The latest MENA Economic Monitor Report - Spring 2016, expects Iraq’s economy to recover from a low base, growing at 7.2 % in 2016 and to hover around 5 % in the next few years.

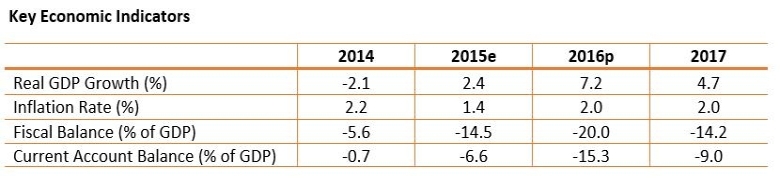

Iraq has faced two simultaneous crises since the second half of 2014: the ISIS insurgency and the oil price shock. These have severely impacted the economy and compounded structural vulnerabilities. The twin crisis, coupled with political instability in 2014, decelerated private-sector consumption and investment, and limited government spending, particularly on investment projects. As a result, the non-oil sector is estimated to have contracted by 9.0 % in 2015, following an 8.8 % fall in 2014. In contrast, growth in the oil sector has remained resilient, with output rising 12.9 % in 2015 to a new high of 3.5 million barrels per day, supported by the southern oil fields, which are beyond ISIS’ reach, and which account for 90 % of total production. After contracting 2.1 % in 2014, real GDP is estimated to have rebounded to 2.4 % in 2015. Inflation was 1.4 % in 2015.

The twin crises have resulted in a sharp deterioration of both fiscal and external accounts and worsening poverty. The fiscal deficit widened to 14.5 % in 2015, due significantly to lower oil revenues and higher humanitarian, and security-related expenditure. The government implemented fiscal consolidation measures in mid-2015, aimed at improving revenue collections, in particular from oil, and at containing non-oil primary spending. The large fiscal deficit, meanwhile, has been financed through external borrowing, including loans from the IMF and the World Bank. The twin crises have also led to the widening of the current account deficit to 6.6 % of GDP in 2015, reflecting a 47.3 % drop in export earnings in 2015. Poverty reached 22.5 % in 2014 nationwide; and in the ISIS-affected governorates, the direct impact of economic, social and security disruptions is estimated to have doubled poverty rates to 41.2 %. Internally displaced persons make up half a million of Iraq’s poor in 2014.

The economy is projected to recover from a low base, growing at 7.2 % in 2016 and to hover around 5 % in the next few years. This is driven by the projected ramp-up in oil production, increase in oil-related FDI, structural reforms, implementation of the IMF program, and a lessening of the incremental impact of the ISIS insurgency going forward. With the Iraqi selling oil price projected at $30, which is significantly below the 2015 oil price and the 2016 budgeted price of $45 p/b, fiscal and external positions are expected to remain under pressure. Despite the moderate reduction in military-related spending and the fiscal consolidation measures, the fiscal situation is projected to worsen due to lower oil revenues, with the fiscal deficit expanding from 5.6 % points of GDP in 2014 to 20.0 % of GDP in 2016 on current policies, though the financing of such a deficit will be challenging. On the external side, the current account deficit is projected to widen from 6.6 % of GDP in 2015 to 15.3 % of GDP in 2016. Higher-than-projected oil prices would improve both the fiscal and external balances.

The macroeconomic outlook is subject to significant risks related to the global environment, social and political developments, and the ISIS insurgency. A weaker pace of global economic growth or continued excess global oil supply could put downward pressure on global oil prices and renew pressures on the twin deficits. Any worsening of the ISIS insurgency would materially and negatively impact the economy. Domestic political tensions could rise anew, which could undermine the reform effort. The large fiscal consolidation effort, especially highly sensitive streamlining of the wage bill, could also give rise to social tensions, impact the implementation of reforms, and exacerbate further existing fragilities and conflict.