Recent developments: Growth in the South Asia region has picked up in 2017. In India, recent data indicate an acceleration in growth, with an easing of cash shortages and a rise in exports. An increase in government spending, including on capital formation, has partially offset soft private investment. In Pakistan, favorable weather and increased cotton prices are supporting agricultural production, and the China-Pakistan Economic Corridor infrastructure project and a stable macroeconomic environment have contributed to an increase in private investment.

Growth in Bangladesh has been supported by solid agricultural activity and robust services, despite external and domestic challenges. In Sri Lanka, a resumption of Chinese-funded investment and infrastructure projects have lifted private investment and foreign direct investment inflows, and fiscal consolidation under an International Monetary Fund program has helped improve investor sentiment. In Bhutan and the Maldives, growth has continued to gain traction and Nepal’s growth has rebounded strongly following a good monsoon.

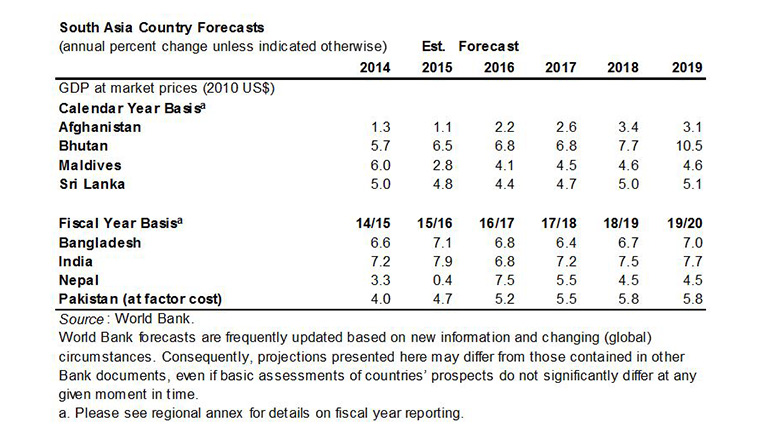

Outlook: Growth in the South Asia region is forecast to advance to a 6.8 percent pace in 2017 and accelerate to 7.1 percent in 2018, reflecting a solid expansion of domestic demand and exports. Excluding India, regional growth is anticipated to hold steady at 5.7 percent this year, rising to 5.8 percent in the next, with growth accelerating in Bhutan, Pakistan, and Sri Lanka, but easing in Bangladesh and Nepal.

India is expected to accelerate to 7.2 percent in fiscal 2017 (April 1, 2017 – March 31, 2018) and 7.5 percent in the following fiscal year. Domestic demand is expected to remain strong, supported by policy reforms. Pakistan is expected to pick up to a 5.2 percent rate in fiscal 2017 (July 1, 2016 – June 30, 2017) and to 5.5 percent in the next fiscal year, reflecting an upturn in private investment, increased energy supply, and improved security.

Sri Lanka’s growth is forecast to accelerate to a 4.7 percent rate in 2017 and 5 percent in 2018, as international financial institution programs support economic reforms and boost private sector competitiveness. Growth in Bangladesh is forecast to ease to 6.8 percent in fiscal 2017 (July 1, 2016 – June 30, 2017), to 6.4 percent in the next fiscal year, and then accelerate to an average of 6.9 percent over fiscal 2019 and 2020, supported by improving remittances as Gulf Cooperation Council countries recover and as business confidence and investment gain momentum.

Risks: Risks to the outlook are tilted to the downside. Setbacks to reform processes would slow the removal of supply constraints, dampen productivity growth, and hinder integration into global value chains. Security concerns in countries such as Afghanistan and Pakistan could hold back investment and business confidence.

Despite progress in fiscal consolidation, public debt remains high across the region, and contingent liabilities are building up. While South Asia is less integrated into the global economy than other regions, and therefore less likely to be affected by negative external shocks, several external risks remain a concern. One is the possibility of weaker-than-expected demand, or a rise in trade restrictions in advanced economies, which could weigh on exports. Another is the possibility of an abrupt market reassessment of the U.S. monetary policy tightening, which could lead to capital outflows. Yet another is the uncertain outlook for remittances, which could slow in the aftermath of tighter immigration policies in advanced economies or continued fiscal consolidation among members of the Gulf Cooperation Council.

Risks of natural disaster from extreme weather events have also increased substantially in recent years.