The latest MENA Economic Monitor Report- Spring 2016, expects Egypt’s growth to slow down to 3.3% in FY16, before rebounding thereafter.

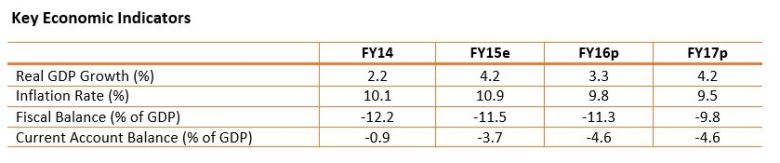

Economic growth doubled (to 4.2 %) in FY15, after four years of slow growth. Yet challenges remain, and were aggravated by the recent foreign exchange crunch. Growth in FY15 (July 2014/June 2015) was attributed to the restoration of stability and improved confidence, resilient private consumption, and the government’s public investments that started to crowd in private investments. The first quarter of FY16 witnessed subdued growth (of 3 %, from 5.6 % a year earlier), mainly due to foreign exchange shortages that stifled production. The inadequacy of foreign exchange along with an overvalued Pound hampered Egypt’s competitiveness; lowering the volume of exports by 26 % in Q1-FY16. Unemployment inched downwards (to 12.8 % in the H1-FY15 versus 13.3 % a year earlier), albeit partially reflecting dropouts from the labor force. The labor force participation rate dropped to 46 % of the adult population (those above 15 years old) versus 50 % at end-2010. Headline inflation eased slowly in early-2016, reaching 9 % in February 2016, from an average of 11 % in the previous three months. The Central Bank of Egypt (CBE) has recently started tightening monetary policy to curb inflation, especially in light of the recent exchange rate depreciation.

The CBE allowed the official exchange rate to weaken in mid-March as pressures on external accounts intensified. Net international reserves (NIR) dropped in FY16, due to large debt repayments, the unfavorable external environment, the recent crash of the Russian airplane over Sinai, as well as the CBE’s ongoing injection of foreign exchange to meet import needs and to clear forex backlogs. Thus, NIR declined to just below $16.5 billion in October 2015, and has stabilized at this level through end-February 2016. The CBE left the official exchange rate to weaken by 14.3 % on March 14, 2016, after the parallel market premium had surged to 18 % above the official rate. The CBE held a later auction at a slightly stronger exchange rate, but still signaled a move towards more flexibility.

The fiscal stance improved in FY15 due to key consolidation measures, but the reform momentum has faded in FY16. The budget deficit reached 11.5 % of GDP in FY15 (compared to 12.2 % of GDP in FY14, and 13 % of GDP in FY13), thanks to the partial streamlining of energy subsidies, revenue-enhancement measures, and the drop in international oil prices. This was achieved whilst the government raised allocations to health, education, and infrastructure, in line with the constitutional mandate. Yet, the reform pace has slowed down in FY16, as the energy subsidy reform program was only partially implemented, and the ratification of the VAT and the mining laws have been delayed.

The outlook is for GDP growth to slow down to 3.3 % in FY16, before rebounding thereafter. A combination of unfavorable domestic and external factors is undermining growth in FY16. Important sectors have been underperforming, notably, the extractives which continue to suffer from liquidity issues (accumulated arrears were recorded at $3 billion in end-2015); and tourism, affected by the Russian plane crash last October. Externally, the sluggish recovery of the Euro zone is expected to weigh on Egypt’s growth, while the lower oil prices and slowdown in Gulf countries might negatively impact Egyptians’ remittances; hence private consumption. The deficit is expected to decline to 11.3 % of GDP in FY16, and decline further in the medium term, with continued fiscal consolidation effort. Egypt’s external accounts are likely to worsen in FY16 before recovering afterwards, provided that monetary authorities continue to ease restrictions on foreign exchange and re-align the exchange rate.