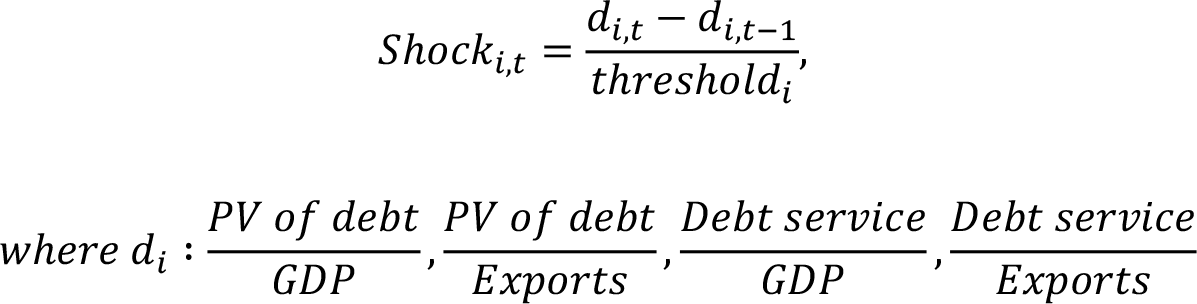

Granularity

You have arrived at Station 10, your final stop in this interactive guide. Here you will learn how to further differentiate between countries that fall under the moderate risk of debt distress category and assess debt sustainability for countries under the high risk of debt distress or in debt distress categories.

|

|

|

|

Once the risk rating is determined, analysis that provides more differentiation in characterizing the extent of vulnerabilities is assessed.

Countries in the moderate risk category are numerous and display a great diversity of debt vulnerabilities. To provide more granularity into the assessment of risks facing those countries, the DSA offers a further evaluation of a “space to absorb shock” without being downgraded into a high risk category. These outputs were shown in station 6, as they are key outputs for countries in moderate risk of debt distress.

For countries in high risk of debt distress or in debt distress, their debt sustainability should be examined.

Moderate Risk Tool

Using DSAs produced since the LIC DSF's inception, staff calculated the distribution of observed shocks that led to a rating downgrade to a high risk of debt distress. Such shocks are calculated as the observed change in debt burden indicators, or the peak in debt after and before the shock leading to a downgrade, in percentage of the respective threshold.

Potential shocks are calibrated from their observed distributions.

If you would like to find more information check out the DSF Policy Paper

Moderate Risk Tool

The moderate risk tool helps countries better understand the subtleties of a moderate risk rating.

- This tool illuminates the nature and diversity of debt vulnerabilities in moderate risk countries, with particular attention paid to any buffers these countries may have to absorb shocks.

- This tool can help countries understand the diverse risk characteristics and debt vulnerabilities associated with a moderate risk rating in the external DSA.

- This tool is calibrated based on the distribution of shocks that result in a downgrade from a moderate to high risk of debt distress.

- Assessment of the “space to absorb” shocks should shed light on the robustness of the debt position and be discussed in the DSA write-up for countries rated with a moderate risk of debt distress.

Application of the Fund’s Debt Limits Policy and the World Bank’s Non-Concessional Borrowing Policy will not be affected by the above characterization.

