Poverty in Uganda has fallen substantially over the past 20 years. From 1992 to 2005, the proportion of the population living in poverty declined from 56.4 percent to 31.1 percent. However, sluggish growth and the drought of 2016-17 have reversed some of the gains. Inequality too increased with the GINI index, a measure used to monitor inequality, increasing from 0.40 in 2012 to 0.43 in 2016. Using data from the Uganda National Household Survey of 2016-17, a new report analyzed how the country’s fiscal system affected poverty and inequality.

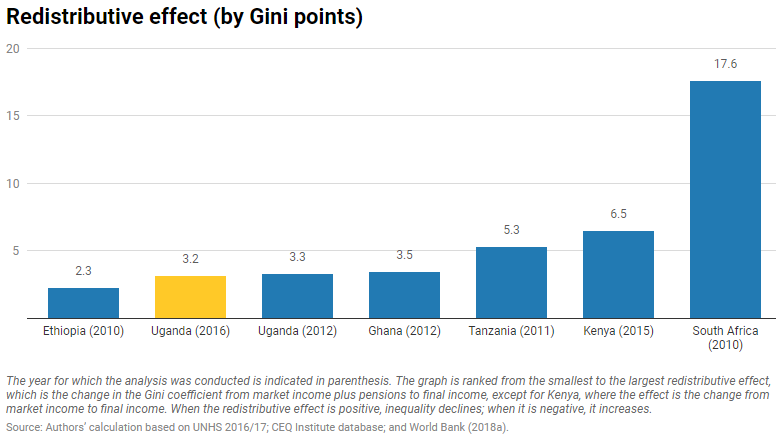

The report — Impact of Fiscal Policy on Poverty and Inequality in Uganda — notes that Uganda’s fiscal policy is moderately equalizing and lowers the Gini coefficient by 3.2 points. Personal income tax, followed by education in-kind transfers, are the biggest contributors to reducing inequality. Although equalizing, fiscal policy can induce poverty in Uganda.

“Using the internationally-recognized methodology developed by the Commitment to Equity Institute, this study analyzes the incidence of public revenues and expenditures on the level of poverty and inequality in Uganda,” said Carolina Mejia-Mantilla, one of the authors of the report. “With poverty and inequality forming the two foundational pillars of Uganda’s Second National Development Plan, the report aims to provide an understanding of the impact of fiscal policy that is critical for budget deliberations.”

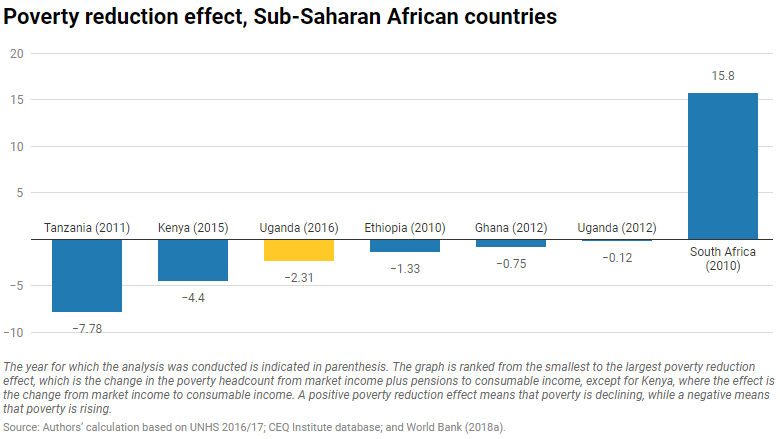

The report takes into account the combination of both revenues and expenditures in conjunction and looks at the net fiscal incidence and shows that while fiscal policy as a whole is moderately equalizing, it is poverty inducing.