Only one-third of the small and medium-sized enterprises (SMEs) in the world are run by women.

, particularly in accessing finance.

An estimated 70% of women-owned SMEs in the formal sector in emerging markets are underserved by financial institutions. This amounts to a financing gap of $285 billion.

There are many reasons for this.

Women are less likely to own assets which can serve as collateral and are more likely to be excluded because of unequal property rights or discriminatory regulations, laws and customs.

Addressing this financing gap and investing in women-owned enterprises is one of the highest-return opportunities available in emerging markets.

The growth of female-owned enterprises can be a key driver in reducing overall high unemployment rates since unemployment rates among women are higher and since women are more likely to hire other women.

Women Entrepreneurs in Ethiopia: Over the past decade, Ethiopia has achieved high economic growth, averaging 10.7% per year, establishing the country among the fastest growing economies in Africa and the developing world. However, Ethiopia is falling behind its peers in the area of credit to the private sector. According to the World Bank’s Enterprise Surveys, access to finance is perceived as the main business environment constraint by micro (41%), small (36%), and medium (29%) enterprises in Ethiopia, compared to a Sub-Saharan Africa average of 24%, 20%, and 16% respectively.

At the same time, opportunities for women entrepreneurs in Ethiopia lag far behind those of men.

In The Economist’s Women’s Economic Opportunity index, Ethiopia occupies the 107th rank out of 112 countries. Growth-oriented women-owned enterprises don’t have the investment they need to thrive. Most fall into a “missing middle” trap, in which they are served neither by commercial banks nor by microfinance institutions. High minimum loan sizes and excessive collateral requirements restrict women’s access to loans from commercial banks. Microfinance Institutions (MFIs) primarily cater to micro-firms with group lending schemes that provide very small loans, and tend to have low outreach to women (30%).

Women’s Entrepreneurship Development Project (WEDP) is a $50 million IDA investment lending operation designed to address the key constraints for growth-oriented women entrepreneurs in Ethiopia. DFATD Canada and UK’s DFID are key development partners funding part of the project’s activities with an additional $13 million. The project became effective in October 2012.

.

Since the project created the first ever women-entrepreneur focused line of credit in Ethiopia in 2013, the demand has been staggering. The WEDP line of credit is disbursing roughly US$2 million in loans to growth-oriented women entrepreneurs every month, far exceeding initial targets. Several hundred women participate in the project’s cutting-edge entrepreneurship training program each month, which draws lesson from modern cognitive psychology and equips participants not only with business skills in the traditional sense, but also with the ability to ‘think like an entrepreneur.’

As of August 2015, the project provided loans to more than 3,000 women entrepreneurs and entrepreneurship training to 4,500 woman. The project has exceeded most of its own forecasted plans and expectations, and is amongst the highest-disbursing and highest-rated projects in the region.

How it Works: WEDP’s line of credit involves a market “up-scaling” operation where the Development Bank of Ethiopia (DBE) acts as a wholesaler and MFIs act as retailers. The project uses an incentive approach aimed at (i) helping DBE developing a new business line involving wholesaling of MSE subsidiary loans and provision of related technical support to participating MFIs; and (ii) helping the MFIs build up a high quality MSE loan portfolio based on credit techniques that have been developed and validated under successful micro and small loan programs in other countries, introduced through downscaling or upscaling approaches to microfinance.

Top Achievements: WEDP is changing the way the microfinance sector caters for micro and small entrepreneurs and is reaching previously underserved segments of the population. WEDP disbursed US$22 million in loans to female entrepreneurs in 2014, against a target of US$16 million, with repayment rates (99.6%).

An embedded impact evaluation component is capturing key learnings and results of the project.