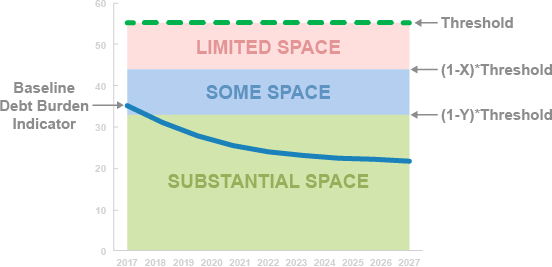

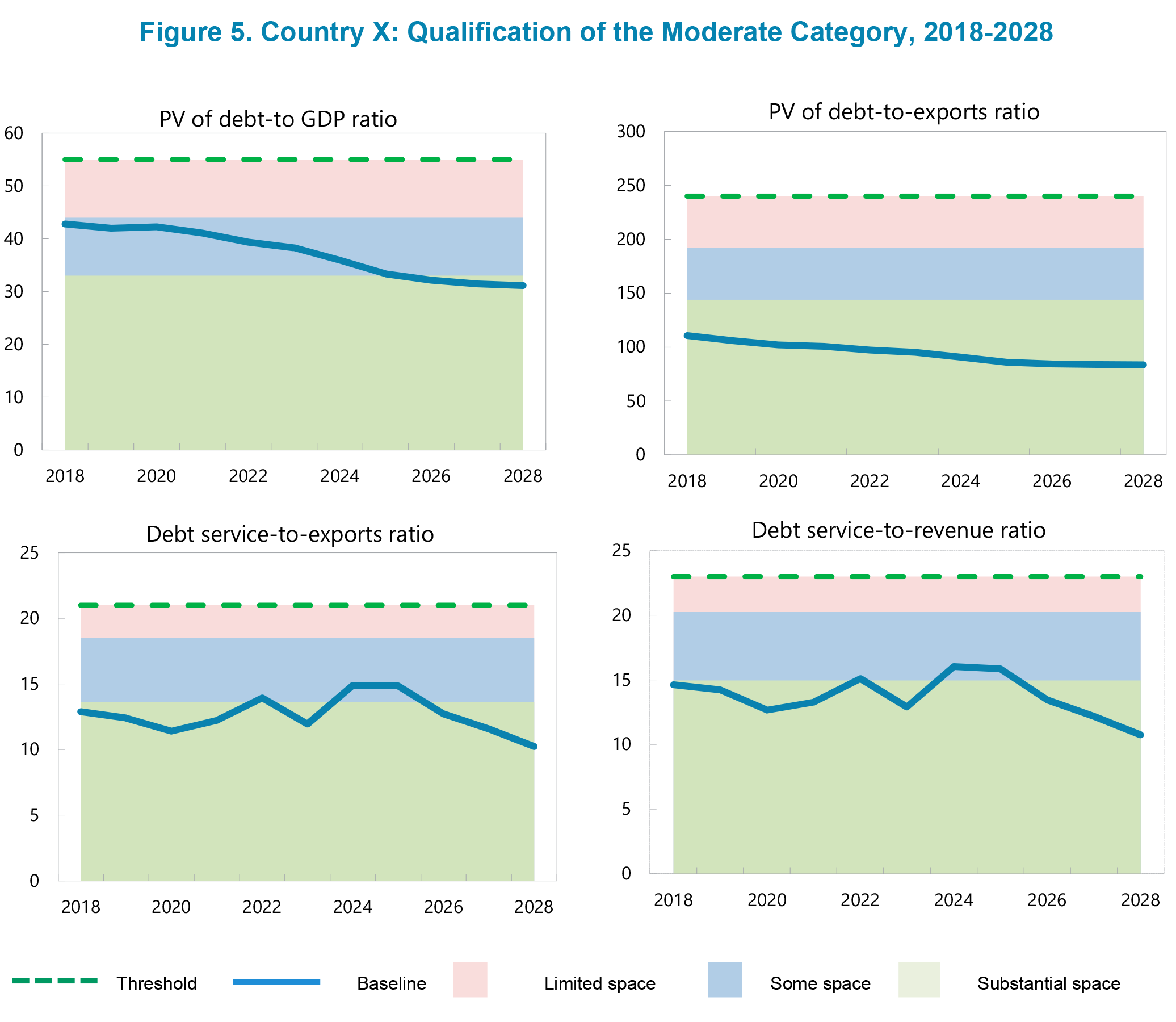

This tool also provides three classifications based on a historical analysis of shocks that moved countries to a high risk of debt distress.

For the PV of debt/GDP and PV debt/exports thresholds, X is 20 percent and Y is 40 percent. For debt service/exports and debt service/revenue thresholds, X is 12 percent and Y is 35 percent.

This tool is for countries that are moderate based on the final risk rating in the external DSA. One-off breaches are excluded for the purposes of these classifications.

In the stylized example directly below, it would be classified as having some space to absorb shocks. If everything evolves as projected, the country will eventually have substantial space to absorb shocks.

Output 5-1

In the template, this table is in the “Output 5-1” sheet.

Assessing Sustainability

The rating In Debt Distress is not only applied when there is a distress event such as a restructuring or arrears, but also during “significant or sustained breaches of thresholds.”

Sustainability is fundamentally a matter for judgement and general considerations in assessing sustainability should be applied based on:

- Whether debt burden indicators are at high levels and continuously rising.

- Whether breaches under the baseline scenario are significant or sustained (beyond four to five years), cover both debt and debt service indicators, and only rebound after some time.

- When your country has a high risk of debt distress and underlying this are significant or sustained breaches, you need to judge whether debt is sustainable.

- Whether the projected debt path is one in which we have strong confidence. Wider confidence intervals imply a greater chance of a debt distress event, all else being equal.

However, as in the case of other risk ratings, an assessment that debt is unsustainable also must incorporate broader judgement.

In general, overall public debt and public external debt can be regarded as sustainable when there is a high likelihood that a country will be able to meet all its current and future financial obligations.

In practice, sustainability would imply that the debt level and debt service profile are such that the policies needed for debt stabilization under both the baseline and realistic shock scenarios are politically feasible and socially acceptable, and consistent with preserving growth at a satisfactory level while making adequate progress towards the authorities’ development goals.

Thus, other factors not captured in the model, like feasibility issues, debt structure and holders, and impact on development goals, also need to be accounted for.

Takeaways for Station 10

Takeaways for Station 10

- If a moderate risk rating is assigned, you should also make a more granular assessment of the risks within the moderate risk category. If a high risk or in distress rating is assigned, you should assess whether the breaches are significant and sustainable.

- A country may be judged to be in debt distress not only when there is a distress event (restructuring, arrears), but also during “significant or sustained breaches of thresholds".

This completes your journey!

|

|

|

|

|

|

|

|

|

|