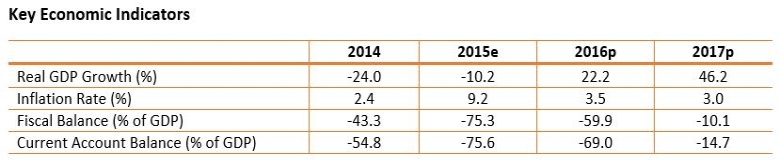

The latest MENA Economic Monitor Report - Spring 2016, expects Libya’s fiscal and current account deficits to continue in 2016, with the budget deficit at about 60 % of GDP and the current account deficit at 70 % of GDP. In the next few years, as oil production reaches full capacity, growth is projected to rebound at 46 % in 2017 and 15 % in 2018.

The political conflict has taken a severe toll on the economy, which has remained in recession for the third consecutive year in 2015. Political strife, weak security conditions, and blockaded oil infrastructures continue to constrain the supply side of the economy, which shrank by 10 % in 2015. Production of crude oil fell to the lowest level on record, to around 0.4 million barrels per day (bpd), which represents a quarter of potential. The non-hydrocarbon sectors remained weak due to disruptions in the supply chains of both domestic and foreign inputs, as well as lack of financing. Inflation accelerated to 9.2 % in 2015, mainly driven by a 13.7 % rise in food prices. Lack of funding to finance imports (especially subsidized food) generated shortages and an expansion of the black market. Prices of flour quintupled.

Protracted political standoff, coupled with lower international oil prices, have hit public finances hard. Budget revenues from the hydrocarbon sector have fallen to only a fifth of the level in the pre-revolution period, while spending has remained high. The share of the public wage bill in GDP is at a record of 59.7 %, mainly reflecting new hiring of civil servants. Meanwhile, investments have been insufficient for sustaining adequate public provision of health, education, electricity, water and sanitation services. However, savings have been realized on subsidies, which fell by 23.6 % thanks to tougher control of the supply chains of subsidized products and lower import prices. Overall, the budget deficit rose from 43 % of GDP in 2014 to 75 % of GDP in 2015. The deficit was mainly financed from the Government’s deposits at the Central Bank of Libya (CBL).

The balance of payments deteriorated further in 2015. Oil exports declined to 0.3 million bpd. Oil export revenues are estimated to have reached less than 15 % of their 2012 level. At the same time, consumption-driven imports remained high. The current account swung from balance in 2013 to a deficit estimated at 75.6 % of GDP in 2015. To finance these deficits, net foreign reserves are rapidly being depleted. They were halved from $107.6 billion in 2013 to an estimated $56.8 billion by end 2015. The official exchange rate of the Libyan Dinar (LYD) against the $ continued to weaken, depreciating further by more than 9 % in 2015. In the parallel market, the LYD depreciated by around 160 %, due to restrictions on foreign exchange transactions that were implemented by the CBL.

Improvement of the economic outlook depends crucially on the endorsement by the House of Representatives of the Government of National Accord (GNA) formed under the auspices of the UN. The economic and social outlook assumes that the GNA begins governing the country by restoring security and launching programs to rebuild the economic and social infrastructures. In this context, production of oil is projected to improve to around 1 million bpd by end 2016. On this basis, GDP is projected to increase by 22 %. However, the fiscal and current account deficits will continue in 2016, as revenues from oil will not be sufficient to cover the budget expenditures and consumption-driven imports. This should keep the budget deficit at about 60 % of GDP and the current account deficit at 70 % of GDP. As oil production reaches full capacity, growth is projected to rebound at 46 % in 2017 and 15 % in 2018, before stabilizing between 5 and 5.5 % thereafter. Both the fiscal and current account balances will significantly improve, with the budget running surpluses expectedly from 2018 onwards, while current account deficits will progressively decline to less than 0.5 % of GDP in 2019. Foreign reserves will average around $22 billion during 2017-2019, representing the equivalent of 8.2 months of imports.