Some key achievements are as follows:

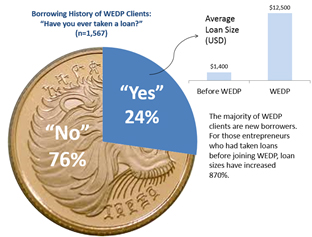

- Reaching the underserved: WEDP is successfully reaching its target segment of under-served women entrepreneurs, who have the desire and potential to grow their businesses. 76% of WEDP clients have never taken a loan before.

- Unlocking needed capital: One of WEDP’s objectives was to increase loan sizes, since most Ethiopian women-owned enterprises were stuck in a ‘missing middle’ trap where loans offered by microfinance were too small to meet their needs. For repeat borrowers, loan sizes have increased on average by 870%.

- Catalyzing growth: According to initial surveys, the average WEDP loan has resulted in an increase of 24% in annual profits and 17% in net employment for Ethiopian women entrepreneurs, one year after taking the loan. These female-owned businesses are continuing to grow, as the impacts of capital investments play out. Repayment of loans stand at 99.6%.

- Improving capacity of lenders: Through a dedicated technical assistance component, WEDP is building the capacity of . The MFI’s improved ability to appraise, resulted in their capacity to reduce the collateral requirements from an average of 200% of the value of the loan to 125%. At the same time, WEDP microfinance institutions are adopting and diffusing new techniques to reach and serve women entrepreneurs better. They are developing new loan products and recognizing new forms of collateral such as vehicles, personal guarantees, and even business inventory, to secure loans. This is all the more relevant in a country where there is no existing collateral registry.

- Underwriting innovations in the sector: WEDP is introducing innovative credit technologies to lenders, such as psychometric tests which can predict the ability of a borrower to repay a loan and reduce the need for collateral. This technology allows entrepreneurs who do not have collateral to take an interactive test on a tablet computer which predicts their likelihood to repay. If they score highly, they can borrow without traditional collateral. The test is being piloted under WEDP and subjected to a rigorous impact evaluation. Other banks are asking for the technology already, and scaling-up this technology could have a sea-level change on access to credit in Ethiopia

“With WEDP, the microfinance institutions’ appetite for risk has increased. Previously, they provided loans in small amounts of $1000 - $1500. Now, they are making WEDP loans averaging over $10,000. Plus, they have taken part in a capacity building program, which helped them assess these larger loans using cash flow analysis and risk mitigation techniques. So the MFIs are strengthening both in terms of loans disbursed as well as in their knowledge of lending,” said Beimnet Foto, Principal Appraisal Officer, Development Bank of Ethiopia.

Top Challenges

Unlocking the growth potential of Ethiopia’s women entrepreneurs involves addressing a number of intractable constraints. To date, the project has encountered several important challenges and learnings:

- Lenders need help too. Helping lenders move away from traditional collateral-based lending and adopt innovative (and likely more effective) forms of appraisal is a powerful way of expanding access to women entrepreneurs. Improved appraisal can be easier and more profitable for lenders, but changing the way a bank makes loans takes time, and most lenders are cautious when reforming these fundamentals. Flexible, responsive, long-term technical assistance to lenders is critical in bringing about sustainable changes.

- Engaging men is critical. When women entrepreneurs grow their businesses, dynamics in the household and the family can change. Engaging husbands, partners, and male family members to ensure their buy-in and support is critical. Linking women entrepreneurs with trusted male mentors and role models in other sectors can help them transition into more profitable businesses.

“WEDP’s Access to Microfinance component provides excellent experience to show financial institutions that and that with good cash flow analysis and lending procedures, collateral requirements can be relaxed.” (Independent Review of WEDP, July 2015). - Training is hard. While most women entrepreneurs say that they want to enhance their skills, many don’t register for training programs. Women usually cite time constraints or concerns about quality as the main reasons why they won’t attend entrepreneurship trainings. At the same time, women who participate in WEDP’s entrepreneurship trainings tend to rate them very highly and recommend them to others. Entrepreneurship training needs to be of high quality, in accessible locations, and at convenient hours, in order to attract busy women entrepreneurs. Marketing the benefits of training programs is critical.