 20 years of projections. The projected macroeconomic, fiscal, and external time series should form a consistent and coherent baseline scenario.

- The template also requires data on external and public debt including past stocks, as well as the repayments of the principal and interest on the existing (outstanding) portfolio throughout the entire projection period. This data is classified by creditor and by maturity.

- Finally, the template requires users to make coherent assumptions about external and domestic financing—the new borrowing necessary to cover the Gross Financing Needs (GFN) for all the projection periods. This financing can be external or domestic.

- Under the baseline scenario, the financing assumptions in the template are made in several Input sheets distinguishing between the disbursements amount, external financing terms, and domestic financing instruments. A separate Input sheet is used for the assumptions on financing under the stress scenarios.

Travel to Station 3 for the next part of your journey

|

|

|

|

|

|

|

|

|

|