The latest MENA Economic Monitor Report - Spring 2016, expects Palestine’s growth to remain unchanged at 3.3 % in 2016, although its economic outlook continues to be highly uncertain.

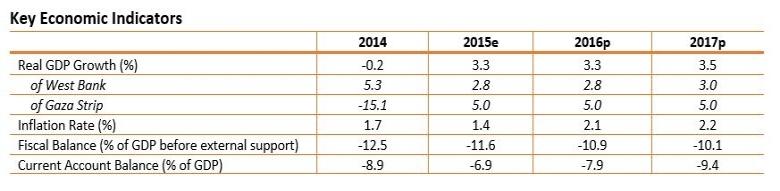

An economic recovery is underway following the 2014 recession caused by the Gaza war. The economy is estimated to have expanded by 3.3 % in 2015. Reconstruction efforts have provided a boost to the Gaza economy where real GDP growth is estimated to have reached 5 % in 2015, driven by strong growth in the construction sector as well as retail and wholesale trade. However, growth in the West Bank slowed in 2015 with real GDP expanding by 2.8 %, which is 2.5 %age points lower than in 2014. The slowdown is mainly attributed to a significant decline in foreign aid in addition to the Israeli decision to suspend the transfer of Palestinian taxes in early 2015, resulting in a severe liquidity squeeze. Unemployment continues to be stubbornly high at 26 %. In the West Bank, it amounted to 19 % by the end of 2015 while it was twice as high in Gaza. Unemployment is exceptionally high amongst Palestinian youth, particularly in Gaza where more than half of those aged between 15 and 29 are out of work. Inflation remains low and stable, at 1.4 % in 2015.

The Palestinian Authority's (PA) fiscal deficit (before grants) narrowed in 2015 to 11.7 % of GDP. Expenditure growth was high, exceeding 6 % (in nominal NIS terms), mainly driven by spending on transfers and goods and services. However, it was offset by strong revenue growth of 9 %. Aid in 2015 dropped by almost 30 % relative to the previous year and was less than needed to cover the deficit, leading to a U5$650 million financing gap. The PA resorted to accumulation of arrears and domestic borrowing to cover the gap.

The current account deficit (excluding official transfers) is estimated to have declined to 11.3 % of GDP in 2015 due to a narrowing of the trade deficit. Preliminary estimates indicate that the trade deficit reached 36.6 % of GDP in 2015, which is 3 %age points lower than its 2014 level. This was mainly driven by a decline in imports from Israel as growth slowed in the West Bank.

The economic outlook continues to be highly uncertain. Under a baseline scenario that assumes no change to the Israeli restrictions on trade, movement and access, growth is expected to remain unchanged in 2016 at 3.3 %. In the West Bank, growth is projected at 2.8 % assuming that the ongoing clashes do not escalate. Growth in Gaza is projected at 5 %, as reconstruction advances. If reconstruction continues at its current pace, Gaza's GDP will not rebound to its prewar levels until 2018. In the medium term, overall growth in the West Bank and Gaza is expected to hover around 3.5 %, leading to stagnant per capita incomes and rising unemployment.

Significant downside risks remain that could significantly worsen the economic outlook. First, the pace of reconstruction and recovery in Gaza has been slower than anticipated and despite some acceleration in recent months, additional setbacks are possible. Second, the outcome in the West Bank may be worse than expected if tensions continue to escalate. This environment may significantly weaken consumer and investor confidence, and hence, negatively impact economic activity. Finally, the failure to form a unified government for West Bank and Gaza has created two parallel regulatory frameworks: one in the West Bank and another one in Gaza. All this could potentially have a negative impact on the business climate